| 2018 | 2019 | ||||||

| Price: | 9.70 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 151 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 1,470 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 60 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,530 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- China Yangtze Power 600900 12/18/2018

Description

Central Puerto (NYSE: CEPU)

Link to PDF: https://www.dropbox.com/work/CEPU%20VIC?preview=CEPU+VIC.pdf

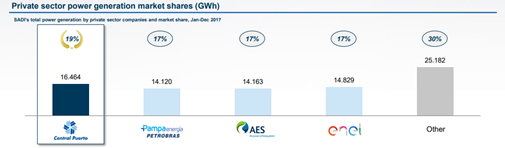

- CEPU is the largest private sector power generator in Argentina, with a diversified portfolio of high quality assets (thermal, hydro and wind) and a meaningful backlog of projects under construction. In 2017, CEPU had a 10% market share as measured by systemwide capacity and a 19% market share among private sector power generators as measured by total power generated.

- In February 2018, CEPU IPOed on the NYSE at $17.70/sh., but has traded down since then, largely because of the economic turmoil in Argentina. However, we believe CEPU will in fact be a net beneficiary of this turmoil vis-à-vis depreciation of the Argentine Peso (98% of revenues are in USD, while only 30% of OPEX and 80% of CAPEX are denominated in USD). Unless you believe that Argentina will revert to the Kirchner era or go down the path of asset nationalization, which we don’t believe will be the case, CEPU’s cash flows (in USD), should not only be safe, but grow at a rate substantially above that of other LatAm utilities over the next 4 years. While an economic recovery in Argentina is not a precondition for investors to make money investing in CEPU at current levels, we believe that CEPU has meaningful upside should a recovery in Argentina occur. Consequently, we view the risk/reward of an investment in CEPU as very favorable. We believe that CEPU at least deserves a multiple in-line with other LatAm GenCo’s given its EBITDA growth profile and USD denominated revenues. As investor sentiment improves, we believe CEPU, valued at 6x 2021 Adj. EBITDA, is worth $19.14/sh. and has a ~97% upside over the next two years to the current trading price of $9.70. This represents a 12% levered FCF yield at our target valuation vs. a 23% levered FCF yield at today’s price.

Key Points:

- CEPU will increase its production capacity by 22% between now and mid-2020 only through the contracted projects that CEPU is currently in the process of building. However, CEPU’s Adj. EBITDA, denominated in USD, should grow by 102% by mid-2020. Additional project wins would provide further upside. Argentina’s energy generating assets can be bifurcated into two remuneration regimes: Base Energy and New Energy. Remuneration for CEPU’s New Energy thermal assets (monomic price: $32/MWh) is significantly higher than for its Base Energy assets (monomic price: $17.5/MWh). Consequently, CEPU’s expansion projects generate a higher EBITDA/MW of capacity than its existing Base Energy assets.

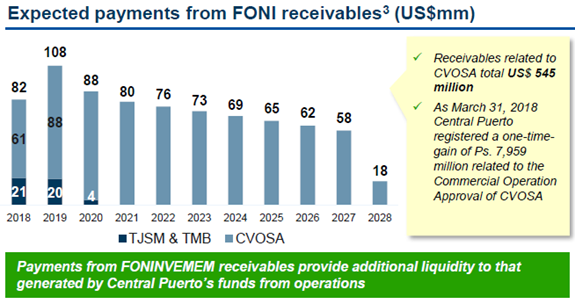

- CEPU has equity ownership in 3 power plants as part of the FONINVEMEM program, a program in which power generation companies, like CEPU, contributed receivables for electric power sales between 2004 and 2011 as a means of funding new power plants. CEPU collects a receivable cash flow stream for 10 years post-COD (Commercial Operation Date) of the project and retains equity ownership in the asset thereafter. CEPU’s EBITDA doesn’t reflect these receivable cash flows (averaging ~$72 M/yr. for the next 10 years).

