| 2024 | 2025 | ||||||

| Price: | 21.22 | EPS | 2.53 | 0 | |||

| Shares Out. (in M): | 57 | P/E | 8.4 | 0 | |||

| Market Cap (in $M): | 1,211 | P/FCF | 8.4 | 0 | |||

| Net Debt (in $M): | 481 | EBIT | 47 | 0 | |||

| TEV (in $M): | 1,692 | TEV/EBIT | n/a | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- Union Auction AUCT 07/18/2023

- PEAKSTONE REALTY TRUST PKST 07/11/2024

Description

Elevator pitch

Sila Realty Trust (Sila) is a triple net lease healthcare REIT primarily focused on owning medical office buildings (MOBs). Despite a high quality real estate portfolio and an under-levered balance sheet, Sila trades at a 10.6% implied cap rate and only 8.4x ‘24e FFO. At peer-level leverage Sila’s FFO multiple falls to 7.3x vs. peers at 10.9x. Further, REITs are out of favor and peer group valuations are at all-time lows. With a strong lease profile, low leverage, and an attractive valuation, we think the risk here is well below average. We see ~60% upside with optionality to 100% if interest rates return to pre-Covid levels.

We think unique trading dynamics (explained below) have resulted in this attractive valuation and a re-rating in the short-term is possible.

Description & Background

Sila was founded in 2013 as a public non-tradable REIT. From 2013-2019 they raised capital and acquired properties healthcare properties as well as data centers. In 2021 they sold their data center business, paid down debt and paid out capital to shareholders. They are now a pure-play healthcare REIT. They own 136 properties across several healthcare property sub-types -the types that typically exhibit above average growth via low patient costs such as outpatient facilities, surgical centers, etc. Notably, they do not invest in higher cost settings like senior housing, skilled nursing, or general acute care hospitals. Specifically, their exposures are:

% of ABR (annualized base rent)

37% Medical office buildings

34% Specialty and surgical centers

29% Inpatient rehabilitation

Sila owns both on-campus and off-campus facilities that are generally close to tenant patient referral sources such as hospitals or are in MOB clusters. They target geographies with dense populations that exhibit at or above average growth. Tenants are generally market leading providers with dominant market share. Sila puts particular emphasis on tenant financial health and rent coverage ratios. Leases are high quality, described in more detail below.

Near-term Trading Catalysts

-

Sila is newly public with little following. Sila was previously a non-traded REIT (it was technically public - they filed with the SEC, etc. but did not trade). They listed on the NYSE on June 13th, 2024 and became tradable then. Prior to going public they had 60,000 investors that essentially had no liquidity. They now have liquidity for the first time and we would guess there are quite a few hitting the bid, taking advantage of the long-awaited liquidity. This selling has likely put pressure on the stock right out of the gate. In anticipation of this selling pressure Sila announced a $50MM Dutch Tender on listing day (5% of shares). The Dutch tender is currently in effect with a price range of $22.60 - $24.00. (For the beer money crowd there is odd lot priority here with an odd lot tender offering a near guaranteed $120 profit on 99 shares by the July 19th expiration, a 5% return in 10 days). The tender could also be creating some short-term arb demand, so we may get a little choppiness the next couple of weeks.

-

Sila came public via direct listing, so it didn’t get the normal investment banker marketing and road shows that come with IPOs. Sell-side coverage and investor relations activity is likely right around the corner.

-

Importantly, they are very under-levered. As they increase leverage their FCFE and equity value should benefit materially. They recently made a $125MM acquisition with just cash on the balance sheet. We expect them to put their debt capacity to work in M&A, resulting in attractive FFO growth.

-

It will likely get added to indexes.

Sila is a High Quality REIT

Sila has very low leverage for a REIT with only 3.0x debt/EBITDA vs. 5.9x for its peer group. Net debt/assets is only 23% vs. 46% for peers and interest coverage is 7.4x. Further, 100% of debt is fixed and 100% of assets are unencumbered.

Tenant leases are clean and simple, characterized by:

-

Long-term (typically 10-15 years) with a weighted avg. remaining lease term of 8.4 years vs. peers at 5.8. Only 17% of rents mature in the next five years resulting in visible, durable income streams.

-

Triple net - 99.9% of Sila’s leases are triple net vs. peers at 79.1%. This results in minimal capex and excellent FCF with 90% property level EBITDA margins. Further, tenants are more likely to renew upon lease expiration because the cost to build-out an MOB is relatively high so tenants don’t want to walk away from their investment.

-

Single tenant - 91% of ABR are single tenant leases, generally resulting in a long-term lease with low/no vacancy.

-

Contractual rent increases - 83% of rents have contractual escalators averaging 2.2% with the remaining tied to CPI, resulting in low but highly visible FFO growth.

