| 2023 | 2024 | ||||||

| Price: | 0.75 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 1,605 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 1,480 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 394 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,875 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

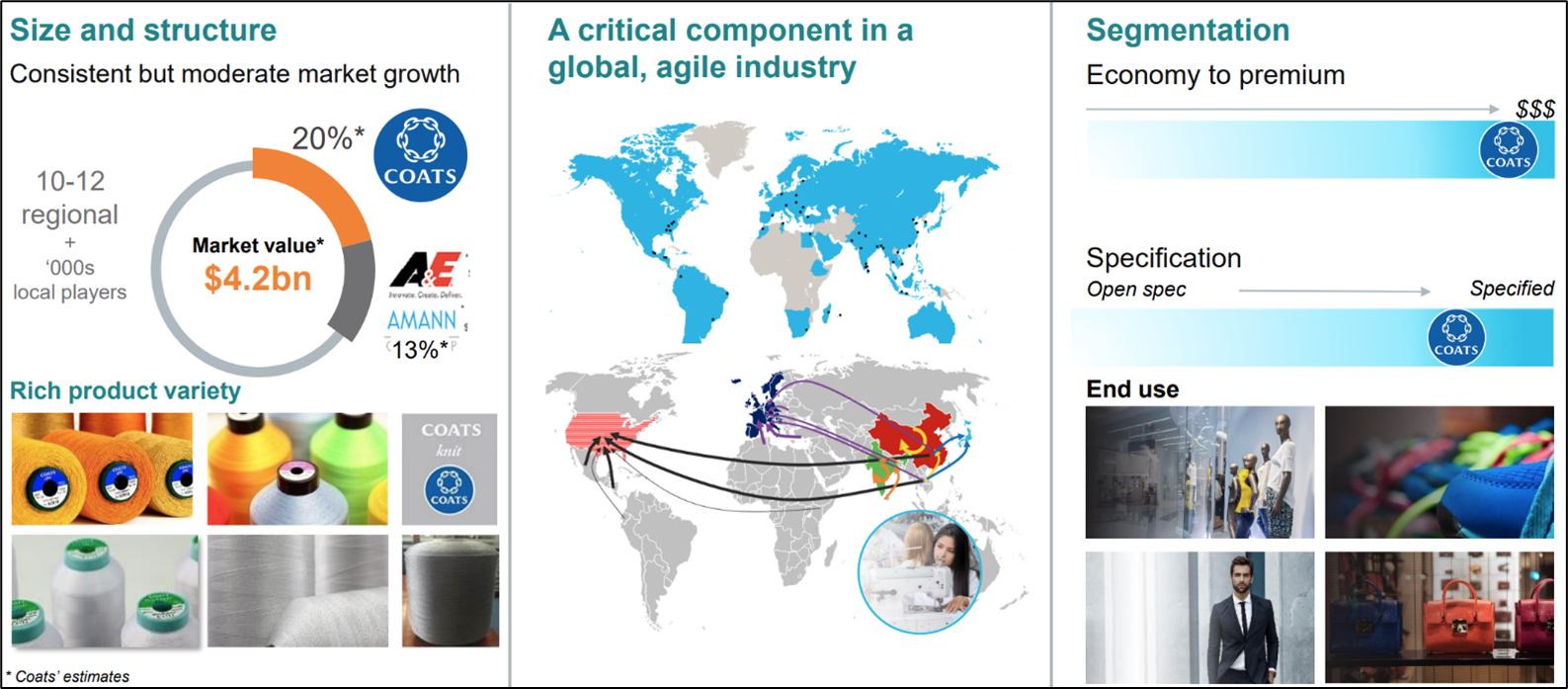

Coats is the world’s leading supplier of premium thread, serving brands in the footwear, apparel and performance materials markets. It earns attractive returns due to the high importance and relatively low cost of quality thread, along with its world class manufacturing base enabling customer flexibility at scale.

