| 2024 | 2025 | ||||||

| Price: | 17.75 | EPS | -0.27 | 0.26 | |||

| Shares Out. (in M): | 34 | P/E | -65.7 | 69.5 | |||

| Market Cap (in $M): | 167 | P/FCF | 310 | 44 | |||

| Net Debt (in $M): | 0 | EBIT | -3 | 2 | |||

| TEV (in $M): | 146 | TEV/EBIT | -50 | 61.3 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

Description

A veteran serial entrepreneur with a Ph.D. in Physics, recognized as a pioneer in the global energy-based aesthetic device industry, is leading a new technological advancement. Together with a seasoned executive team—who previously contributed to his public market successes—he is introducing a significantly enhanced product for therapists and clients for the third time.

The company is in the midst of a global rollout of a superior product targeting a recurring 100% gross profit margin from a razor-and-blade business model (consumables), based on an installed base, satisfied therapists, and growing patient demand. The company is approaching a cash flow and profitability inflection point as sales grow and device usage increases.

Valued at a price suitable for a potential take-private transaction, the company is still under the radar of global investors due to a language barrier and its listing on a lesser-known overseas exchange. However, the company is poised for a major boost in visibility and profitability, with plans to list on NASDAQ.

Sofwave designs, develops, manufactures, and commercializes a non-invasive, full-body aesthetics platform based on proprietary technology and intellectual property (IP). The company aims to build a large, global installed base, producing high-quality, 100% gross margin recurring revenue streams, led by pioneers of the non-invasive aesthetic surgical/medical industry.

Sofwave’s patented technology is an FDA-approved procedure designed to lift, tighten, and smooth skin in various areas of the body. It provides significant improvements in skin condition and appearance, including reducing fine lines and wrinkles and lifting/tightening eyebrows, neck, arms, abdomen, thighs, and more. This can be achieved in a single treatment session, with no downtime, regardless of skin type or color.

Strategy & Business Model.

Drawing on extensive experience founding and leading multiple industry-leading businesses, Sofwave’s business model has been designed by founder Dr. Shimon Eckhouse from day one to overcome the big challenges and drawdowns of current technologies by focusing on generating better results for Patients, Therapists, and Investors with an eye on one of the biggest, most successful value creation in the industry.

Sofwave’s combination of technology and its business model results in three key advantages:

A superior outcome for the patient: faster treatment, faster results, significantly less painful, fewer treatments needed, more effective (in some cases, the only effective treatment), more FDA-approved indications and body areas, no downtime—can be done during a lunch break.

Superior economics for the therapist: lower platform costs, lower consumable costs (leading to higher clinic-level gross profit), higher ROI, shorter payback period, elimination of the need for credit underwriting in most sales processes, elimination of consumable inventory investment and maintenance, happier clients, more treatment options (resulting in increased sales and cash flow for the therapist), and centralized customer acquisition.

And a superior business outcome for Sofwave: platform sales and an installed base that generate a stable, recurring, high-margin (100% gross) consumable revenue stream, with global opportunities driven by innovative, disruptive intellectual property (IP), giving investors true exposure to the industry's value creation.

Sofwave’s founder and senior management have a highly successful, proven case study that they set out to replicate, which investors should note: the Zeltiq Aesthetics CoolSculpt body-slimming Cryolipolysis device (fat cell removal by freezing). This lower-cost platform delivers Cryolipolysis cycles charged per use, resulting in an installed base that generates a recurring, high-margin revenue stream in addition to capital equipment sales.

Zeltiq Aesthetics was acquired by Allergan in February 2017 for $2.48 billion, and later sold to AbbVie in 2020 for $63 billion.

Early indications suggest Sofwave's value proposition is recognized by both therapists and clients, and it has been adopted accordingly. The business remains relatively under the radar of global investors while trading on the Tel Aviv Stock Exchange, but this is expected to change with a Nasdaq listing anticipated around 2025.

Past Experience Applied to Building a Recurring Cash Flow Machine.

Sofwave strategically reduces capital equipment gross profit by pricing the platform at under $100,000. This price allows therapists to more easily access hassle-free credit card funding to purchase the device, in contrast to the stricter underwriting requirements of higher-priced competitors. Faster, easier sales close, reducing friction and improving business outcomes.

Lower platform costs compared to competitors result in a higher return on investment and a shorter payback period for the therapist, creating a strong business case even before considering the superior outcome for the end client.