- CEPU has an under-levered balance sheet, with a net debt position of $60M as of Q2 2018. We believe that CEPU could comfortably take on 2-3X leverage, which in our view gives CEPU an extra $700-1,000M of balance sheet capacity to bid for new projects in upcoming government auctions or bid for the government’s equity stake in existing power generating assets.

- Argentina currently lacks sufficient power generation capacity, which will only be exacerbated as power demand grows (typically GDP+). Argentina plans to auction off an additional 10 GW of generation capacity by 2025 (vs. 36.5 GW installed capacity EOP 2017). Given CEPU’s strong track record, we expect CEPU to at least maintain market share as system capacity grows. While the bidding processes are almost completely based on price, in certain cases, the ability to expedite completion represents a firm advantage. CEPU has already purchased land and 969 MW of gas turbines, which could help accelerate the completion cycle of a new thermal projects by up to 1 year. We believe that any deterioration to Argentina’s economic or political landscape will have little impact on CEPU’s LT cash flows. We believe that the risks of further liberalizing Argentina’s energy generation policy are skewed to the upside.

1) New Energy assets have legally binding PPA’s (15-20 yr. length) and remuneration cannot be legally changed by the government.

2) Any changes impacting remuneration for power generation assets impacts the government’s ability to incentivize future generation capacity, which we believe carries strong political importance.

3) We can envision a scenario, perhaps over the next 5 years, in which the government changes Base Energy remuneration policy to remove inefficient assets from the system (i.e. those that use high cost fuel sources or inefficiently use low cost fuel sources). However, for that to happen the government will need to 1) auction off additional capacity at New Energy rates (CEPU should win its proportionate share additional capacity that carries a higher EBITDA/MW than inefficient capacity at Base Energy rates) and 2) improve Argentina’s natural gas shortage in the winter months, which causes efficient generation assets to switch to significantly higher cost fuel sources.

4) If the government allows a TERM market, in which private energy users can contract directly with generators, for thermal assets, like they do for renewable assets, we believe that CEPU could potentially realize pricing for its Base Energy assets closer that which is received for its New Energy assets.

5) CEPU expects to benefit from an additional operating margin if fuel purchasing responsibility is shifted back to generators, as opposed to the current regime in which CAMMESA, Argentina’s wholesale energy market administrator, is responsible

*Currency is in USD unless otherwise noted.

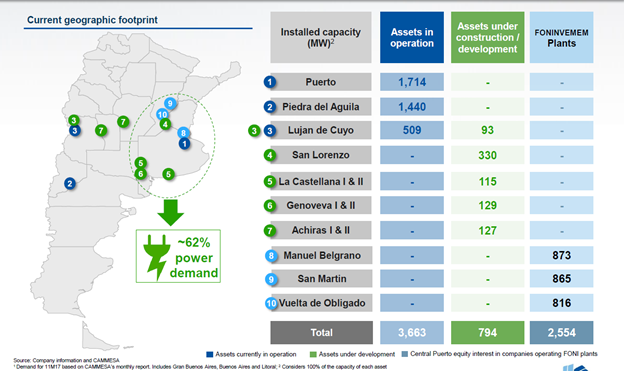

1) Assets

CEPU has a total installed power generation capacity of 3,663 MW (100% owned), representing 10% of the country’s capacity, which was 36.5 GW as of 2017. Measured another way, CEPU had a 19% market share among private sector power generators as measured by total power generated (Figure 1). CEPU owns a balanced portfolio of generation units, including thermal (2,223 MW) and hydro sources (1,440 MW), located close to high demand centers.

