| 2024 | 2025 | ||||||

| Price: | 14,185.00 | EPS | 852 | 1052 | |||

| Shares Out. (in M): | 1,218 | P/E | 16.6 | 13.5 | |||

| Market Cap (in $M): | 112,647 | P/FCF | 12.3 | 10.1 | |||

| Net Debt (in $M): | 20,224 | EBIT | 1,461K | 1,775K | |||

| TEV (in $M): | 134,325 | TEV/EBIT | 14.1 | 11.6 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

Description

Sony Investment Thesis

July 19, 2024

Sony – The awakening global giant in video games and anime

Sony (~$116 billion enterprise value) is a leading Japanese multinational conglomerate that generates $81 billion in revenue and $9 billion in earnings across six business segments. Most of Sony’s revenue comes from “Sony Entertainment,” which combines three of these segments (Games, Pictures and Music) and represents 58% of group revenue and earnings.

Sony is widely recognized for its leadership in electronic hardware, financial services in Japan, and legacy media (music, TV series, and movies). While these businesses are rightfully celebrated and contribute to the company’s valuation, there is a much more compelling and future-facing aspect of Sony’s business that remains underappreciated and undervalued by the market – its two generational consumer platforms, PlayStation and Crunchyroll. These platforms are capturing secular growth in key consumer categories: video games and anime.

We believe PlayStation should now be seen not as a hardware business or a hit-driven content business, but rather as a crucial distribution channel for games, functioning as an “App Store” platform for purchases, content library, and storage. As this transition unfolds, PlayStation will hit a “magic window” in which the lifetime value of its customers will grow ~3x over the next 5 years.

The other key secular growth area for Sony is the global rise of anime. Sony owns the world’s largest video streaming platform for anime, Crunchyroll. Crunchyroll is the “Netflix for anime,” has scaled to +140M users, and is entering a robust growth stage where it will increase monetization and widen its user base.

PlayStation and Crunchyroll already collectively generate high-margin software earnings of ~$2 billion today, but we believe this will grow 5.2x to $10.4 billion over the next 5 years. These two consumer platforms are driving a major inflection for Sony, positioning it as a leading global owner of industry-leading, digital-first, software-driven, engagement-based entertainment platforms. Altogether, this new Sony Entertainment will account for +71% and +81% of revenue and earnings respectively in the next 5 years. Despite this, the market still views Sony as a cyclical hit-driven hardware manufacturer and legacy media owner. We believe Sony today offers a robust ~3x upside to reach our intrinsic value estimate of ~$362B enterprise value, with PlayStation and Crunchyroll driving our upside case (Fig. 1).

Figure 1. Sony offers ~3X upside on the back of entertainment platforms PlayStation and Crunchyroll

Our first and most critical assumption is that Sony’s Games business has undergone a major secular transition, from a hit-driven, hardware-dominated cyclical model to a true platform model characterized by recurring spending patterns. PlayStation is now a “generational” consumer platform.

Historically, Sony’s Games business has shown significant cyclicality between console generations, with operating profit turning negative during the transitions to the PlayStation 2, 3 and 4. Only with its most recent console generation, the PlayStation 5 (PS5), did Sony break out of this cyclical pattern (Fig 2).

Figure 2. PlayStation has become significantly less cyclical

This has occurred because the PlayStation has now become a generational platform—a “ticket into a software ecosystem” rather than just a piece of hardware. It owns the distribution channel for buying your games, it provides the interface for storing them, and it serves as the central hub for managing your game library and your entire gaming experience (Fig. 3).

Figure 3. PlayStation has become a generational platform, controlling both distribution and content library

PlayStation generates software revenues through three key avenues: its App Store, Live Service games, and Subscriptions. Together, these three avenues have grown from $10.1 billion in FY2019 to $16.6 billion in FY2024 (Fig 4). This represents a 10% CAGR and we believe the next 5 years will see an acceleration to +12% CAGR, reaching $29.2 billion in revenues.

Figure 4. Sony’s Games business now makes +$16.6 billion in annual software revenue

We will break down each of these drivers below.

-

App Store

PlayStation is at its core a key distributor of third-party games, which represent +86% of total software unit sales. Its evolution to an “App Store” was made possible by a structural shift to digital distribution – gaming consumers now make direct purchases via digital channels, bypassing retail middlemen. This evolution has transformed PlayStation from a physical console needed to play games to a comprehensive “App Store” platform that is a key distribution channel for buying games.

