| 2024 | 2025 | ||||||

| Price: | 11.80 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 97 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 1,144 | P/FCF | 3.3 | 0 | |||

| Net Debt (in $M): | 125 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,265 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- SPAC!

- None found

Description

Executive Summary:

The SPAC, Flame Acquisition Corp (FLME) is in the process of merging with an E&P Energy company, Sable Offshore, in a ~$1bn combination. The investment thesis here centers on the strategic acquisition and reinvigoration of the Santa Ynez Unit (SYU) oil and gas assets, currently owned by Exon Mobile (EM) and located along the Gaviota Coast in Santa Barbara County, California. In addition to the SYU assets, FLME is also buying two pipelines, which EM acquired from Plains Exploration, facilitating access to key oil and gas infrastructure. Despite the negativity surrounding SPACs, this transaction has been met by strong investment demand evidenced by the SPAC common shares trading a $1 above the cash value of the SPAC Trust as well as by the massive $520mm of PIPE capital raised by prominent investors. The attraction to the thesis lies in the high quality of the asset, its access to infrastructure and attractive pricing, cheap valuation, strong balance sheet, and prominent management team. The key risks lie in getting regulatory approvals to be discussed below. The valuation is very attractive at a 30-50% discount to peers, while the downside pre-deal close) is limited by the value of the SPAC cash trust i.e. we see $3-$5 of upside vs $1 of downside by investing in the FLME shares. FLME also has warrants that could be used as another way to express a view on the stock (see Disclaimer at the end).

The Management:

The SPAC team is led by Jim Flores. Most E&P investors know him as he has a rather solid value creation track record. Jim Flores served as Vice Chairman of Freeport-McMoRan, Inc. and CEO of Freeport-McMoRan Oil & Gas, from June 2013 until April 2016. From 2001 until 2013, Mr. Flores was the Chairman, CEO and President of Plains Exploration & Production Company and Chairman and CEO of Plains Resources Inc. From 1994 until 2000, he was also the Chairman and CEO of Flores & Rucks, Inc. which, after several acquisitions, was later renamed Ocean Energy Inc. prior to its sale to Devon Energy Corporation. The following chart summarizes his achievements.

Jim Flores is putting up most of the capital to fund this transaction and he is also getting a decent equity stake in the surviving entity. After the merger, he will be staying on to run the operations of Sable Offshore together with his SPAC team composed of former senior management colleagues from Freeport McMoran Oil and Gas and Plains Exploration, who will also receive meaningful equity incentives.

The Transaction:

The transaction is structured as a two-step merger. Sable Offshore, a HoldCo controlled by Jim Flores, has entered into an agreement to acquire the SYU assets from EM. FLME, in turn, will merge with Sable Offshore, which will be the surviving entity and be renamed Sable Offshore. One of the most interesting parts of the transaction is that EM is not taking cash or shares in the deal for the sale of the asset. Instead, EM has agreed to finance the assets with a 1st Lien Loan in the amount of ~$625mm (net of a $19mm deposit). This loan matures in 2027, however it also has a “Springing Maturity”, 90-days after restart of the SYU assets’ operations. The EM 1st Lien Loan is PIK at 10% and started accruing at the signing of the deal in early 2022. There are some potential adjustments to the value of the loan (with a max of $75mm for certain Title / EPA Clean Up Adjustments) that can go in either direction. These adjustments are subject to confirming title (e.g. EM hadn’t paid certain easement access to the government so potential that could be a small issue), further the cost of some of the environmental regulatory approval may be added/subtracted from the amount depending on the final figures. Finally, it should be noted that EM also has a Reassignment Clause, i.e. if FLME is not able to restart the assets and bring them to operations by January 1, 2026, EM has the right to reassign the assets to another party with virtually no compensation to FLME, except for some relatively minor expenses. Here is a chart from the latest presentation on the size and structure of the deal. The chart is slightly outdated, showing $450mm in PIPE capital, vs the latest amount of $520mm. Further, the Loan doesn’t include the PIK accrued interest, which could be an additional ~$130mm by the time the deal closes.

