| 2022 | 2023 | ||||||

| Price: | 40.80 | EPS | 4.70 | 5.18 | |||

| Shares Out. (in M): | 59 | P/E | 8.7 | 7.9 | |||

| Market Cap (in $M): | 2,407 | P/FCF | 8.7 | 7.9 | |||

| Net Debt (in $M): | 606 | EBIT | 386 | 425 | |||

| TEV (in $M): | 3,013 | TEV/EBIT | 7.8 | 7.1 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- spinoff

- Dividend yield

- FCF yield

Description

SUMMARY

Kontoor Brands currently offers a great opportunity to invest in a business with two global brands—Wrangler and Lee—at a very reasonable price. The business had languished under former parent VFC Corporation which had treated its highly and consistently profitable jeans business as a cash cow and underinvested in it. This resulted in both revenues and operating profits of the jeans business languishing over the last twenty-five years. Since KTB’s spinoff three years ago, the brands have been reinvigorated by an incentivized management, with clear improvements in performance and potentially years of continued improvement ahead. Trading at about 8.6x projected 2022 EPS, and paying a dividend yielding 4.5%, the stock appears compellingly cheap, and is likely to give us an annualized total return of more than 20% over the next three to five years, with little risk of permanent capital loss.

INVESTMENT THESIS

I previously wrote up Kontoor Brands on VIC in June 2019, just after it had been spun off by VFC. The price then was $30.75. In April 2021 I recommended exiting the position, when the price had roughly doubled, earning us a total return of about 110% (including dividends) in less than two years.

Enough has changed since then to warrant a new report.

Now I’m heading back to the trough, looking for seconds. In the 12 months since my exit recommendation in April last year, KTB’s stock price has dropped by more than a third while the fundamentals of the business have improved dramatically from pre-pandemic levels. (From its peak of $69 one year ago, the stock is down more than 40%.) Therefore, I once again recommend the purchase of Kontoor. Three years ago, I wrote, “. . . I believe that Kontoor at its current price represents excellent value, with the prospect of large capital gains, possibly more than 100%, over two or three years. While we wait for the price to appreciate, we will collect a hefty dividend . . .” The same words can be used today (though the dividend yield is now “only” 4.5% vs. 7.3% in mid-2019. The dividend was eliminated briefly in the early days of the pandemic, though it was subsequently reinstated at a lower level. More on this later). Having the stock double from current levels over the next two or three years is not hard to imagine.

If you’re still reading, I urge you to read my June 2019 writeup for background, much of which I won’t repeat here. [George Bernard Shaw: “I often quote myself. It adds spice to my conversation.” I don’t know if I could say the same for myself.] Also, do read the message thread that followed, and in particular puppyeh’s view, which is cynical of my conclusions. (Incidentally, I’m a fan of puppyeh’s work, and paid careful attention to his comments.) And while you’re at it, also read VIC member bdad’s recommendation to short KTB in May 2021. His timing was impeccable, almost perfectly catching the stock’s peak price.

Despite the views of these VIC members, I believe that KTB represents a very interesting opportunity today. I have no difficulty imagining 20% compounded returns over the next few years. Also, given the durability of the company’s two brands, their growth opportunities, the huge cash-flow generation, the relatively modest debt load, and the improving balance sheet, I think that the long-term downside risk is very limited.

