| 2023 | 2024 | ||||||

| Price: | 2.50 | EPS | n/a | n/a | |||

| Shares Out. (in M): | 158 | P/E | n/a | n/a | |||

| Market Cap (in $M): | 395 | P/FCF | n/a | n/a | |||

| Net Debt (in $M): | -89 | EBIT | -35 | -10 | |||

| TEV (in $M): | 306 | TEV/EBIT | n/a | n/a | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- QUEST DIAGNOSTICS INC DGX 08/09/2019

Description

Standard BioTools (LAB US)

Investment Summary

Standard BioTools is a small-cap life science tools company that presents a compelling opportunity to invest in best-in-class technology in a large and growing industry with limited downside.

In the past, the company (formerly known as Fluidigm) was operationally and commercially mismanaged. In 2021, the business saw an activist engagement pushing for a strategic change, and in 2022 was re-capitalized by investors, who also brought in a strong and highly experienced management team to bring the struggling firm to profitability.

We believe LAB has long been misunderstood by the investment community due to the former management’s operational missteps and divergent trajectories of the business divisions. However, after just one year under new leadership, the company is already showing signs of progress on multiple fronts. It now presents a uniquely attractive case in the small-cap life science sector of a well-capitalized enterprise with a clear path to positive FCF and a number of near- and medium-term catalysts.

In our base case, we see Standard BioTools fetching $1b+ valuation on $200m+ sales by 2026 as a strong niche player in the $7b+ directly addressable high-plex segment of the proteomics market, implying 2-3x investment return in the next 3 years.

On the downside, we see the current valuation of ~$350m EV (treating convertible preferreds as debt) on ~$100m sales at around a floor level, supported by existing high-margin recurring consumables and services revenue of ~$80m, and believe LAB’s acquisition will be easily digestible by strategics if the company fails to execute its growth strategy.

Situation Overview

The company has existed in various iterations since 1999. Now called Standard BioTools, it operates two business lines: one, accounting for ~$60m of current sales, focuses on the fast-expanding and highly promising field of proteomics. This is the study of proteins and how they function in cellular processes, which provides critical insights into the understanding of disease. It does this using mass cytometry, powered by LAB’s best-in-class proprietary CyTOF technology.

LAB’s second business line, accounting for ~$40m of current sales, focuses on genomics, or the study of an organism’s genes expression. It does this through microfluidics, which enables the manipulation of small volumes of fluid in a precise and automated high-throughput manner.

Historically, management and investors focused on the microfluidics division of the company – hence its old name, Fluidigm. Although this division saw a brief and unsustainable bump during the pandemic because it allowed for high-throughput COVID testing, microfluidics is a highly competitive, commoditized space that is dominated by larger players. This declining division has, in the past, obscured the highly promising mass cytometry side of the business, which is in a higher growth market with much more upside potential and a stronger competitive advantage, despite this previously suffering from underinvestment.

The company has endured a torrid time recently, hit by a series of operational and corporate issues (amplified by global supply chain problems during the pandemic) and poor management decisions. In 2021, the company saw activist investors pushing for a strategic change and it subsequently proceeded with a $255m financing deal with the large biotech investors Casdin Capital and Viking Global. The deal, which completed in April 2022, also saw a management overhaul, with Casdin Capital bringing in its management team headed by the new CEO, Dr. Michael Egholm, who was formerly CTO at Danaher Life Sciences and led Pall’s biopharmaceutical division before that. The COO Alex Kim was previously at Pall, as was board member Martin Madaus, while board member Frank Whitney was in charge of the Affymetrix turnaround from 2011 and before that the CEO of Dionex.

This strong team of experienced life science players has a proven track record of commercializing technologies and is incentivized mostly by stock options (with a $4/sh strike price). It is now actively turning the company around and pursuing a new strategic direction. This involves downsizing the microfluidics side of the business, allowing it to squeeze stable and low growth profits from attractive but small niche applications, and focusing on mass cytometry – a strategy symbolized by the name change to Standard BioTools. LAB’s best-in-class proprietary CyTOF technology has demonstrated its high growth potential (~30% CAGR in 2016-2019, pre-COVID) and has a clear lead in data quality over conventional flow cytometry (as we discuss in detail below). There are no other scaled competitors offering similar high-throughput, high-plexity profiling at single cell resolution level in proteomics.