This has had a profound impact, as PlayStation now acts as a toll road on every digital game purchase (Fig. 6). This shift not only provides PlayStation with a higher take rate and profit margin vs. physical distribution, but also benefits third-party publishers, who retain a larger share of revenue compared to physical sales. This is a win-win for both the industry as a whole and for consumers, who have structurally shifted their behavior: Since FY2016, PlayStation’s digital penetration rate has expanded from 19% to 70% today, and we project it will reach 90% by FY2029E.

Figure 6. Consumers are now making purchases directly via PlayStation’s “App Store,” which charges a 30% “toll” on every digital purchase

-

Live Service Games

Digital distribution not only supports the downloading of traditional buy-to-play games; it also enables live service games, which monetize through “add-on content” (downloadable content or “DLC” and microtransactions). Over the last six years, Sony has nearly doubled its revenue from add-on content, and will surpass the FY2021 COVID high this year. With growth now renormalized, we project this revenue stream will double again over the next 5 years (Fig. 7).

Figure 7. PlayStation is now also a platform for live service games

It’s not just the quantity of this revenue stream that matters; it’s also the quality. Online multiplayer live service games that generate add-on content revenues are designed for long-term play (sometimes over decades) and continuous engagement. Their rise has transformed PlayStation into a digital-first platform with significant recurring revenue. Today, 51% of PlayStation’s App Store revenue consists of a “stable base of revenue from major franchise titles, with a large share of ongoing content” (see Appendix 1). Looking ahead, Sony plans to allocate over 60% of its studio investments to live service games by 2025. And we expect GTA VI (a third-party title), the biggest game to launch in over a decade, to launch alongside Sony’s online live service offering in 2025. We anticipate live service games will continue to grow their share of engagement in the coming years, expecting 2 out every 3 major launches (including content updates, expansion packs and packaged games) to be from live service titles by FY2029E (Fig. 8).

Figure 8. Live service games will expand to a majority on the back of a shift in Sony’s first-party development spend

With the rise of live service games, users on old hardware remain engaged and monetized, seamlessly carrying forward their engagement and spending to new-generation hardware, thereby mitigating cyclicality. As of April 2024, half of PlayStation’s monthly active consoles are still on PS4 and account for 37% of total engagement hours. We believe many of these users will eventually transition to PS5 in the coming years, and in doing so accelerate on the margin the digital spending ratio, revenue, and engagement for PlayStation (see Appendix 2).

-

Subscription

PlayStation is now also an engagement-based network, facilitated by PlayStation Plus subscriptions that offer access to shared online multiplayer gaming experiences. These subscriptions, combined with live service games, have transformed PlayStation into a dynamic platform with approximately 50 million highly engaged, highly monetized, and significantly stickier monthly paying subscribers (Fig. 9).

Figure 9. PlayStation has ~50m monthly paying subscribers who pay as part of their regular “life expenditure budgets”

As Live Service games continue to grow their share of engagement on the PlayStation platform, we anticipate that more users will become PlayStation Plus subscribers to gain access to them. We therefore expect PlayStation’s “Network Services Revenue” (annual subscription revenue) to grow from $3.4 billion in FY2024 to $5.8 billion by FY2029E (Fig. 10).

Figure 10. PlayStation’s Network Services (annual subscription revenue)

These three components—the App Store transition, the rise of live service games, and the rise of paying subscribers—are all generators of growth for Sony, and they all generate recurring software revenue streams. Putting them all together, we believe the lifetime value of PlayStation users should increase exponentially by 3x over the next 5 years. For reference, from 2015 to 2020, during the transition from PlayStation 4 to PlayStation 5, we also saw an uplift in customer lifetime values. Essentially, the next 5 years will see an accelerating increase as more of the installed base transitions to the latest PlayStation console (Fig. 11).

Figure 11. In the next 5 years we think Sony can grow LTV on the back of live service games and the late stage PS5 console cycle

To sum up, PlayStation has evolved from a hit-driven, cyclical model that experienced significant fluctuations around key disc-based blockbuster launches, to a robust, engagement-based, digital-first platform dominated by high-margin software revenue. We expect software revenue in Sony’s Games segment to expand from $17 billion in FY2024 to $31 billion in FY2029E, and alongside that, we expect the operating margin in the segment to expand from 7% to 19% (Fig. 12), reaching a new normal operating profit level of +$7.3 billion (refer to Fig. 2).