Asset Overview:

Offshore Platforms: The SYU is an amalgamation of three offshore platforms, strategically positioned in federal waters offshore California. These platforms have a cumulative working interest across 16 federal leases, covering approximately 76,000 acres. The Hondo and Harmony platforms develop the Hondo Field, while the Heritage platform focuses on the Pescado and Sacate Fields. These platforms are located 5-9 miles offshore. They operate in shallow water depths of 900 to 1,200 feet, service a total of 112 wells, consisting of 90 producers, 12 injectors, and 10 idle wells. An additional 102 identified, undrilled opportunities present a promising avenue for future expansion.

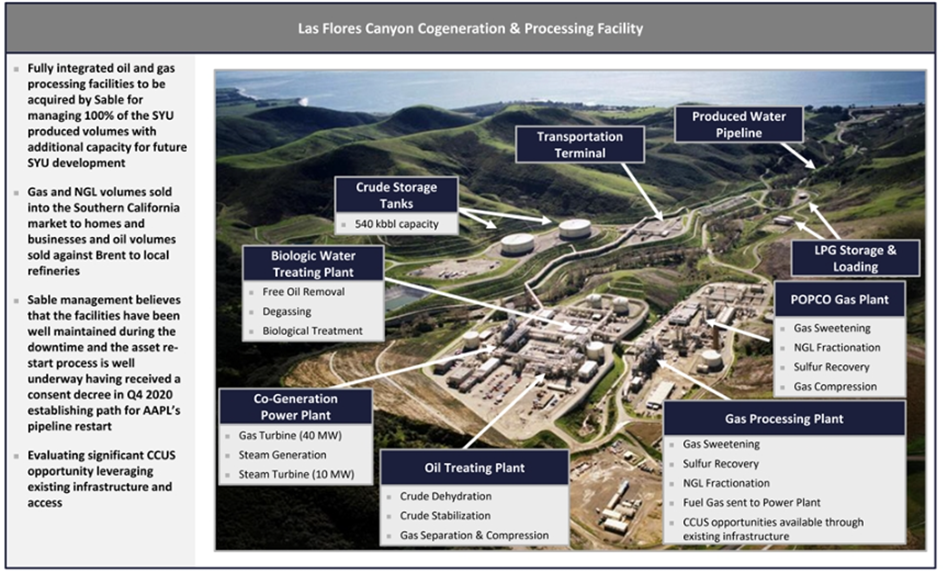

Onshore Processing Facility: Complementing the offshore platforms is a wholly owned onshore processing facility situated along the Gaviota Coast at Las Flores Canyon. Covering approximately 1,480 surface acres, the onshore facility is a fully integrated oil and gas processing center. It includes crucial components such as an oil treating plant, biologic/physical water treating plant, gas processing plants, a co-generation power plant, crude storage capacity of 540 MBbls, a produced water pipeline, liquified petroleum gas storage, and a transportation terminal. The facility infrastructure positions SYU well for efficient operations.

Pipeline Segments 901 and 903:

In addition to the offshore and onshore assets, the FLME purchase includes Pipeline Segments 901 and 903, formerly owned and operated by Plains and recently acquired by EM. These pipelines, integral to the oil transportation network, connect the SYU to local refinery markets. Despite a past incident (Line 901 incident), where a Plains Pipeline transporting produced oil from SYU experienced a leak, leading to a shutdown and subsequent safety measures, the potential restart outlined in the Consent Decree provides a strategic advantage in securing crucial connectivity for oil distribution.

Production History and Potential:

Between 1981 and 2014, SYU demonstrated its production prowess by generating over 671 MMBoe of oil and gas. In its prime, the platforms produced an average of 27 MMcf of natural gas and 29 MBbls of oil and condensate per day in 2014. However, in May 2015, the Line 901 incident prompted a suspension of production, leading to the shut-in of SYU assets and placement of facilities in a safe state. Despite the hiatus, the assets remain operation-ready, with ongoing inspections, maintenance, and surveillance.

In 2015, before the closing of the project, Plains conducted an analysis, which identified additional untapped opportunities, suggesting the potential for up to 102 identified, undrilled opportunities based on spacing assumptions. The strategic location of SYU off the California coast, combined with its historical production success, positions it favorably for capitalizing on the growing energy demands. Furthermore, the assets have proven to have a shall decline of 8% p.a. which reduces the reinvestment rate required to maintain projected production.