Each device comes preloaded with 3,000 pulses included in the sales price. The therapy involves delivering energy pulses into the patient’s skin, with the exact number of pulses varying based on the treatment area and indication.

Once the 3,000 pulses are used, the therapist reloads the device by purchasing additional pulses from Sofwave. Pulses cost $1.50 each, though purchasing in bulk can reduce the price.

Pulses are essentially a digital product, carrying a 100% gross profit margin and contributing fully to the pre-tax bottom line. This provides Sofwave with a strong incentive to help therapists maximize device usage and grow their Sofwave business through support, marketing, and expanding use cases via R&D.

Business Benefits for the Therapist.

Apart from the therapy’s superiority (discussed later), the therapist benefits from the following economics:

Doctors typically charge patients around $2,000 to $2,500 per full face and neck treatment. Pulses for a single treatment (per FDA guidelines) cost the doctor $150 to $200 in consumables, without the need to hold any inventory or manage boxes.

Pulses can be bought very close to the patient’s arrival (improving working capital management at the clinic’s level) in addition to generating a 90% gross profit margin for the therapy sold.

With two treatments per week, therapists can recoup their investment within 5-7 months (compared to over a year for competitors) and easily cover installment or credit payment terms.

Using the popular InMode device for comparison, the same doctor would need a set of 3 treatments to achieve the same result, paying $400 in consumable costs per treatment, or $1,200 total COGS.

This results in about 50% gross profit for the series, which takes more time and is less desirable for the end user, even for competing indications (Sofwave indications cover a wider scope).

Happy clients are returning for additional treatments, which offer higher gross profit margins and lower administrative complexity, creating a strong incentive for therapists to increase the usage of their Sofwave device. This drives a healthy, growing global recurring revenue stream with high double-digit to triple-digit growth rates.

Global Expansion Strategy.

Sofwave is focused on global expansion, with direct sales efforts concentrated in the US and the UK, while utilizing distributors for other regions.

Distributors benefit from discounted prices, which reduce Sofwave’s gross profit on their sales. However, this is offset by the elimination of the need to invest in S&M for these regions, a major expense that typically accounts for approximately 40% of revenues. As a result, the business maintains healthy bottom-line economics for scalable systems and pulse distributor sales.

Most recently, Sofwave has received marketing approval from ANVISA (Brazil Health Regulatory Agency), the Taiwan Food and Drug Administration (2022), and Mexico’s Food and Drug Administration (2023).

Sofwave expects imminent approval from Japan’s Food and Drug Administration. In addition, Sofwave is conducting comprehensive clinical trials in China through its partner HTDK, with potential NMPA authorization in 2025 or 2026.

It is worth noting that when Sofwave announces regulatory approval in a new territory, the announcement typically coincides with a significant purchase by the local distributor, as preparations for launching local sales are already in place.

Brand Awareness, Marketing, and Sales Strategy.

Sofwave is running an in-house online marketing campaign aimed at increasing awareness of its new, innovative therapy and generating demand, which is then routed to doctors capable of providing the treatment. Doctors, who are often not skilled in marketing, greatly appreciate Sofwave’s support in attracting patients and helping them grow their practices. This approach is unusual in an industry that typically focuses on capital equipment sales. By aligning Sofwave’s incentives with the success of its clients, this strategy fosters a differentiated relationship between doctors (clients) and Sofwave (supplier), resulting in a stronger, higher-quality partnership.

Sofwave engages core audiences, including dermatologists and plastic surgeons, through conferences and exhibitions, as well as strong word-of-mouth marketing as doctors share their clinical and business successes. In addition, Sofwave reaches its audience through direct contact, with experienced salespeople presenting the product to their established client base.

Based on search traffic and site visits, Sofwave's brand awareness is trending positively.

In a move similar to Zeltiq, Sofwave hired a team of Practice Development Specialists to follow up with newly onboarded or under-active therapists, ensuring they are fully supported. This team provides advice, additional training, support, and assistance in activating the new device and increasing its usage, capturing a greater share of treatments in the doctor’s clinic.

According to management’s comments during the second-quarter 2024 call, this initiative is already yielding positive results.

Technology Evolution, Founder Significance, Competitors, and Competitive Advantage.

To understand what sets Sofwave apart in its competitive industry and management pedigree, we need to take a broader look at the technology, and the industry's historical evolution.