Apart from strategically realigning the business with its strongest parts, and closing previously glaring commercial execution gaps, the new leadership team has also been focused on trimming the cost structure and implementing the lean production ethos Egholm learned at Danaher. The strategy is starting to bear fruit, with clear progress on the cost side and mostly subtle signs of commercial execution success.

So, why invest in LAB now?

-

The new strategy creates a much larger TAM

A core tenet of the new strategy is moving the client base from an academic niche to cater for a much bigger TAM. In proteomics, Standard BioTools has finally launched clinical-grade instruments that should turn it from a research-advancing company with a sub-scale revenue base and bloated cost structure to a fully-fledged commercial platform straddling applications from academic and research labs to contract research organizations (CROs) and clinical settings. New and more attractive equipment offerings should drive not only re-acceleration of instruments sales to 20%+ growth for the next 3-5 years but also bring in up to 2x higher consumables pull-through coming from increased utilization.

In microfluidics, the company has radically narrowed its product offering to just one device with an attractive value proposition for niche markets. It has also been implementing an OEM partnership with Olink, using its microfluidics technology in Olink’s Signature Q100 system. As a result, microfluidics has broken even on a segment operating profit level and is expected to become a positive contributor with broadly stable device sales and a high share of consumables.

-

The strategy is already starting to bear fruit

We believe the new management team has been executing well for over a year now and can already start to see real signs that the turnaround is working – they have reduced the opex base by ~25% or $35m annually, and coupled with the operating leverage on growth, LAB should achieve positive FCF by Q4 2024; until then Standard BioTools has ample liquidity of $155m cash available against just $15m current quarterly cash burn rate. This is setting the stage for big operating leverage and means LAB is already a more derisked opportunity that still offers 2-3x potential upside.

-

LAB has better tech than its competitors

We explore LAB’s offering in more detail below, but the new management’s plan is to harness the value of its superior tech. The company acted upon early customer feedback and upgraded CyTOF XT to make it more accessible and reduce the setup time; the same learnings were applied to Hyperion XTi imaging system, the first device developed under Egholm’s leadership, launched in April 2023, and we see a catalyst-rich path forward for the stock as the company rolls out its new generation of instruments.

Investing now means we can get in ahead of inflection with some near- and medium-term catalysts coming up. When combined with the recent sell-side coverage of the stock, educating investors on the new and improved LAB, this makes for a very exciting investment opportunity.

Mapping proteins – from $7b to $12-20b directly addressable market in the next 3-5 years

Understanding the organization of cells and tissues and how this influences function is a fundamental pursuit in life sciences research and proteins provide highly valuable insights. Proteins perform a vast array of functions within living organisms, including catalyzing metabolic reactions, replicating DNA, and transporting molecules from one location to another.

While there is one genome for all cells in each organism and ~20k protein-encoding genes in humans, proteins change dramatically according to the organism and the conditions present (age, cell cycle, cell-to-cell interactions, etc.) and there are over 1m protein variants in every human. Protein analysis is required to profile and understand cellular function as well as the interaction in tissues and other complex microenvironments. Analysis identifying multiple protein types (multi-plex) at the single-cell level is essential to understand these complex systems.

There is growing demand for high-dimensional (or high-plex) cell analysis and solutions that can provide a complete picture of cellular biological processes and interactions. The market for single-cell proteomics – addressed by LAB’s CyTOF XT device – is estimated at above $3b currently and growing around 5% annually. We expect LAB to take share from the legacy technologies as it expands from academia and research labs using CyTOF for discoveries to CROs and pharma, which can translate discoveries into innovative drugs and validate clinical trial outcomes with CyTOF.

Further, preserving spatial context is useful when the spatial distribution of cells and the signaling between them is biologically relevant – a major use case is in assessments of tumor microenvironments and how they change in response to therapies. This cutting-edge research market for spatial proteomics –addressed by LAB’s Hyperion XTi device – is estimated at above $4b currently and growing 15-20% annually with the potential additional upside of $5-10b from clinical applications in the next 5 years. Hyperion XTi is a next-generation imaging system with 5x the speed and an unmatched signal detection level to quantify and visualize the tissue microenvironment. It can image 40+ parameters simultaneously to give faster results and co-detect protein and RNA for deeper insights.

In our base case we assume that the new generation of devices will help LAB nearly double its installed base over the next 4 years with only modest incremental adoption outside of its current core customer base. However, given that there’s currently no close competitor doing spatial single-cell proteomics with 40+ plexity, we estimate in our bull case that LAB can 10x its adoption and eventually take 15-20% of this market.