Figure 1: CEPU is the largest private energy generator in Argentina as measured by power generation in 2017

Figure 2: CEPU has a diverse installed base of power generating assets in high demand centers

Existing Thermal Assets

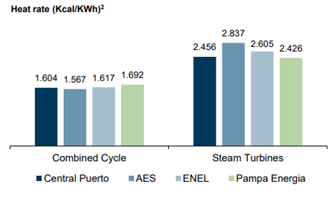

The company consistently prints high availability rates supported by a rigorous maintenance program. The average availability of CEPU’s thermal assets (91% in 2017), is 12% higher than market average (79% in 2017). CEPU’s units are favorably positioned along the system’s power dispatch curve and rarely turned down by the dispatch administrator. Importantly, 92% of thermal capacity is flexible (can run using natural gas or fuel oil/gas oil), insulating CEPU from natural gas shortages in winter months. CEPU’s efficiency levels compare favorably to those of its competitors due to efficient technologies (Figure 3). CEPU’s existing thermal assets are remunerated under the Base Energy regime (Capacity payment of US$ 7,000 per MW per month; and Energy payments US$ 7 per MWh for generation with natural gas and US$ 10 per MWh for generation with fuel oil/gas oil). The thermal plants operate under an indefinite concession and fuel is provided from CAMMESA. CEPU’s assets have a low level of maintenance capex, expected to run $7M/yr., because long-term maintenance contracts with turbine manufacturers flow through OPEX.

Figure 3: Efficiency level measured by heat rate, which is the amount of energy used by an electric power plant to generate one kWh of electric power, for the period between February 2018 and April 2018. CEPU’s efficiency levels measure favorably compared to its main competitors

- Puerto Complex (1,714 MW Capacity)

- Composed of two facilities, Nuevo Puerto and Puerto Nuevo, located in the port of the City of Buenos Aires.

- Puerto consists of a combined cycle plant (765 MW capacity) that uses natural gas or gas oil; and 5 steam turbines (949 MW capacity) that run on natural gas or fuel oil

- Puerto Complex’s availability was 91% in 2017, 75% in 2016 and 75% in 2015

- The Puerto combined cycle plant is one of the most modern and efficient plants in Argentina

- Scheduled maintenance of the Puerto Combined Cycle Plant resulted in a 27% yr./yr. reduction in thermal generation in H1 2018

- Composed of two facilities, Nuevo Puerto and Puerto Nuevo, located in the port of the City of Buenos Aires.

- Luján de Cuyo (509 MW Capacity)

- Facility located in Luján de Cuyo, Mendoza

- Luján de Cuyo consists of a combined cycle plant (343 MW capacity) that uses natural gas or gas oil; 2 steam turbines (120 MW capacity) that run on natural gas or fuel oil; and 2 co-generation turbines (46 MW capacity) that run on natural gas or gas oil

- Luján de Cuyo’s availability was 93% in 2017, 81% in 2016 and 89% in 2015

- Steam is delivered to YPF pursuant to a separate contract

Existing Hydro Asset

- Piedra del Águila (1,440 MW Capacity)

- Piedra del Águila is the largest private sector hydroelectric generation complex in Argentina.

- Facility is located approximately 1,200 kilometers to the southwest of Buenos Aires at the edge of Limay River and on the border of the Neuquén and Río Negro provinces.

- Concession lasts until December 29, 2023. CEPU intends to renew the concession agreement prior to expiration

- Base Energy remuneration: Capacity payment of US$ 3,000 per MW per month; and Energy payments US$ 4.9 per MWh for generation

- Piedra del Águila’s availability has been 100% in 2017, 2016, and 2015

- Piedra del Águila can store energy for 45 days operating at full capacity

- The recent drought in the Pampas region of Argentina did not affect the power production of CEPU’s hydro asset due to different geographies. However, in 2016 Piedra del Águila had its worst generation year due to a drought in that region.

- Piedra del Águila is the largest private sector hydroelectric generation complex in Argentina.

Thermal Assets Under Development

CEPU is currently constructing 423 MW of cogeneration thermal plants (100 % owned; 15-year PPA with CAMMESA). Importantly, the energy prices received are under the New Energy pricing regime, which is significantly higher than the Base Energy pricing. The thermal plants will be completely financed with internally generated cash flows/cash on hand.