Youthful beauty is often associated with firm, glowing, smooth, and healthy-looking skin, as opposed to the wrinkled and sagging skin that comes with aging.

The dermis is a thick layer of skin that contains fibrous and elastic tissue, providing strength and flexibility. Fibroblast cells in the dermis produce collagen and elastin, which contribute to skin's fullness, smoothness, and elasticity.

As we age, the levels of collagen and elastin in the dermis decrease, causing the skin to lose its fullness and elasticity, leading to sagging, wrinkles, and a less youthful appearance.

Extreme diets or rapid weight loss, such as that caused by GLP-1 agonist medications, can also result in loose, sagging skin, sometimes referred to as the 'Ozempic look.'

Generally, all non-invasive aesthetic devices aiming to improve sagging skin and wrinkles work by increasing the levels of collagen and elastin in the dermis, either directly or indirectly. Most successful products on the market today fall into one of several technological evolutions developed throughout the industry's history.

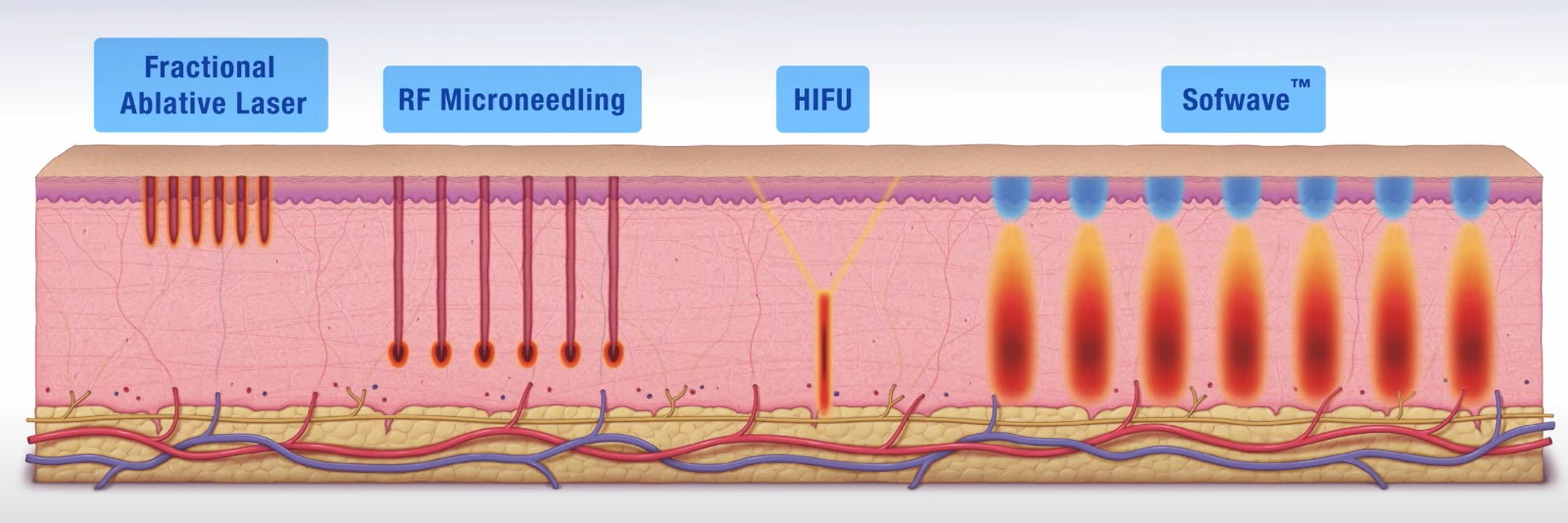

Lasers.

In the early 1990s, lasers were applied to the skin's surface to improve conditions such as pigmentation and unwanted body hair. It was discovered that ablative laser therapy, which uses a laser beam to destroy the outer layer of skin, heats the underlying layers, stimulating collagen production over time.

As expected, destroying the skin's surface is painful, and the process can be lengthy (depending on the desired outcome), often requiring multiple treatments.

In some cases (20-30%), the treatment may cause new pigmentation, a significant issue for a therapy intended to improve appearance.

Downtime can range from days to weeks for more aggressive treatments, during which patients need time to heal at home and may not be able to resume normal activities.

Sofwave’s founder, Dr. Shimon Eckhouse, who holds a Ph.D. in Physics, invented and patented what is now known as 'Intense Pulsed Light Therapy' (IPL). He went on to commercialize the technology through ESC Medical Systems, which later became Lumenis. Lumenis later IPOed and eventually was taken private.