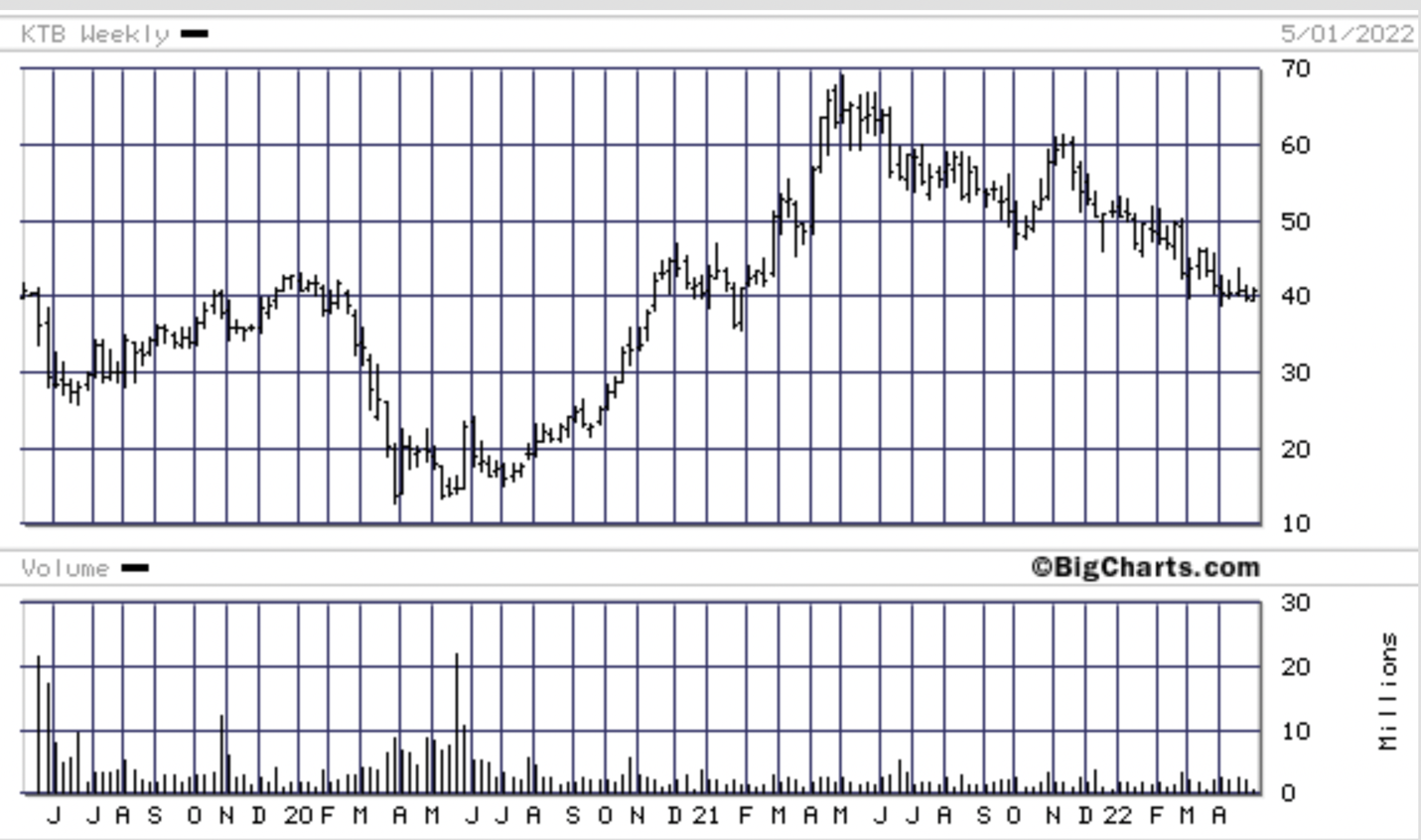

Below is a chart showing KTB’s stock price movement from the time of the spinoff in 2019 to the present. Following a big downdraft in the early days of the pandemic, the price reached a high of $69 in mid-2021. The decline over the last year is probably because of supply chain concerns and worries about the impact of politics on their growing China business. [They have little exposure to Russia and Ukraine.]

FINANCIAL PERFORMANCE

With the 4Q 2021 earnings report in early March, management provided its outlook for 2022. Their projections are surprisingly strong and suggest that, despite the pandemic, the business has gained traction since the spinoff, with revenues set to increase to above 2019 pre-pandemic levels, and operating profits to be the highest since 2016, with indications of further increases to come. EPS in 2022 is projected to be between $4.65 and $4.75. Given the improvement in the business over the last three years, despite the pandemic, the stock seems remarkably cheap, trading at less than 9x 2022 EPS and at something like 8.0x projected 2023 EPS.

The table below shows the performance of the business since the spinoff in 2019. Sales and profitability dropped sharply during 2020, due to the pandemic, but the company was still very profitable using GAAP accounting and even more so using “adjusted” earnings. 2021 saw a strong recovery in the business. Management’s projections for 2022 are for sales of about $2.7 billion, the highest level since 2016, with operating margins (EBIT) at over 14%, higher than any year since 2017. At an analyst meeting a year ago, management projected that operating margins would exceed 15% by 2023, and EPS would exceed $5.00. My projections below for 2023 and 2024 assume 5% revenue increases in each of those years, and 15% EBIT margins. This results in EPS of $5.18 in 2023 and $5.57 in 2024, numbers that are not hard to believe.

In the two tables below, we can see that, prior to the 2019 spinoff, VFC’s jeans business made operating margins of 16% - 19% in most years between 2010 and 2017. These numbers may have excluded some corporate overhead allocations of VFC, but suggest that further operating margin improvements, to perhaps 17%, are attainable. EBIT margins of 17% in 2024 (rather than the 15% I have above) would result in EPS of about $6.35 which could cause the stock price to exceed $100 two years from now.

Since the spinoff, Kontoor has shed the VF Outlet stores it inherited from its former parent. These generated over $200 MM of revenues and included sales of non-jeans products. Despite that revenue loss of $200 MM, total revenues are strong due to recent growth in sales of Wrangler and Lee products. Sales growth going forward is expected to come from several areas: (1) Digital DTC sales; (2) International expansion, where China is particularly important; and (3) Category extensions, particularly in the T-shirts, work clothing, and outdoor wear categories.