Figure 12. We project software revenue in Sony’s Games segment to expand to $31 billion by FY2029E and for operating profit margin to expand to 19%

We believe the historical boom-bust cycles are in the past. Software is the new focal point, and hardware is simply a ticket into a vertically integrated software ecosystem. With PlayStation’s overall revenue being far more software driven, and the software increasingly becoming more recurring in nature (live service games and subscriptions), we anticipate operating margins will be far more stable at a new normal that hasn’t ever been seen before. Although we aim to be conservative in our estimates, we will not be surprised if margins eventually rise well past 20%.

Our second assumption is that Sony is the best positioned company in the world to capture the global growth and business-model evolution of the anime industry. Just as Netflix revolutionized how people consume TV shows and movies, Crunchyroll has become the go-to platform for streaming anime content. Crunchyroll is the “Netflix for anime” and will drive a major part of Sony’s operating profit growth.

Anime is one of the most exciting secular growth categories to arise from changing consumer behavior, and the industry has now emerged from being primarily dependent on Japan’s domestic market to a global phenomenon. The industry makes money across media, merchandise, books, and games. In total, the market generated $31 billion in 2022 and is expected to surpass $60 billion by 2031, growing at a 10% CAGR (Fig. 13). We estimate there are +600 million anime fans globally, a number expected to reach +1 billion by 2025.

Figure 13. The Anime industry is massive at $31 billion, and growing at 10% CAGR (see Appendix 3)

Anime fans are deeply invested in the worlds they love. They express their passion through cosplay, creating fan art, singing anime karaoke, attending conventions, and other activities. More than just a hobby, anime is a way of life for many fans, which is why a well-stocked “anime shelf” — filled with figures, boxed sets, manga, plush toys, and trinkets - is so important. Despite its mainstream success, anime is still “counterculture” in many ways to fans. Anime’s unique storytelling constructs and directorial aesthetics rooted in Japanese culture make anime feel fresh around the globe year after year, and its popularity continues to rise. It was once considered a niche genre just for hard-core Japanese fans, but streaming has helped turn it into a globally popular juggernaut.

Sony’s strategic consolidation of anime streaming services under Crunchyroll has solidified its market leadership. By the end of FY2022, Sony had unified its anime streaming assets, establishing dominance in the industry. In August 2021, Sony’s subsidiary Funimation acquired KAZÉ, followed by the acquisition of Crunchyroll in September 2021. Integration under the Crunchyroll brand began shortly after. The significant consolidation efforts were completed by March 2022, with the Funimation brand eventually phased out by April 2024. This led to notable user growth in the years that followed. Crunchyroll now boasts 146M monthly active users and 13M paying subscribers (Fig. 14).

Figure 14. Sony has consolidated the Anime industry and owns the leading steaming platform, Crunchyroll

Measured by total users, Crunchyroll is already half the size of Netflix and ranks among the top three video streaming services. However, only 9% of Crunchyroll’s user base are paying subscribers. We believe this reflects an anime streaming industry still in its relative infancy and indicates substantial growth potential (Fig. 15).

Figure 15. Crunchyroll is half the size of Netflix already, and is now a top 3 streaming service

Unlike generalist platforms such as Netflix, which typically share licensed anime content with other platforms, Crunchyroll is the primary destination for anime fans and has secured exclusive licensing agreements with a multitude of Japanese anime studios, granting it access to a vast and diverse library of anime titles not available elsewhere. In fact, Crunchyroll has the most comprehensive library of anime content, catering to both mainstream and niche anime audiences.

Although Netflix has had some success with creating its own anime content (Netflix Originals), most users continue to demand licensed content, which is often only available on Netflix for a limited time. Furthermore, Netflix typically waits to release entire seasons of this content all at once, following its binge-watching model. Crunchyroll, by contrast, can simulcast episodes shortly after they air in Japan, catering to the demand for immediate access to new content.

Additionally, Crunchyroll has cultivated a vibrant community of anime enthusiasts through forums, events like Crunchyroll Expo, and a dedicated merchandise store, fostering deep user engagement and loyalty. Moreover, Crunchyroll has already announced plans to launch creator tools to support anime studios, signaling increased collaboration and stakeholder engagement (Appendix 4).

Given the secular growth of anime in the entertainment industry, Crunchyroll’s dominant position as the go-to anime streaming platform, and its exclusive access to an extensive library of content, we expect Crunchyroll’s monthly active users (MAU) to expand from 146 million in FY2024 to 300 million by FY2029E, or +2x from here. In our MAU forecast, we assume that 25% of anime fans (600m total) are on Crunchyroll today and we maintain this assumption on back of 1.2 billion fans by 2029.