IPL technology continues to be widely used today.

RF Microneedling.

The next technological evolution sought more effective ways to address the loss of collagen and elastin.

Unlike earlier technology that used external heat (such as lasers), the next technological evolution focused on penetrating the dermis to stimulate regeneration through small, targeted heat injuries. As the dermis heals, the new tissue generates more collagen and elastin.

As the name suggests, RF Microneedling uses numerous small needles to mechanically puncture the skin and penetrate the dermis. Once in the dermis, radiofrequency (RF) heats the needles, delivering heat injuries to both the skin and dermis - see video.

As the treated area heals, fibroblasts produce more collagen and elastin, making the skin appear firmer and tighter.

RF Microneedling technology was commercially developed by Syneron Medical, another company founded by Dr. Shimon Eckhouse, along with industry figure Moshe Mizrachi (who would later go on to establish and IPO the US-listed InMode Ltd, using the same RF Microneedling technology).

Syneron later went public on the Nasdaq in 2004, acquired Candela in 2010, and was eventually taken private by Apex Partners for $397 million.

As a private company, Candela quietly grew into one of the largest players in the RF Microneedling market. A 2022 S-1 filing revealed that they generated $322 million in revenue in 2020, approximately 50% more than InMode at the time.

RF Microneedling technology was highly successful, and today, decades later, many companies sell RF Microneedling devices worldwide.

The largest publicly traded RF Microneedling company in the U.S. is InMode (NASDAQ: INMD), which generated $490 million in revenue in 2023, at least until Candela returns to public markets.

While being a big step forward from Laser-based devices and while generating some spectacular commercial success, RF Microneedling suffers from the following issues:

-

RF Microneedling is a highly painful treatment. The patient’s face is punctured by thousands of needles, which then burn both the dermis and the skin. Some doctors have reported needing to use the same numbing protocols as in facelift surgeries. Even with aggressive numbing protocols, some patients are unable to tolerate the pain and do not return for subsequent treatments, often requesting a refund. As one doctor put it: “It hurts like hell. It's one of the most painful treatments in my clinic. In many cases, patients do one treatment and can’t continue onto the next one.”

-

As a result, selling this treatment carries significant risks: potential damage to the doctor's reputation, loss of cash flow from the treatment series (due to refunds), and the loss of future business. In an industry with high client acquisition costs, this poses a significant challenge for therapists.

-

A single treatment is rarely sufficient. Typically, a series of at least three treatments is required to achieve visible results.

-

A proper treatment often leaves the client's face bruised, sometimes requiring 2-3 days to a week of downtime for recovery, depending on the treatment.

-

The treatment can take up to 1.5 hours in total.

-

Approximately 20% to 40% of patients with skin type 3 or higher may develop hyperpigmentation, resulting in brown patches on the treated areas.

-

The range of FDA-approved indications for RF Microneedling is somewhat limited, and the aggressive nature of the treatment naturally leaves certain body areas unsuitable for treatment.

Ultrasound Therapy: High-Intensity Focused Ultrasound (HIFU).

About the time Eckhouse IPOed Syneron in 2004 scientists started exploring using High-Intensity Focused Ultrasound waves (“HIFU”) to deliver energy into the Dermis, without puncturing the skin at all.

Ulthera (now owned by Merz Aesthetics) developed the HIFU application for the skin and received FDA approval in 2009.

This treatment was considered a significant advancement, eliminating the need to insert hundreds, if not thousands, of needles into the patient’s face. As would be expected, downtime is considerably better.

For some reason, Ulthera’s IP registration in the U.S. was stronger than in other regions. As a result, Ulthera therapy, or close variations of it, are used globally by various companies, such as CLASSYS Inc. from South Korea.

While the cosmetic HIFU application introduced a significant innovation to the market, none have achieved blockbuster success, likely for the following reasons:

The HIFU technology involves delivering an energy cone culminating at a small area of convergence deep in the skin, further away from the transducer, where the therapeutic heat is generated.

At the time of development, it was considered that the most beneficial clinical results would be achieved by delivering heat deep into the tissue, where nerves and fat cells exist (this is no longer the case). As a result, the device/therapy has the following drawbacks:

-

Because a significant amount of ultrasound energy from a wide base penetrates the skin and converges deep within the tissue, a large area becomes saturated with energy. Unfortunately, this makes the treatment highly painful.