Contingent Resources and NSAI Evaluation:

To gauge the potential of the SYU assets, Sable engaged NSAI, an oil and gas reserves auditing and consulting firm. The independent evaluation focused on contingent resources and cash flow related to the potential acquisition of certain SYU oil and gas properties. As of December 31, 2021, NSAI estimated low estimate (1C) contingent resources, emphasizing the regulatory and operational contingencies influencing the classification. The estimated petroleum quantities are contingent upon approval from regulators, re-establishment of transportation systems, and the commitment to restart wells and facilities. While currently classified as contingent resources, there exists the potential for reclassification as reserves upon resolution of these contingencies.

Pipeline 901 Accident, Consent Decree and Restart Potential:

In May 2015, Plains All American Pipeline faced a significant environmental challenge when a crude oil release occurred from the Las Flores to Gaviota Pipeline (Line 901) in Santa Barbara County, California. This incident, known as the "Line 901 incident," resulted in a portion of the spilled crude oil reaching the Pacific Ocean at Refugio State Beach via a drainage culvert. Plains responded promptly by shutting down the pipeline and implementing its emergency response plan. A Unified Command, comprising entities like the U.S. Coast Guard, EPA, State of California Department of Fish and Wildlife, and others, was established to manage the response efforts. Cleanup and remediation operations were conducted, and the Unified Command eventually dissolved after determining the completion of these efforts.

A significant development in the SYU narrative is the Consent Decree entered into by Plains in 2020. This decree outlines a clear path for the potential restart of Lines 901 and 903, crucial components of the oil transportation infrastructure. The commitment to restart production is subject to regulatory approvals, re-establishment of oil transportation systems, and a steadfast commitment to revitalize the wells and facilities. The company has set the goal of re-starting the production in Q3’2024. The key impediment for the restart is safety approvals from the OSFM (Office of State Fire Marshal) for Line 901. The pipeline is about 10 miles long and the key solution involves the installation of insulation / safety valves. The cost of these valves hasn’t been disclosed but even if one assumes that one of these valves will have to be installed for each mile and the cost is ($1-2mm, this is my own guess and could be wrong), the costs will be quite manageable. EM and ultimately Sable Offshore will be indemnified by Plains for any legacy environmental issues pre 2022.

Valuation:

One of the main attractions of the story is the cheap valuation. It should be noted that Sable Offshore production will be ~80% oil based and it will have access to the higher Brent prices giving it better cashflow margins. The table below summarizes the cashflow at various commodity prices.

The fully diluted share count is as follows (depending on the outcome of the SPAC’s redemption).

Factoring the $388 of projected net debt at close, and the proceeds from the exercise of the warrants at $11.50, the pro forma net debt (for warrant exercise) is $95mm. Adding the accumulated PIK to the debt ($130mm) and using the No Redemption Scenario, we get to an EV of $1,260mm. In other words, at about $500mm EBITDA, the shares are trading at 2.6x EV/EBITDA. The Lev. FCF / MV is an impressive 35%. These valuations are at a 30-50% discount to peers. By purchasing FLME, the downside is protected in the event the deal doesn’t close.In that case investors will get redeemed at the trust value, which we calculate to be around $10.60-$10.65 by March ‘24, when the SPAC expires.

The management has presented the following table in their presentations. It doesn’t account for warrant dilution and PIK interest accumulation, but it is close to the numbers presented above.

Key Risks:

Regulatory Challenges: The success of the venture relies heavily on obtaining regulatory approvals for production restart. Proactive engagement with regulators, transparency in compliance measures, and strategic alignment with regulatory frameworks will mitigate this risk.

Operational Maintenance: Ongoing inspections, maintenance, and surveillance are paramount. Establishing robust operational protocols, preventive maintenance schedules, and technological solutions will ensure the assets remain in optimal condition and compliance with safety standards.

Catalyst: Closing of FLME / Sable Offshore Deal. Receiving Regulatory Approvals. Restarting Production. Capital Returns.

DISCLAIMER: This is not Financial Advice. Do NOT rely on this analysis for investment decisions. Please do your own work as I may have made errors and omissions in this write-up. I own securities in the company and may trade them at any time without additional notice.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Catalyst: Closing of FLME / Sable Offshore Deal. Receiving Regulatory Approvals. Restarting Production. Capital Returns.

| show sort by |