The primary reason users convert to subscribers on Crunchyroll is to unlock ad-free viewing and to access latest episodes (simulcast). Considering that fans become highly invested in their favorite anime over time, we think users will increasingly demand these features. Thus, we project Crunchyroll’s paying user ratio will expand from 9% in FY2024 to 15% by FY2029E and estimate subscriber numbers to grow from 13M to 46M (Fig. 16).

Figure 16. We expect Crunchyroll to grow to 46M subscribers by FY2029E

When we compare it with leading global streaming platforms like Netflix, we believe Crunchyroll has significant potential to increase its average revenue per user (ARPU), both by increasing the ratio of paying subscribers to total users and raising subscription prices over time (Fig. 17). Both levers rest on the same foundation: Streaming services typically become deeply embedded in users’ leisure time, and anime fans are heavily invested in their favorite intellectual properties (IPs).

Figure 17. When we consider platforms like Netflix, we believe there is still significant room for Crunchyroll to raise ARPU by raising prices and converting more ad-supported users to paying subscribers

We believe Crunchyroll has one of the most exciting revenue growth stories in global media, on the back of this user growth and expanding paying subscriber rate. We believe its topline can grow at a +45% CAGR, from $1.4 billion in FY2024 to $8.9 billion by FY2029E (Fig. 18). This is a bold forecast, but we think our assumptions are in line with the secular growth of the industry, Crunchyroll’s superior product offering, and its dominant position as the go-to platform for anime content.

Figure 18. We project Crunchyroll’s revenue to expand to $8.9 billion by FY2029E

On the back of Crunchyroll’s subscription revenue, Sony’s Pictures business is now evolving from its legacy hit-driven model centered on blockbuster Movies and TV Shows, to a pure-play video streaming platform dominated by recurring revenue.

Moreover, Crunchyroll is set to be an important profit driver, and we’re forecasting operating profit to grow at a CAGR of +55%, reaching $3.1B by FY2029E (Fig. 19). As a result, Crunchyroll will become +87% of operating profit in the Pictures segment, effectively transforming the Production segment into a pure-play video streaming platform – akin to Netflix (Fig. 20).

Figure 19. Crunchyroll will CAGR Operating Profit at +55%, reaching $3.1B by FY2029E

Figure 20. Sony’s Production segment will shift to become a pure-play video streaming platform akin to Netflix

Just as PlayStation serves as a generational platform for gaming, Crunchyroll is poised to be the generational platform for anime content. Our Crunchyroll forecasts are aggressive, but the key takeaway should be that it is a high-growth asset that is about to inflect as it begins to take advantage of the operating leverage inherit in the video streaming business model.

The main implication of our two assumptions is that Sony should now be seen primarily as a world-class, digital-first Consumer Entertainment business that owns generational platforms in games and anime. Sony’s current valuation does not come close to reflecting this, nor does it capture the medium-term margin expansion opportunity.

In FY2024 Sony’s Entertainment segments (Games, Music and Productions) accounted for 58% of group revenue. With an upcoming spin-off of its Financial Services segment and continued growth in its core engagement-based platforms, PlayStation and Crunchyroll, we anticipate that Sony’s Entertainment segments will collectively account for 71% of group revenue by FY2029E (Fig. 21).

Figure 21. Over the last 10 years Sony has evolved to become predominantly a leader in consumer entertainment; we expect this evolution to continue over the coming years

While we focused the discussion above on Sony’s new generational platforms, Crunchyroll and PlayStation, it’s also worth touching on the recurring nature of its Music business. While not directly owning a music platform, Sony does have ownership and distribution rights over its large recorded music catalogue and thus has significant supplier power in the growing music streaming industry, which monetizes on a subscription-based model. Though they reach Sony’s Music business indirectly via royalties, subscription revenues paid to music streaming services are very much “recurring” in nature, and thus this segment has itself become more recurring over time. Furthermore, Sony’s position in the music industry is one of significant power as a leading owner, creator and distributor of industry-leading Music IP (Appendix 5).