-

Because the convergence spot is small, the treatment requires many pulses of energy to cover a sufficiently large area and achieve results. This increases the treatment duration (and intensifies the pain, as noted earlier).

-

Delivering energy deep into the skin can severely irritate nerves. Without careful administration, this may result in facial paralysis and significant pain for the patient.

-

Another potential drawback of deep therapy is damage to fat cells within the skin. This type of injury, known as fat atrophy, may lead to a sagging, sunken, or 'skeletal' appearance.

Sofwave Synchronous Ultrasound Parallel Beam Technology (SUPERB™)

For the next few years post Syneron’s buyout by Apex Partners, Dr. Eckhouse set up Alon Ventures, an early-stage Venture Capital focusing on developing early-stage innovative medical device concepts into successful companies.

One of the early-stage ideas in Alon Venture involved applying ultrasound in an Endovascular device to treat hypertension. This technology later evolved into Sofwave SUPERB™.

Sofwave's SUPERB technology uses seven ultrasound transducers to heat the dermis 1.5 mm deep, reaching temperatures of 60-70 degrees Celsius, perpendicular to the skin. The energy is designed to create cylindrical-shaped thermal zones close and parallel to the skin’s surface, enabling maximal and optimal therapeutic results (one Sofwave pulse generates significantly more volume than Ulthera’s pulse), while drastically reducing the risks and pain associated with previous technologies.

At minute 22:00 into this interview (link), Dr. Eckhouse discusses the technology. At minute 23:07 Dr. Eckhouse explains the relation of SUPERB to ULTHERA. The whole interview is worth listening to. Another interview explaining SUPERB ™ can be found here.

Sofwave's SUPERB technology received FDA clearance for multiple indications, demonstrating superior safety and efficacy. In some cases, one or two Sofwave treatments can replace a multi-treatment program with RF Microneedling.

Today, Sofwave’s technology addresses a wider range of indications than other technologies. This dermatologist's statement makes this point clear:

“Neck and Jawline results for Sofwave are eye-popping. There is nothing like it. For acne scars for example: I have other treatment options. RF Microneedling works for acne. It is very painful, I would need several sessions, the patient will need a long downtime - but I have options. You need to understand that for some treatments (neck area for example) I don’t have any viable options. There are no means of treating it without Sofwave. Same with Cellulite. Same with eyelids - there is no other option. With Sofwave 1-2 treatments get the job done. Patients dislike long series of treatments.”

With no downtime, the treatment can be completed during a lunch break, making it highly accessible to busy, successful professionals with limited free time. The pain profile is so mild that I’ve met a doctor who self-administers Sofwave without any numbing cream. Very sensitive individuals may only need a modest amount of topical numbing cream.

There is no risk of hyperpigmentation.

It’s important to note that the treatment is quicker for the therapist to administer, making it more efficient in terms of throughput, in addition to all the other benefits mentioned above.

Overall, patients seem to rate Sofwave’s SUPERB ™ therapy as superior to Ulthera and RF Microneedling (as measured by InMode’s Morpheus8) per a recent realself.com site survey:

Sofwave has strong intellectual property protection, with a substantial portfolio of patents that ensure long-term patent coverage.

This video provides a convenient comparison of the various approaches and technologies discussed above.

Trying to gauge the market size.

By estimating the combined revenues of the top RF Microneedling companies, including private companies' estimated sales figures, we reach approximately $1.5 billion in annual revenue, with most of it coming from capital equipment sales. Public documents suggest there are many more than 60,000 RF Microneedling devices as installed base around the world.

Some studies, including Markets & Research, estimate that the energy-based aesthetic device category is currently valued at nearly $4 billion and is projected to grow to $8 billion by 2028, with a low double-digit CAGR. Additionally, the number of global annual treatments could exceed 100 million.

While 2024 appears to be a challenging period for the entire industry, I expect Sofwave to outperform the market by disrupting competitors and gaining market share. This suggests that future growth rates could accelerate to the mid-to-high teens over the next several years, if not higher.