Sila’s lease rates have consistently approached ~100% vs. peers at 92.5%, and over 99% each of the last five years (below is last five quarters).

Source: Sila NAREIT presentation

Sila has high quality tenants with strong rent coverage, averaging 4.7x for the 70% of tenants with reported financials. Credit quality for the types of healthcare facilities Sila owns are typically much higher than other healthcare REIT sub-types:

Source: Healthcare Realty Trust 4Q23 earnings presentation

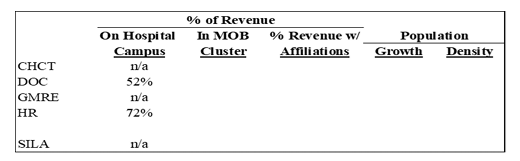

Sila is pretty well diversified. They have 169 leases across 136 properties. They have one client greater than 10% of ABR (discussed in the risk section). The largest geographical concentration is The Woodlands, Texas, at 10.2% of revenue.

Under-levered

Sila is meaningfully under-levered, which is a key part of the thesis. We think they are following a logical REIT playbook. FFO growth is a big driver of REIT valuations so the playbook is:

-

Come public with tons of dry powder to drive inorganic growth via M&A. Check.

-

FFO growth, upward revisions, a strong balance sheet, and durable FCF lead to an above avg. valuation.

-

A good valuation equals a good currency for further M&A. REITs love that.

We fully expect management to bring leverage up to peer levels. With the cost of debt well below ROIs further leverage will be accretive to cash flow. We take a look at what this may look like below.

Valuation

Let’s go through some return scenarios using traditional REIT valuation metrics and current peer valuations. Below is a chart showing Sila and peers on NTM P/FFO. The bold red line is the 10-year Treasury yield inverted. You can see 1) how highly correlated valuations are to interest rates, 2) how much they have derated since rates began to rise during Covid and 3) how cheap Sila is vs. its peers (Sila is that tiny little line at the bottom right).

Source: Factset

And here on NTM EV/EBITDA. Sila is on an island unto itself.

Source: Factset

A good starting point is to consider a simple re-rating to peer levels which would provide a ~40% return, not super juicy but adequate imo given the below average risk and the potential for a re-rating in the near-term.

While it is easy to envision a re-rating to peer levels to get a ~40% return, we also think it is easy to envision a re-levering to ~peer levels where we get much higher returns. Illustratively, if we lever Sila up from 3.0x to 5.0x debt/EBITDA and use the proceeds to buy back stock at $23, it drives proforma ‘24e FFO/share from $2.53 to $2.91, or 15.1%. At peer level valuation on the proforma numbers we get upside of $31-32, or a ~60% total return.

But even after re-leveraging Sila we are left with an apples-to-oranges comparison to peers because, we believe, Sila is higher quality for all the reasons previously mentioned…

Is a 5% premium to peers too much to ask?

~70%. That’s more like it. That is a fine return for a REIT with Sila’s characteristics. Let’s look at one final scenario. Thus far we’ve been centering our valuation on comps. But are the peer level valuations reasonable? Well, they are actually at all-time lows. The peer group 10-year average P/FFO multiple, including the depressed levels of the last three years, is 15.7x vs. only 10.9x today. Why? Interest rates. Refer back to the slide earlier showing how correlated valuations are to interest rates. If interest rates and REIT multiples return to pre-Covid levels we get some really interesting numbers.

The economy appears to finally be slowing (for real this time). Lower rates are not needed for this pitch to work but would be very additive to returns.

Finally, let’s look at cap rates and asset value.

Pick your own cap rate and BV or NAV multiple but a 10.6% cap rate and the asset value here strikes us as attractive.

Industry backdrop

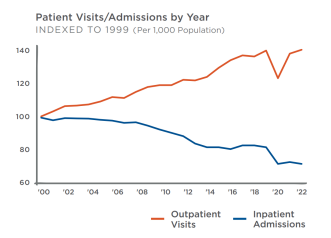

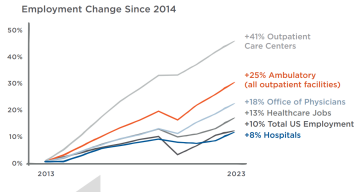

The population is aging, providing a natural demand tailwind for Sila’s properties. From 2022 to 2030 the 65+ age cohort is expected to grow 22% while the remaining population only grows 1.4%. This age cohort averages seven doctor visits per year vs. only three for those under 65. That’s a big change in demand. Further, outpatient visits are taking share from inpatient visits due to their lower costs. Outpatient centers are growing faster than just about any other part of the healthcare continuum.