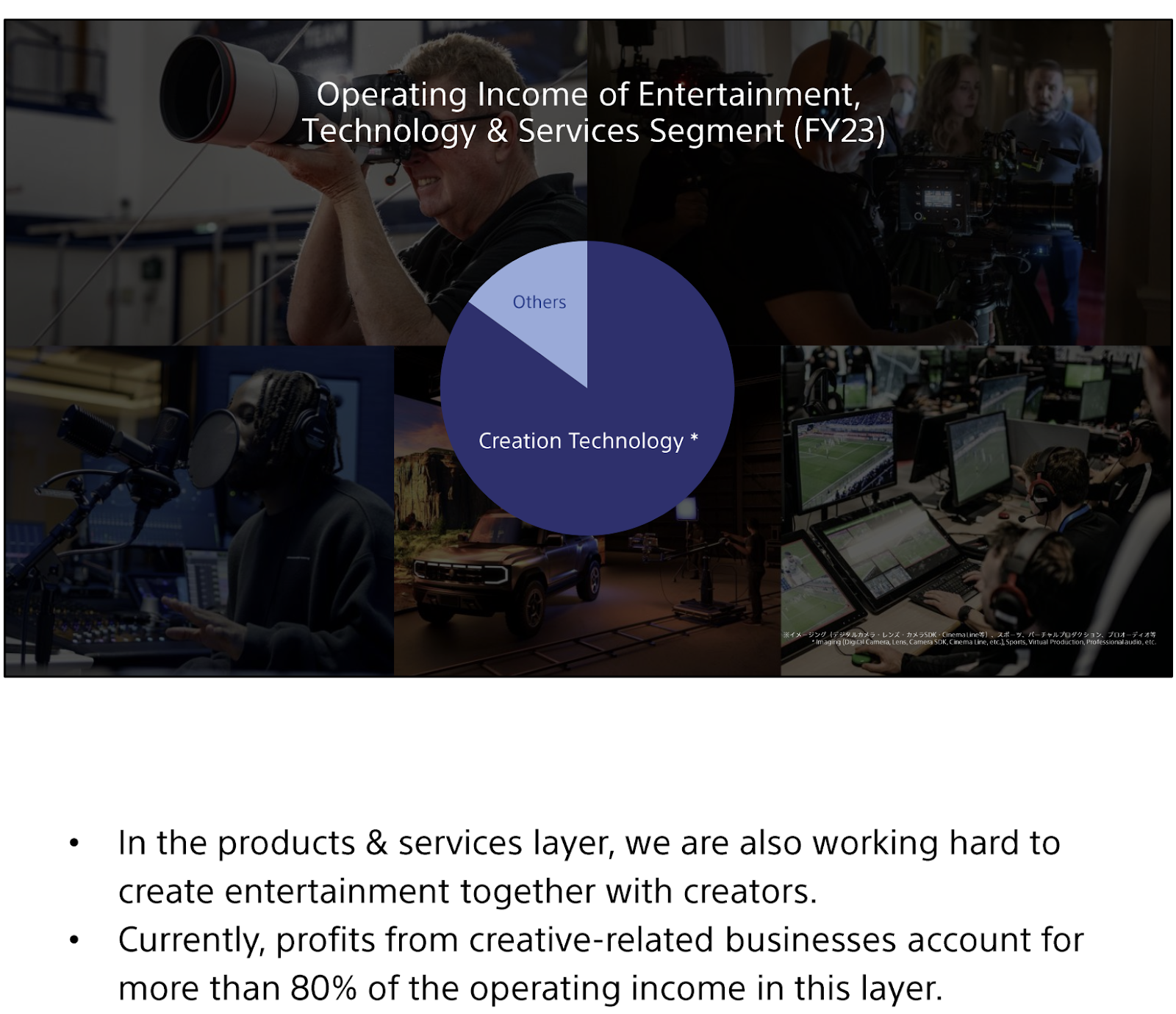

It’s also worth noting that even outside of the core Entertainment segments, Sony’s other segments are well aligned with the broader Entertainment industry. For example, in Sony’s Entertainment, Technology & Services segments (electronics), about 80% of operating profit is from “Creation Technology” that serves the supply side of the Entertainment industry (film producers, music producers, etc.) (Appendix 6).

We estimate that Sony will generate +$48 billion in revenue from its platform businesses, primarily software, by FY2029E (Fig. 22). This mix shift will drive Sony total group operating profit to expand, reaching +$17 billion by FY2029E, with its consumer Entertainment segment (including its generational platforms) expanding to account for +81% of group operating profit (Fig. 22). Furthermore, this shift in revenue and profit mix to consumer entertainment categories, which in turn are becoming platform-dominated and are higher-margin, will drive total group operating profit margin to expand from 10% in FY2024 to 17% by FY2029E (Fig. 23). Simply put, Sony is becoming one of the largest and highest-quality digital entertainment businesses in the world.