ECONOMICS OF BUSINESS

The table below suggests that the economics of KTB’s business are outstanding. The “Capital Employed” by the business at the end of each year ranged between 21.4% and 25.2% of annual sales (let’s assume 25%). This definition of “Capital Employed” includes working capital (excluding cash) plus other assets less other liabilities (excluding debt), plus PP&E. The capital employed at the end of 2021 was $529.8 million. (This number also approximates the tangible capital employed in the business.) GAAP operating income in 2021 was $283 million, indicating a return of 53.4% on capital employed.

This suggests that to generate an incremental $100 million in annual sales requires a one-time investment of about $25 million. If the incremental sales generate incremental operating margins of 15%, this implies that a one-time investment of $25 million can result in a permanent increase in EBIT of $15 million, or a 60% annual pre-tax return.

This also says that the investment required for growth is relatively modest, compared to the overall profitability of the business. 2022 sales are expected to be $2.7 billion and net income about $277 million. To grow sales by 10%, or $270 million, in 2023 will require incremental capital of about $67.5 million, leaving about $210 million for other purposes – debt reduction, dividends, and stock repurchases. That is real FCF of about 9% on the current market value of the stock, after required spending for revenue growth.

CAPITAL ALLOCATION

Since the spinoff, net debt has been reduced by $360 million, from $936 million to $576 million. Dividends of $213 million have been paid, and in 2021 $75 million was spent on stock repurchases. My expectation is that debt will continue to be reduced gradually from here, and that stock repurchases will at least offset dilution from compensation plans. I also think that dividends are likely to be increased significantly from the current level.

Prior to the spinoff Kontoor said that they would be paying an annual dividend of $2.24, or $0.56 each quarter. After three quarters of paying a dividend at that rate, the pandemic hit, and management eliminated the dividend in the second quarter of 2020. After two quarters of no dividend, it was reinstated at a lower rate of $0.40/quarter in 4Q 2020. One year later this was increased to $0.46 quarterly.

The company’s stated dividend policy is something of a puzzle. At the time of the spinoff, management said that the initial dividend would be $2.24 and the payout ratio would be 60%. Since then they’ve also said that they expect investors to get a dividend yield of 5%, which is puzzling because they seem to be predicting what the stock price will be, and implying that the stock price today should be something like $37 based on the current dividend. The 60% payout, which they haven’t repeated recently, suggests that the annual dividend today (or later this year) should be about $2.80, based on their recent projection of $4.70 of GAAP EPS for this year. My sense is that they will increase the dividend again in the fourth quarter, possibly to the pre-pandemic level of $2.24, which would be an increase of over 20% from the current level. I believe an annual dividend rate of $2.80 over the next couple of years is very plausible. That level would be only 25% higher than the initial dividend rate of $2.24.

VALUATION VS. LEVI STRAUSS

In my previous writeup in June 2019, I compared the valuation of KTB with that of LEVI. I said then, and I still believe, that Levi deserves a premium valuation to Kontoor. The valuation gap then was large, and although it has narrowed since then (KTB is up about 33% while LEVI is down 13%), I think Kontoor is still the cheaper stock today. This is based on current valuation metrics and also on my view that KTB’s margins will continue to improve over the next few years, resulting in higher earnings growth than LEVI is likely to get. In addition, KTB has a higher dividend yield, and I expect that its dividend will increase meaningfully in the next couple of years (see discussion on dividends above).

ENDGAME?

I think that management has stabilized the business since the spinoff, and the next few years should provide modest top-line growth (maybe mid-single digits), with higher operating income growth resulting from improving margins. EPS growth should be even higher, maybe 10%-15%, as debt is reduced further and the share count declines a little with buybacks.

I think of Wrangler and Lee as being closer to “basic” clothing (such as underwear) than fashion. If you like your Wranglers, you’re not likely to go looking for a different brand next year. This could make the company attractive to buyers at some point. I don’t know what strategic buyers would be interested—it’s unlikely to be Levi, in my opinion. What would a financial buyer pay for roughly $400 million of EBIT, which can be expected to grow? I’m not a PE guy and would welcome input here. Is $4 billion to $5 billion too high a price? That would imply a pre-tax yield of 8% - 10% for the buyer. To a shareholder, after deducting $600 million of debt, that suggests a potential buyout price of $57 to $75 today.

RISKS

-

Economic downturn.

-

Increased supply chain disruptions.

-

Interruption of China growth story.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

1. Higher sales and profits in coming quarters.

2. Increased dividend later this year.

| show sort by |