Why LAB should win market share in proteomics

Currently, proteins are mostly detected by legacy mass spectrometry (protein identification by mass), immunohistochemistry (marking proteins by optically identifiable fluorophores), and more recent bulk and spatial transcriptomics (encoding proteins by RNA). However, all these technologies face impossible trade-offs between data quality, resolution, and throughput.

-

When applied at a single cell resolution, mass spectrometry is a slow, low throughput, and prohibitively expensive method. Most of the instruments in this field are provided by large conglomerates, such as Thermo Fisher (TMO) or Bruker (BRKR).

-

Immunohistochemistry is a simple, low-plex and low-cost technology that can reliably look at 1–3 markers. Due to the low number of markers per scan it takes a significant amount of time and resources to attain the same insights higher-plex imaging can provide in one go. Using the same principle as immunohistochemistry but more advanced methods, fluorescence-based cytometry has significantly progressed over the past 5 years and can be efficiently applied at a single cell level. However, due to fluorescence spectral overlap it is physically limited by 5-20 parameters or biomarkers it can detect in one run. The leading fluorescence-based proteomics competitors are Cytek (CTKB), Akoya (AKYA) and IsoPlexis (recently acquired by CELL).

-

Bulk transcriptomics allows scientists to look at tens of thousands of parameters at a low cost, but loses sensitivity, resolution, and any spatial information. In turn, spatial transcriptomics is even more costly and has limited cellular resolution. As a result, proteomics is outside of the core focus for 10x Genomics (TXG) and Nanostring (NSTG) instruments’ applications.