Figure 22. Sony’s generational platforms will generate +$48 billion in revenue by FY2029E

Figure 23. Group Operating Profit margin will expand to 17% by FY2029E.

Despite this, we believe the market still views Sony as a something along the lines of a “typical hardware manufacturer and legacy entertainment media supplier,” and fails to fully appreciate its market leading positions as a platform owner in two growing industries, games and anime. Because of this, we believe Sony trades at a significant discount to its true intrinsic value.

To value Sony, we apply a sum-of-the-parts (SOTP) analysis, where we separate the company into two big categories:

1) Rest of Sony (Financial, Hardware, Music, Pictures)

2) PlayStation & Crunchyroll

The major driver to our SOTP valuation comes from PlayStation and Crunchyroll (Fig. 24).

Figure 24. Sony offers 3X upside to reach our intrinsic value estimate

We broke out “Rest of Sony” into its 4 major business lines: Financials, Hardware, Music, and Pictures. We then applied average peer earnings multiples to what we believe each business would earn in 5 years (Fig. 25).

For PlayStation and Crunchyroll, we broke out their respective earnings and attached premium valuation multiples to reflect quality and growth. We believe this is most contrarian part of our thesis, where we see the combination of earnings growth and valuation multiple re-rating driving our intrinsic value estimate.

Figure 25. Breaking out Sony’s SOTP by business line

In addition to this SOTP analysis, when evaluating Sony on near and medium-term valuation metrics against peers, it becomes evident that Sony is also undervalued given its current business quality. Despite generating 66% of revenue and 68% of operating profit (excluding the Financial Segment to be spun out) from its leading entertainment businesses, Sony continues to be valued closer to a typical hardware manufacturer. If we take Sony’s current revenue mix by business and only apply average industry multiples to each revenue stream, it should trade at 3.3x (Fig. 26).

Figure 26. Despite Sony’s already transformed business model, it still trades with peers in the hardware manufacturing sector

We project that Sony’s entertainment business will account for over 71% of revenue and 81% of operating profit by FY2029E, with the group achieving a 17% operating profit margin. As the market starts to recognize Sony as a leading entertainment company with core engagement-based platforms, we anticipate a significant rerating in its valuation, with a multiple approaching its platform peers. We believe a fair multiple, reflecting the mix of Sony’s businesses, is 4X EV/Revenue in the long run (Fig. 27).

Figure 27. As Sony continues its transformation it will break away from hardware peers

On an absolute basis, we believe Sony is trading at a cheap ~10x on our +2-year EBIT estimate, and less than ~6X on our +5-year estimate (Fig. 28).

Figure 28. Sony trades below 6X +5-year EV / EBIT

As Sony’s transition naturally leads to improved earnings, we predict investors will inevitably grow to appreciate the quality of its entertainment platforms. But there is one direct catalyst that should accelerate this process: In October 2025, Sony will spin off its Financial Services segment, which offers insurance, online banking, and other financial services primarily in Japan. The spin-off will underscore Sony’s commitment to becoming a leaner, more focused Entertainment business. With the Financial Services segment being spun off, and the entertainment business continuing to grow to become a bigger part of group revenue and operating profit, we expect a narrowing of Sony’s conglomerate discount, and a rerating to reflect its improved business quality and ownership of generational platforms.

What risks and concerns do we have?

-

PlayStation 5's hardware sales and software attach rates don't catch up to those of PlayStation 4, thereby hindering LTV expansion of the total user base. We think this risk is mitigated by several factors:

-

Given the much higher spend on live service games, most of which are available on both platforms, we believe the more important metric has become monthly active users (MAUs) rather than hardware installed base. Even so, PS5 hardware sales are effectively in line with PS4 hardware sales on a life-to-date basis (-1% lag) and we see significant console-selling games still in the pipeline.

-

Even if the software attach rate fails to catch up with PS4, the overall higher spend on live service games or “add-on content” will more than outweigh the decline.

-

We anticipate that software attach rates will catch up to those of the PlayStation 4, with a key factor being the launch of GTA VI, a current-generation console exclusive. This game will be a significant system-seller and will accelerate the life-to-date software attach rate of the PlayStation 5. This is particularly beneficial since the PlayStation 5 is monetizing users at a higher rate compared to the PlayStation 4. Unlike GTA V, which launched on the PS4 in the second year of its sales cycle and was a significant tailwind for software sales through the cycle, GTA VI will launch in the second half of the PlayStation 5 sales cycle. With GTA V having sold over 200 million units since its 2013 release, we believe there is huge demand for GTA VI. Thus, we believe that GTA VI will be a major catalyst in bringing PS5 hardware and software unit sales to parity with PS4.