In summary, the market is substantial and experiencing secular growth, driven by the following factors:

-

Aging demographics are expected to drive increased demand for aesthetic treatments, while Millennials are seeking procedures earlier to preserve their youthfulness,

-

Rising wealth and disposable income, particularly in the APAC region, are driving increased demand,

-

Social media is increasing the emphasis on appearance and normalizing cosmetic procedures,

-

Aesthetic chain businesses and medical aesthetic spas (Medspas) are experiencing growth,

-

The service provider base is broadening, with non-dermatologists seeking to diversify and expand their practices,

-

Increasing public awareness of non-invasive treatment options is driving demand,

-

The growing popularity of GLP treatments, which can result in loose skin (the 'Ozempic look'), is driving demand for treatments and procedures to address this side effect.

Management.

Sofwave's C-suite management team includes veterans called back by Dr. Shimon Eckhouse (79), such as Lou Scafuri (former CEO of Syneron Candela, 72), Assaf Korner (former Syneron Global VP of Finance, 49), and James Bartholomeusz (former CTO of Lutronic and VP of Product Development at Syneron-Candela, 42), along with other key staff. This leadership team brings many years of experience and deep familiarity with industry key opinion leaders (KOLs) and important contacts.

Multiple interactions with management have underscored the team's deep industry expertise and proven track record of operational success, which is uncommon for companies with such low market capitalizations.

Dr. Eckhouse is the largest shareholder in Sofwave, holding a 24.8% stake, giving him significant skin in the game alongside other shareholders.

Financials.

From 2020 revenues increased by more than tenfold: from $4.2 million to over $50 million in 2023.

In 2020, revenues from Pulse sales were negligible due to the lack of an installed base. However, with the placement of devices, Pulse sales grew to nearly $13 million in FY 2023 and $10.7 million in the first half of 2024, with a very likely annual run rate exceeding $20 million, representing an 8X increase since 2021. Year-over-year, Pulse revenues nearly doubled in the first half of 2024.

Notably, while many competitors are struggling with high interest rates and attributing a roughly 50% drop in sales to 'cautious consumers' (NASDAQ:INMD, NASDAQ:CUTR), Sofwave grew by 22% in the first half of 2024, maintaining steady capital equipment sales despite the downcycle.

In the second quarter of 2024, Sofwave's pulse revenue grew by over 80%, while competitors experienced a decline in consumable revenues (NASDAQ:INMD down 2.6% and NASDAQ:CURT down 40%).

Sofwave's gross profit consists of Pulse sales at a 100% gross margin and capital equipment sales at around 65% gross margin. Currently, the overall gross margin stands at approximately 75% and could increase further with the growth of Pulse sales as the installed base expands.

Operating expenses consist of R&D at 23% of revenues (FY 2023), S&M at 55%, and G&A at 12%.

Looking ahead, the expense percentage of revenues is expected to decrease as sales grow, with estimates of R&D at 10%, S&M at 40%, and G&A at 10%, resulting in an EBIT margin of approximately 15%.

A key question for investors is whether business-building expenditures, such as R&D and S&M at this stage, should be viewed as expenses or investments in the company's future, particularly when they contribute to long-term growth, such as an expanding installed base generating Pulse revenue and driving innovation.

When considering expenses in terms of growth versus maintenance, I estimate a maintenance-only budget to be around 45% of revenues today, which would result in approximately 30% EBIT baseline on a maintenance expenditure only today.

Although currently a loss-making, cash-burning business (-$8.26 million loss in FY 2023), the inflection point to profitability appears to be just around the corner. Management has guided toward cash flow break-even in FY 2024, despite a challenging climate for competitors. It is expected that most of the contribution will come in the fourth quarter due to seasonality (Q4 being the strongest, followed by Q2, with Q1 and Q3 slower).

Sofwave's cash from operations was negative $2.9 million during the first half of 2024 (compared to negative $5.9 million in 1H 2023), but the company has ample cash ($21 million) on the balance sheet to transition to profitability.

As of June 2024, the average number of outstanding shares is 34,324,169.

Valuation & Financial Expectations.

Sofwave's enterprise value is $146 million. What are we buying?

While Sofwave has not yet disclosed its installed base numbers, I estimate there are approximately 1,380 devices as of June 2024.

Assuming each device is used 2.5 times per week, this would result in over 135,000 treatments annually (assuming a net 10 months per annum).

With an average of 110 pulses per treatment at $1 per pulse, this results in a pulse revenue run rate of approximately $15 million, before accounting for additional device sales, an expanded installed base, or improvements in pulse yield.

At an enterprise value of $146 million, this translates to approximately 10 times EV/recurring pulse revenues.