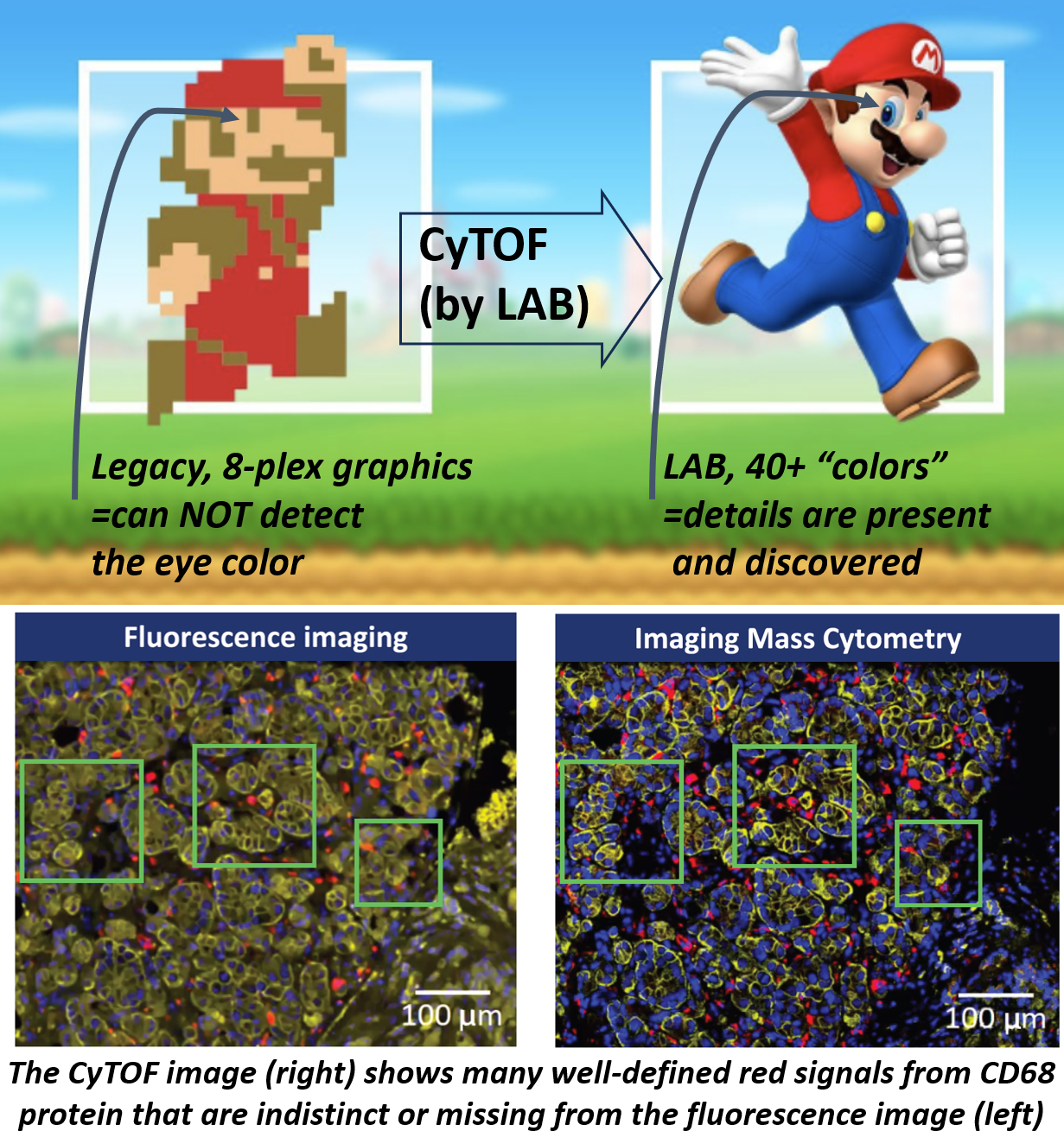

In 2014 LAB acquired DVS Sciences, the original inventor of Cytometry by Time of Flight (CyTOF) technology, for $208m and has since invested around $200m in CyTOF R&D. CyTOF’s unique difference from the above-mentioned traditional flow cytometry methods is using heavy metal isotope labels rather than fluorescent labels for detection of proteins. As CyTOF technology is practically limited only at around 60 parameters, it effectively unlocks a disproportionally higher number of insights, improves the sensitivity of the tests, and implies lower cost per biomarker detection, while it can also maintain spatial context. The new CyTOF XT can interrogate more than 50 labels simultaneously on millions of individual cells.

By analogy, if proteins imaging were a videogame, LAB advances technology from 8-bit pixelated (8 colors plex) Mario to modern-age graphics – previously it had been impossible to tell the color of Mario’s eyes. In LAB’s case, CyTOF allows the detection of previously hidden or indistinct biomarkers, such as CD68 on the picture below. In this example, some patient cases might not clearly show the presence of CD68 on the images due to their low quality or visibility issues caused by the lack of LAB instruments. This situation could lead to potential misdiagnosis of diseases, misunderstanding their mechanism of action, and/or incorrect determination of treatment.

LAB has established a solid presence in academia and in research labs (capturing around 20% of this directly addressable market share). The difficulty in moving to CRO and commercial labs has been primarily high cost, low automation (high manual labor time), and low speed of data acquisition for LAB’s previous generation of instruments. Despite these limiting factors, LAB became the go-to instrument to use for high-plex studies, as evidenced by the quickly growing number of publications and clinical trials:

-

Of more than 1,850 publications with 20 or more protein markers, 96% used mass cytometry or CyTOF by LAB. This roughly matches the combined total of all publications for low-plexity fluorescence peers (CTKB, AKYA and ISO).

-

Imaging Mass Cytometry (IMC by LAB) in spatial proteomics currently features in over 200 publications and is growing over 50% annually.

-

Adoption of CyTOF and IMC-measured outcomes in clinical trials reached over 200 trials, with an accelerated need for the instruments expected for clinical results validation as studies progress to the next phases.

The new CyTOF XT and Hyperion XTi are up to 5x faster than previous instruments, automated for minimal hands-on operator time, have almost 2x lower footprint and are, overall, much more convenient tools for high-throughput operations such as CROs and bio-pharma. Hyperion XTi is currently the only available high-resolution spatial proteomics tool allowing as fast as a 40-minute turnaround per slide. Moreover, LAB takes exceptional care of servicing customers with pre-designed protein biomarkers and test panels to save customers time and costs on their own research and test trial efforts.

Finally, our cost analysis below shows that the new generation of LAB tools effectively more than halves the experiment costs per sample and are now directly comparable to Akoya, while producing much higher-quality data.

The comparative analysis with lower-plex instruments demonstrates latent potential for LAB to re-accelerate its installed base growth once customers adopt the new generation of devices. CTKB, AKYA, and ISO have all been rapidly adopted by CROs since 2021 while LAB was dealing with its internal manufacturing struggles and corporate changes. We expect LAB to catch up now with the roll-out of the new devices, including Hyperion XTi.