The opportunity is timely because 1) recent M&A has made its footwear components segment the industry leader, which should enhance growth and margins, and 2) pension deficit nearly eliminated, resulting in agreeement with Trustee to shut off ~$30m/yr cash contributions, which comprised ~50% of FY22 free cash flow. As these fundamental improvements gain visibility, they should be reflected in ~45% higher valuation (~£1.10/sh).

|

Consensus |

Our view |

What’s it worth |

|

|

|

Business model

The apparel segment (~50% PF revenue) sells premium thread to the apparel industry, and has scale to serve any brand or manufacturer, with market share >2x its next largest peer. Thread is typically 1-2% of the cost of a garment, but is critical to product performance and durability. Below is from a 2018 presentation–market share is now ~25% but general structure is similar:

Coats’ operational capability enables it to deliver thread anywhere in the world on short notice, with very specific colors and performance attributes, to large customers with specific needs.

The footwear segment (25% PF revenue) serves over 300 brands and 2,500+ manufacturers. Similar to apparel, its market share is at least 2x the next competitor, following the 2022 acquisitons of peer component suppliers Texon and Rhenoflex.

|

Products by company Customers by company

|

For reference, the picture below shows what the footwear components listed above do:

Footwear components are also a minor cost of the shoe, but are critical to initial feel, fit and silhouette, which are key drivers of consumer buying decision.

Performance materials are engineered threads for fire retardant protective wear, oil and gas infrastructure and other industrial products.

From 2018 presentation:

Value proposition

-

Thread is important to garment quality. If a customer buys a premium garment or shoe, and it begins to rip, it reflects terribly on the brand. To avoid this, premium brands often specify premium players like Coats, which rarely comprise more than 1% of input cost.

-

Another area of importance is manufacturing throughput. Thread failure in manufacturing is an expense that manufacturers and brands loathe. If thread breaks during manufacturing, which happens with lower quality brands due to needle heat, it slows down the entire process and impairs factory efficiency.

-

Scale is becoming increasingly important as brands consolidate suppliers, globalize their businesses, and improve manufacturing flexibility. Coats’ global, digital production base makes it one of the few thread makers able to accommodate customers of any size.

Source of mispricing

-

Business quality may be underappreciated. When most people hear thread, the gut reaction is a commodity product with heavy price pressure. Researching Coats highlighted the importance of thread to garment quality, and the poor risk/reward of using a cheaper brand

-

The pension opportunity, while disclosed during Q4 earnings, is not yet reflected in financial statements, but the potential for ~$30m annual FCF to fall to the bottom line is meaningful to a company with $65m FY22 FCF.

-

There may also be some UK discount, as Coats is a heritage British brand and trades in London, but transacts in dollars and operates globally. Currently <2% of revenue is from UK, and 20% Europe total.

Pension

At 3/31/21, the triennial valuation estimated a £193m funding deficit. As a result, payments were scheduled at $27m/yr (£22m) through 2028. Since then, the gap has been erased due to 1) payments from Coats, 2) higher discount rates, and 3) de-risking actions such as buying an annuity to fully cover 20% of beneficiaries. As a result, the Trustee has agreed to switch off payments if the deficit remains in 1% surplus for two consecutive months, only requiring future payments if the pension goes back into deficit. This is realistic in 2023, and management will make an announcement if it happens.

The FY22 annual report states that Coats is expected to contribute $31.6m in FY23 (ex-admin fees). However, this amount “will be lower in the event that regular cash contributions to the Coats UK pension scheme are switched off under the mechanism set out above.”

Peers

Apparel competes most directly with American & Efird (owned by Platinum Equity since 2018) and Amann. Platinum bought A&E from KPS in 2018 for a rumored $540m, according to WSJ. For reference, A&E is estimated <50% of Coats’ apparel revenue.

Most other peers are not publicly traded, and those that are mostly trade in Asia. Looking at apparel manufacturing subcontractors, Eagle Nice (2368.HK) trades at mid/high-single digit EV/EBIT. This business is lower quality (based on ROIC), with lower margins than Coats. There are not many relevant comps for this niche business.