Adding just half of 2023 device sales (approximately $37 million) brings total revenues to around $33 million, or about 4.5 times EV/revenue.

Take private valuations.

When Zeltiq was acquired by Allergan for $2.475 billion, it was generating approximately 55% of its $354.2 million in revenue from recurring consumable sales ($194.81 million).

On a price-to-recurring-revenues basis, this equates to 12.7 times recurring revenue and approximately 7 times total revenue, which can be attributed to Zeltiq's profitability and faster growth rates at the time of the transaction.

Ulthera was acquired by MERZ in 2016 at a multiple of 6 times revenue, including capital equipment and pulses.

Based on these data points, one could argue that Sofwave is currently trading at a discount to its takeout valuation, providing a solid and continuously widening margin of safety.

What is the upside?

In a mediocre scenario that does not account for significant traction in APAC (Japan, China), Europe, does not foresee any increase in traction with incremental buyers (such as Medispas and other non-dermatologist or plastic surgeons), ignores gross profit expansion driven by recurring pulse growth or and factors in a very modest increase in device usage, the results could look something like this:

Using 6 times EV/revenue (takeout valuation) by 2026 could result in a market cap approximately twice that of today’s within 2.5 years (above 30% CAGR), offering reasonable returns while allowing for a discount rate and some stock dilution keeping in mind the approval from Japan could literally land any day now.

Considering the conservative assumptions mentioned above, I’m reminded of Benjamin Graham’s famous quote: 'You don’t have to know a man’s exact weight to know that he’s fat.' Similarly, we don’t need much more to conclude that Sofwave stock is undervalued and likely to meet the IRR expectations of even the most discerning investors.

After spending considerable time speaking with and assessing management, as well as conducting extensive on-the-ground research, and noticing how competitors' sales talent are defecting to Sofwave in the US, I believe Sofwave's performance will likely exceed these expectations.

Even without excessive optimism, shareholders are likely to be handsomely rewarded at the current price point. In a potential future scenario where Sofwave has an installed base of 6,000 devices, U.S. annual sales reach 500 units, and each device is used an average of 3.3 times per month, the company could support a revenue run rate of over $120 million, along with significant operating leverage from Pulse recurring revenues. This would drive an EBIT margin above 30% and support a premium valuation of $700 to $800 million in market cap or a higher potential buyout offer within 5 years.

It will be interesting to see how the Sofwave story unfolds.

Reason for current valuation.

Sofwave was listed on the TASE stock exchange in Israel in 2021, during an IPO wave that included some questionable businesses seeking liquidity, often referred to by local traders as “The 2021 screwups”. The early-stage listing was driven by the opportunity to access cheap funding at high valuations during the free-money, pre-2022 era. The listing funds funded the early stages of Sofwave’s journey, likely as the only public raise as a public company.

Currently, local Israeli traders' sentiment is poor, with deep skepticism, though this is starting to shift with improved results and execution, as reflected in the stock chart.

Sofwave suffers from Orphan Stock syndrome: Local Israeli traders have a strong home bias and are often reluctant to research global companies. They tend to evaluate businesses through local valuation lenses and exhibit a justifiable distrust for inexperienced Israeli founders with global aspirations. For some reason, the fact that this management team has successfully executed this playbook twice before is overlooked. Conversely, global investors do not expect to find a high-quality global business on the local stock exchange and face language barriers when it comes to discovering, researching, and even purchasing these stocks, until the matter is brought to their attention.

The few Israeli analysts who have reviewed Sofwave as part of a brute force scan approach have often conducted shallow assessments, concluding that 'Sofwave is just another commodity capital equipment seller, and unprofitable too—hard pass.' The lack of competent analyst coverage makes it difficult for the public to recognize the value at hand.

Sofwave is often mislabeled as an 'InMode copycat,' with global bankers viewing it as 'another InMode.' Consequently, Sofwave faces criticism for not attaining the same high valuation in Tel Aviv as InMode on Nasdaq during InMode's prosperous periods, and when InMode's business faces challenges, Sofwave is unjustly assumed to warrant a similar lower valuation, even when its business model is stronger and results are better.

I believe that all of the issues mentioned above will resolve over the next 24 months with continued business execution, a transition to profitability, and a NASDAQ listing, along with enhanced investor relations activities targeted at global investors, which are already underway.

Catalysts.