In all, we believe LAB will likely take share from the current legacy instruments and should be able to significantly outgrow the market. That said, in our base case we assume only modest adoption of the new generation of devices accounting for the industry inertia of CRO and biopharma. We also attribute zero value to LAB’s potential in diagnostic/clinical applications that alone could generate ~$1b in consumables annually if adopted to ~2m screening tests (at $500/sample cost accounting for higher volumes) for the cases that currently lack sufficient sensitivity. For example, the recent research by Zhejiang PuLuoTing scientists in China (enrolling over 2,000 participants) demonstrated that CyTOF-detected cell markers significantly improved the current standard test sensitivity for hepatocellular carcinoma (HCC) and pancreatic ductal adenocarcinoma (PDAC) in humans.

Microfluidics – right-sized for low and stable profits

Microfluidics is a high throughput technology based on miniaturization of fluid flows and massive parallel processing. LAB previously led the market with its Biomark HD platform, which was later disrupted by lower cost next-generation sequencing (NGS) and polymerase chain reaction (PCR) devices from much larger competitors. However, the new management has refocused LAB’s microfluidics on a two-pronged strategy.

First, it now focuses on niche applications that feature highly precious samples, require expensive treatment reagents, or niche customers such as small labs that are looking for all-in-one solutions instead of a full bench of best-in-class devices.

Second, LAB now provides OEM services and manufactures devices that are being designed, marketed, and distributed by partners such as Olink. Importantly, while these device sales are low-margin for LAB, the accompanying consumables sales are high margin and recurring.

Since the start of the partnership in 2021, Olink has grown its Signature Q100 placements quickly with 26 new placements in Q1 2023, expanding the total installed base to 117. If Olink continues its growth trajectory we estimate that by Q1 2024 LAB can benefit from around $10m of additional consumables sales per year, or 25% of current total microfluidics revenue, with a gross margin of ~80% and no incremental SG&A. This growth will be partially offset by fading legacy Biomark usage and consumables pull-through. Going forward, the company is targeting one additional OEM partnership annually.

Financials and valuation – asymmetric risk/reward

LAB is expected to generate above $100m in sales in 2023 with gross margins above 65% by the end of the year. The new leadership team has reduced costs and focused on efficiency leading to opex of $105m in 2023, which is expected to remain broadly flat (barring M&A). With growing revenues and flat opex, we expect the business to reach FCF profitability by late 2024 riding the growth in proteomics and operating leverage.

In the longer-term, by 2026-2027 we expect microfluidics to maintain a stable 10% operating margin on ~$50m sales, while mass cytometry should scale from the current $60m to ~$180m sales and reach above 20% operating margins supported by high gross margins due to the differentiated positioning of LAB in proteomics. On a consolidated basis, in our base case we estimate the company to generate $40-50m EBITDA by 2026-2027 growing top-line at 15%+ and offering further potential for margin expansion on the back of continuing market penetration in mass cytometry. Applying a reasonable 20-25x EBITDA multiple for this financial profile we arrive at our target $1b+ valuation translating to $6-7/sh by the end of 2026. Importantly, we see limited competition to LAB’s CyTOF technology and expect strong scientists’ standards and installed base network effects to protect LAB’s moat, and margins, for decades to come, implying potentially much larger upside than our base case.

On the downside, we see the current valuation of ~$300m EV on ~$100m sales at around a floor level. The current share price of $2.5/share (incl. $0.6/sh net cash on as-converted prefs basis) is ~25% below implied valuation level at re-capitalization (prefs conversion strike price of $3.4) and further downside is protected by the existing $75m recurring consumables sales at 80% gross margins requiring minimal ongoing sales or R&D efforts. Applying both a punishing 5x recurring gross profit multiple and assuming another two years of FCF burn we see a cumulative 40% downside to $1.5/sh and believe a $300m EV price tag would be easily digestible by strategic suitors.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

-

Increasing installed base of mass cytometry devices driven by new instruments roll-out;

-

Q2 2023 – first quarter with complete roll-out of new devices lapping weak Q2 2022;

-

Continued strong placements of OEM-partnered Olink Signature Q100.

-

Delivering on FCF targets expecting to break even in 2H 2024;

-

Value-accretive M&A extracting SG&A + R&D synergies;

-

Increased sell-side coverage.

| show sort by |