Risks

Industry destocking. Despite Coats leading position in its main verticals and entrenched position in many customer products, if an economic slowdown reduces production of apparel or footwear, revenue will be impacted.

Merger integration. Integrating 3 footwear components suppliers into a coherent business involves standard merger risks. Specific to footwear, if customers became concerned that combined Coats footwear has too much market share (especially those who had been customers of all 3), growth could fall short of expectations.

Interest rates decline. Although 90% hedged against interest rates and inflation, lower rates could increase pension liabilities and modestly negate that part of the thesis.

Limited addressable markets. The company estimates addressable markets of $3.4B in apparel, $1.8B footwear and $3.0B performance materials. This could cap long-term growth for Coats, but on the positive side, likely deters new entrants and maintains attractive margin pools. Near term, market size should not limit growth, but it may limit the potential multiple upside.

Valuation

Aside from pension relief, the opportunity is accelerated footwear growth and improved margins:

Significant margin gain potential due to improved mix, efficiency programs and manufacturing footprint optimization. Chart below shows historical margins versus implied margins in DCF value £1.15/sh. At 17% EBIT, Coats current implied multiple is <7x EV/EBIT. This is a far higher quality business than a single digit multiple suggests.

The below chart estimates value at various EV/EBIT multiples. The risk/reward given the improved balance sheet and footwear opportunity seems decent.

The business has historically traded at 10x EV/EBIT, now with improved segment mix (ex-2019 Crafts sale) with higher margins and a removed pension overhang. Footwear components, complementing the thread business should warrant a higher multiple than Crafts, which mostly sold yarn to hobby stores. Footwear is expected to be Coats’ fastest growing division, whereas Crafts was stagnant. Business mix from 2018 presentation:

On a DCF assuming 5.5% 5yr revenue CAGR, 150bps margin improvement and a 9% WACC, implied share price is ~£1.14 (>50% upside). All of these assumptions are below management guidance, so if they approach mid-term goals, Coats' upside would be greater.

As another valuation data point, when recently-acquired Texon sold to private equity in 2016 for ~£100m, revenue was ~£19.4m and pretax profits £2.9m. (https://www.gazettelive.co.uk/business/business-news/teesside-footwear-factory-sold-part-11153502)

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Catalyst

-

Pension unlock. As mentioned, it is likely that ~$30m annual cash pension payments will be suspended in 2023 as the UK scheme reaches surplus. Enhanced FCF frees capital for investment and potentially returns to shareholders. In 2-3yrs, the entire pension could be removed from the balance sheet if it can be affordably transferred to a third party.

-

Further portfolio enhancement. The business has a more attractive mix today than at the 2016 writeup by exiting Crafts. There is opportunity to further focus by exiting zippers (9% of FY21 A&F revenue), which sounds like a near-term possibility:

“We keep on looking at the performance of the portfolio. We exited Brazil and Argentina. We closed the Russian operations…We continue to look at zips. Zips is one area where we have a strategic review going on, and if there's anything to announce at some point in the future, we will be happy to announce that.” CEO Rajiv Sharma; Oct22 investor day

-

Revised segment reporting. Coats historically segmented “Apparel & Footwear” and “Performance Materials.” Beginning FY23, Apparel and Footwear will report separately, highlighting the Footwear segment. If the business achieves plan, investors could be attracted to Footwear's accelerating growth.

-

Footwear uppers. Footwear segment currently sells ~$400m of components in a $1.8B market. However, it has limited presence in the upper part of shoes and believes it can supply this area also. If achieved, it would more than double footwear TAM.

“The advantage of having an upper is you can integrate the structural components into it directly. So from a manufacturer standpoint, rather than putting 5, 6 pieces in at one time, they just have to put one piece in. It’s a big market. We are in discussions with several big brands and I would expect in the next 24mos, there would be a lot more brands coming out with the uppers.” -CEO Rajiv Sharma

I do not ascribe much value to this, as there are likely limits to how much brands will outsource to a single supplier (research conversation suggested ~30%) but the potential market is very large and the probability is greater than zero.

| show sort by |