Several catalysts are expected to increase valuation and enhance price discovery:

-

Business execution: Sofwave is expected to break even on a cash flow basis in 2024, reducing balance sheet risk. Increased sales traction and a shift into profitability should attract more attention.

-

Deeper APAC penetration: In the second half of 2024, Sofwave is likely to secure regulatory approval in Japan and commence sales of devices and pulses. China is expected to follow in 2025 or 2026. Full penetration into the APAC market is anticipated to drive significant growth and substantially boost cash flows.

-

NASDAQ listing: Sofwave management plans to pursue a NASDAQ listing within the next two years. This move will overcome language barriers, improve market communication (guidance), and attract a global, more sophisticated shareholder base.

-

Discovery: IR efforts designed to tell the story to the correct audience are beginning in preparation to the NASDAQ listing with early Family Offices, US and European funds already establishing positions. I estimate the story will be much better known, followed and understood in 6 months with commensurate rerating.

Risks.

-

Product Acceptance: If Sofwave's clients fail to recognize the superiority of its solution, the company may experience subpar growth and miss the market opportunity. However, the initial feedback from clients and doctors using the product has been overwhelmingly positive, mitigating this risk.

-

Management Execution: Mediocre execution at this early stage could lead to slow growth, subpar financial results, and hinder Sofwave's ability to become a major player in the industry. However, this risk is reduced by management's proven experience in successfully executing similar strategies twice before, along with their achievements to date.

-

Management Capital Allocation: Misallocation of capital—whether through substandard M&A, ineffective R&D or marketing investments, or unnecessary dilution—could significantly undermine future value. However, based on multiple conversations with management and the founder, I believe the risk of capital misallocation in a way that would be detrimental to shareholders is limited.

-

Geopolitical: Sofwave, like other businesses in the industry, is based in Israel. While it may benefit from a stronger USD relative to ILS exchange rates (revenues in USD, expenses in ILS), prolonged disruptions to business operations in Israel could necessitate the re-establishment of supply lines, incurring additional costs. As mitigation, Sofwave holds sufficient inventory outside of Israel and has prepared the business to operate under extreme conditions. Additionally, at least three members of the C-suite team reside in the US.

-

Economy: Prolonged consumer economic stress could negatively affect demand for discretionary services, such as aesthetic procedures. An adverse economic environment (e.g., higher interest rates or a sharp economic downturn) could lead to fewer transactions. However, based on competitors’ financial reports, this impact is already occurring, with Sofwave showing limited effects, potentially due to its smaller size and ability to capture market share with its superior solution and competitive pricing.

-

Key Man Risk: With a 79-year-old founder and a 72-year-old CEO (who has retired four times), the question of succession naturally arises. For now, the experienced and highly capable management team is an asset. The C suite includes two younger executives with very deep industry roots, connections, and familiarity with the industry. Additionally, Sofwave has a sufficiently deep bench of talent ready to step up if necessary. As the business continues to grow and mature, reliance on key individuals will diminish, allowing for a smooth transition.

-

Technological Obsolescence: At some point, new technology will inevitably replace Sofwave’s SUPERB™. However, history suggests that such advancements are unlikely to completely displace the incumbent, particularly regarding pulse revenues from the existing installed base and to make a dent would need to offer even better value proposition - quite a feat and a long way away, for now. With Sofwave, we are still in the very early stages of this product cycle, possibly with more than a decade ahead of us.

Notice: This is not an offer to buy or sell securities, I have a long position in this company & may trade it.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Several catalysts are expected to increase valuation and enhance price discovery:

-

Business execution: Sofwave is expected to break even on a cash flow basis in 2024, reducing balance sheet risk. Increased sales traction and a shift into profitability should attract more attention.

-

Deeper APAC penetration: In the second half of 2024, Sofwave is likely to secure regulatory approval in Japan and commence sales of devices and pulses. China is expected to follow in 2025 or 2026. Full penetration into the APAC market is anticipated to drive significant growth and substantially boost cash flows.

-

NASDAQ listing: Sofwave management plans to pursue a NASDAQ listing within the next two years. This move will overcome language barriers, improve market communication (guidance), and attract a global, more sophisticated shareholder base.

-

Discovery: IR efforts designed to tell the story to the correct audience are beginning in preparation to the NASDAQ listing with early Family Offices, US and European funds already establishing positions. I estimate the story will be much better known, followed and understood in 6 months with commensurate rerating.

| show sort by |