Source: Healthcare Realty Trust 4Q23 earnings presentation

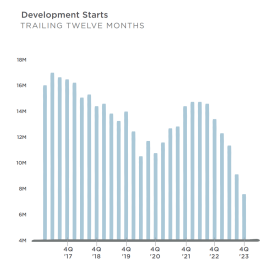

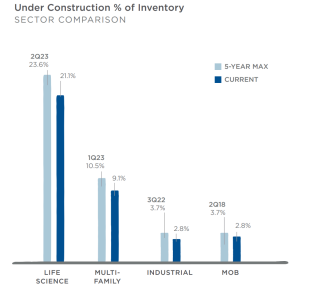

Source: Healthcare Realty Trust 4Q23 earnings presentation At the same time, MOB supply appears to be tightening.

Source: Healthcare Realty Trust 4Q23 earnings presentation

Source: Healthcare Realty Trust 4Q23 earnings presentation

Risks

Tenant credit

According to Sila’s 2023 10-K tenants had the following credit ratings:

There is obvious risk in “not rated” and “below investment grade” tenants. Sila obviously does extensive credit analysis on all tenants prior to signing. Sila’s largest tenant is Post Acute Medical with 15 leases at 14.5% of rents. Post Acute does not have a credit rating and financials are not available, however, according to management they have “very strong coverage ratios”.

GenesisCare, a tenant in 17 of Sila’s properties, filed for Chapter 11 bankruptcy on June 1, 2023. GenesisCare emerged from bankruptcy on February 16, 2024. Since filing for bankruptcy they have not missed a payment and the master lease related to their 17 properties was assumed by the emerging entity and remains in force under its existing terms which, we think, speaks to the high quality nature of Sila’s properties and leases.

Single Tenant risk

The obvious risk with having a single tenant lease is that it has an “all or nothing” aspect to it. If you lose the lease you probably lose all of it.

Conclusion

REITs have characteristics of both stocks and bonds. They sit below equities on the efficient frontier. They generally have betas below 1.0. Sila, however, has return characteristics of an attractively priced equity. Why? 1) The trading dynamics discussed earlier relating to it being a newly public company. 2) Defensive stocks are out of favor with utilities, REITs, and staples all underperforming recently. REITs have underperformed the S&P by 18% YTD and 20% over the past year, more than any other sector.

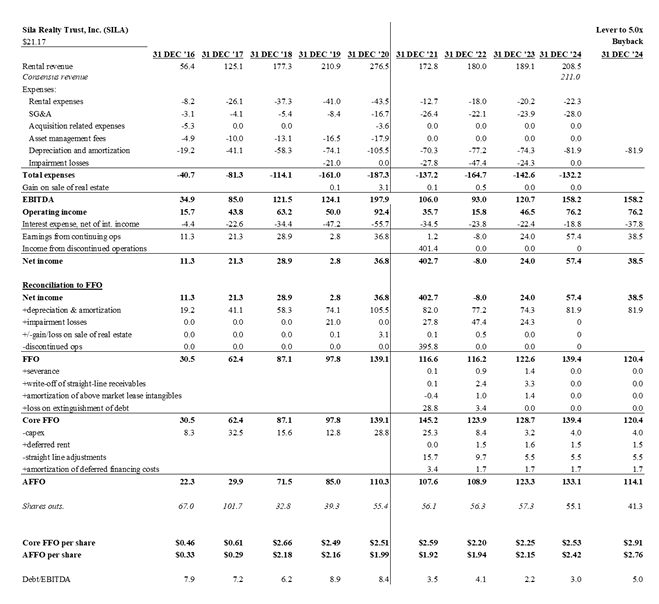

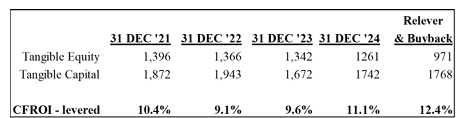

Historical Financials and 2024e

Returns

Other

Some qualitative aspects that are important but are currently a work-in-process…

DISCLAIMER: THIS IS NOT A RECOMMENDATION. The securities described are neither a recommendation nor a solicitation. There are no assurances that securities identified in this note will be profitable investments. The stated opinions are for general information only and not meant to be predictions or an offer of individual or personalized investment advice. This information and these opinions are subject to change without notice. Security information is being obtained from resources I believe to be accurate, but no warrant is made as to the accuracy or completeness of the information. Any type of investing involves risk and there are no guarantees. The author may or may not have material positions in the securities mentioned in this note and will not be obligated to give notice of any changes in their views or positioning. The author makes no representation or warranty, express or implied, regarding the accuracy, completeness, or adequacy of the information. The author accepts no duty of care to you in relation to investments. Past performance cannot be relied on as a guide to future performance.

Catalyst

Sellside coverage.

Relever balance sheet.

| 1 show sort by |