-

-

Competition in the console gaming market.

-

First, the imminent launch of Nintendo Switch 2. The Nintendo Switch 2 will be a significantly more powerful device than its predecessor, capable of running AAA games. This could potentially disrupt Sony and Microsoft, which focus on AAA gaming. However, we believe the Switch 2 will not reach parity with current generation consoles, and major titles like GTA VI are unlikely to be available on the platform. That said, even if Nintendo Switch 2 were able to run all the same games as PlayStation 5, we see Xbox as becoming less of a threat in the console market (see more in the following point).

-

Microsoft might collaborate with Nintendo to introduce Microsoft Game Pass on the Switch 2, potentially bypassing PlayStation. Despite the historical rivalry between PlayStation and Xbox, if Microsoft expands Game Pass to Nintendo, it is probable (in our opinion) that they will also extend it to Sony’s platform. Recent trends show Microsoft releasing previously exclusive titles, such as "Hi-Fi Rush," on PlayStation 4 and 5. Microsoft's goal with Game Pass seems to be reaching as many players as possible, indicating a shift towards becoming a third-party partner for both Nintendo and Sony. This strategy could eventually lead Microsoft to phase out its hardware focus, transforming the integrated hardware-software console market from an oligopoly with three major players to a duopoly dominated by Sony and Nintendo.

-

-

Sony's operating profit margins in the games segment remain low at 7% for FY2024. In a recent management meeting, Sony acknowledged the need to improve profitability by better allocating game development budgets, prioritizing studios with successful track records, and adopting a conservative approach to others. The depressed margins are partly due to operating the supply chain at full capacity post-COVID, leading to extra costs, as well as excessive hiring and salary increases. We anticipate that Sony’s personnel expenditures will normalize as the company becomes more selective in its studio investments and budget allocations.

-

Downside risk in one of Sony’s hardware businesses, for which we don’t have a strong viewpoint.

Conclusion

Seen as a whole, Sony is a massive global enterprise that is now about to inflect, driven by its consumer entertainment businesses. We believe the opportunity comes in recognizing this new narrative emerging from its PlayStation and Crunchyroll platforms, which together can more than double group earnings and, more importantly, generate much higher-quality, highly predictable, software-driven earnings.

Our thesis is underpinned by two key assumptions:

-

PlayStation is now a generational consumer platform

-

The PlayStation business has transitioned from a hit-driven, cyclical model to a robust, engagement-based, digital-first “App Store” platform. This evolution has and continues to be driven by the structural shift to digital distribution, the rise of “engagement-based” live service games, and the increased penetration of PlayStation Plus subscribers.

-

These structural shifts will continue to significantly increase user lifetime value (LTV) as users become increasingly embedded in PlayStation’s ecosystem – buying, playing and storing their game libraries on the platform.

-

As PlayStation’s revenue continues to become more recurring in nature, and as software becomes the dominant revenue stream, margins are expected to rise significantly and reach a new norm by FY2029E.

-

-

Sony can capture massive growth in the anime industry through Crunchyroll, the “Netflix for Anime”

-

Crunchyroll is the leading anime streaming platform and will continue to capitalize on the rapidly growing global demand for Anime.

-

With exclusive licensing agreements, the most comprehensive content library for Anime content, and the ability to simulcast episodes, Crunchyroll's user base, subscribers, and revenue are projected to grow substantially.

-

The platform's low current paying subscriber ratio presents significant upside potential as Crunchyroll continues to convert ad-supported users to paid subscribers.

-

Our sum-of-the-parts (SOTP) valuation attempts to capture what this strategic inflection could be worth in 5 years, and we believe the upside is more than ~3x, with an intrinsic value estimate of ~$362 billion. We believe that the route to bridging this valuation gap involves a combination of accelerated earnings growth, margin expansion, and valuation multiple expansion as investors increasingly recognize the strength of Sony's generational platforms and its evolution into a digital-first consumer entertainment business.

Appendix:

Appendix 1:

Appendix 2:

Half of active consoles are still on PS4 and account for a significant portion of engagement hours. PlayStation 5 users, however, are far more engaged.

Life-to-date spend on PlayStation 5 is +26% higher vs. PlayStation 4 at the same point in its sales cycle.

Appendix 3:

Appendix 4:

Appendix 5:

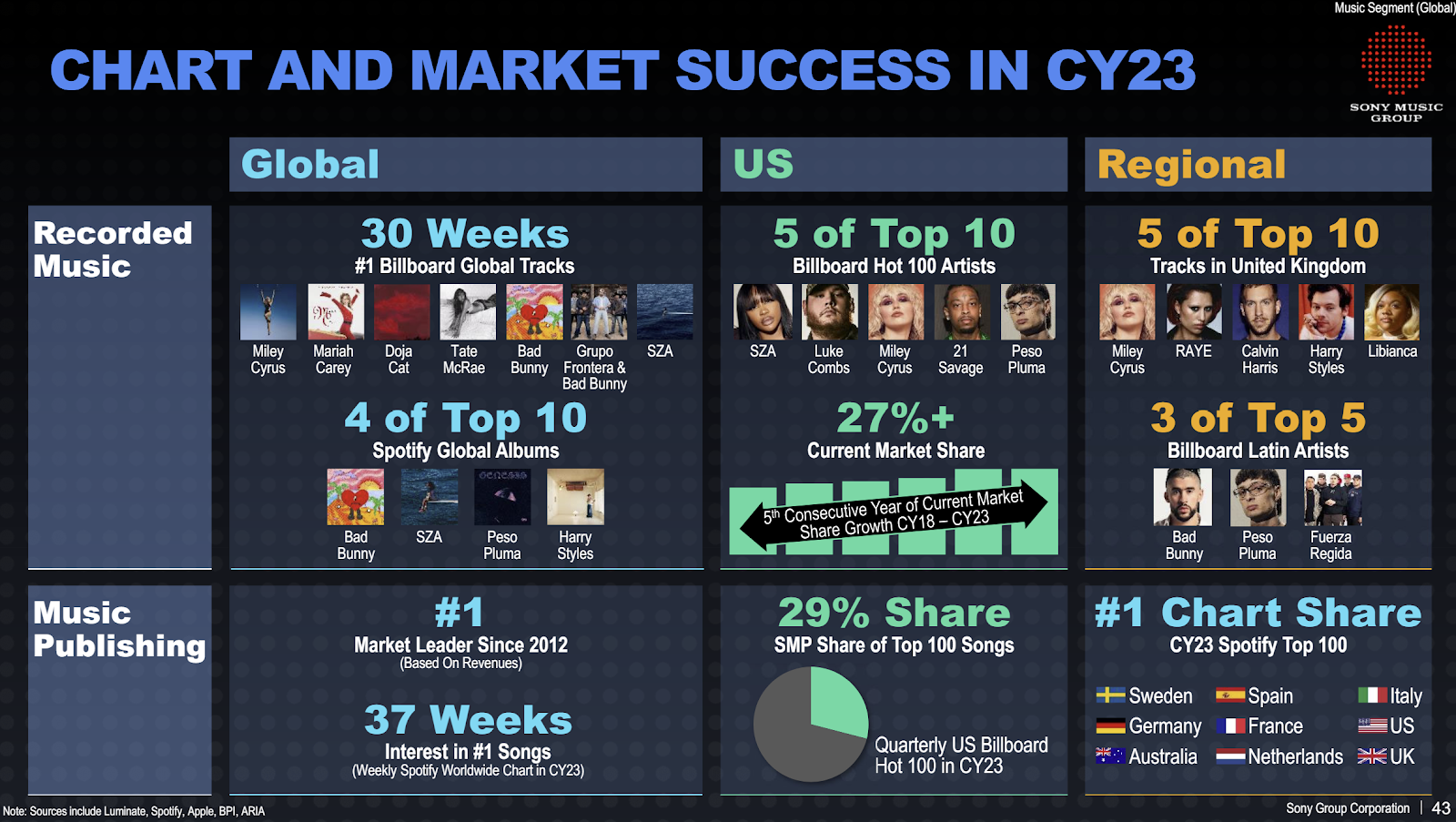

Sony’s artists and catalog continue to have incredible market success

Sony is number one in Music publishing and number two in Recorded Music

Appendix 6:

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Major first-party live service title launches as well as major third-party live service title launches, most notably GTA VI

- Sony disclosing Crunchyroll operating profit level and/or significance in the Pictures segment as well as starting to regularly disclose subscriber numbers as a KPI in their "Supplemental Information" document which is released quarterly

- Spin-off of Sony's Financial Segment, which is expected to occur in Oct 2025

| show sort by |