- Expansion of Luján de Cuyo (93 MW Capacity)

- Expected COD: November 2019

- Awarded energy price [capacity + variable]: 17,100 US$/MW per month + 8 US$/MWh

- CAPEX: US$91mm (US$45mm already disbursed)

- Steam offtake with YPF. New steam contract to replace the current one at Luján de Cuyo

- Expected COD: November 2019

- Terminal 6 San Lorenzo (330 MW)

- Expected COD: May 2020

- Awarded energy price [capacity + variable]: 17,000 US$/MW per month + 8 US$/MWh for generation with natural gas and US$ 10 per MWh for generation with gas oil

- CAPEX: US$284mm (US$42mm already disbursed). Uses one of the 4 turbines already purchased by CEPU

- Steam offtake with T6 Industrial S.A

- Expected COD: May 2020

Wind Assets Under Development

CEPU is currently constructing 371 MW of wind farms, 234MW of which through the RenovAR program (20-year PPA with CAMMESA) and 137 MW of which thought the MATER term market (likely 20 yr. PPA with large industrial users). The renewable projects are held within the entity CP Renovables, which is 70.19% owned by CEPU and 29.81% owned by Guillermo Pablo Reca, CEPU’s largest shareholder. The new wind plants will be 70% financed with non-recourse project debt and 30% financed with cash on hand. The Castellana and Arichas project debt was taken out with International Finance Corporation (“IFC”) and Inter-American Investment Corporation (“IIC”) (rate of Libor +5%; amortizable over 13 years).

RenovAr Program

- La Castellana (99 MW)

- Expected COD: July 2018

- Awarded energy price: 61.50 US$/MWh with a 1.7% PPA inflator

- Expected COD: July 2018

- Achiras (48MW)

- Expected COD: June 2018

- Awarded energy price: 59.38 US$/MWh with a 1.7% PPA inflator

- Expected COD: June 2018

- La Genoveva I (86.6 MW)

- Expected COD: May 2020

- Awarded energy price: 40.90 US$/MWh with a 1.7% PPA inflator

- Tax certificate equal to 20% of the value of electromechanical components made in Argentina

- Expected COD: May 2020

Term Market (MATER

- La Castellana II (15.75MW)

- Expected COD: July 2019

- Awarded energy price: likely ~60 US$/MWh with a 1.7% PPA inflator

- Expected COD: July 2019

- Achiras II (79.8 MW)

- Expected COD: January 2020

- Awarded energy price: likely ~60 US$/MWh with a 1.7% PPA inflator

- Expected COD: January 2020

- La Genoveva I (41.8 MW)

- Expected COD: November 2019

- Awarded energy price: likely ~60 US$/MWh with a 1.7% PPA inflator

- Expected COD: November 2019

FONI Asset Ownership

CEPU holds equity stakes in three thermal generation plants (combined capacity 2,554 MW). CEPU participated in an arrangement known as the FONINVEMEM. These plants are owned by the FONI trust and operated by private generators. The prior Argentine government’s administration created the FONINVEMEM with the purpose of repaying power generation companies, like CEPU, the existing receivables for electric power sales between 2004 and 2011 and funding new power capacity. For the 1st 10 years after COD, these assets have a PPA with CAMMESA and equity holders collect a receivable stream equal to the principal plus interest for the initial receivables contributed. After 10 years, the remuneration rate will convert to the Base Energy rate and private shareholders will receive the asset’s property rights with the condition that the Argentine government be incorporated as a shareholder, effectively diluting private generators’ equity stakes. These FONI holdings do not have any debt on them and the government will be looking to sell its pro-rata equity interest in FONI holdings.

- San Martín (TSMJ): (865 MW)

- Combined Cycle plant completed in 2010.

- CEPU is the 1st minority in TSMJ.

- FONINVEMEM Receivables: CEPU collects US$ receivables in 120 monthly payments plus 360-day LIBOR+1%

- Equity Stake: CEPU has a 30.88% equity stake in TSMJ which will be diluted to 15.5% 10 years after COD (i.e. in 2020). The government will be incorporated as a 50% equity holder.

- Combined Cycle plant completed in 2010.

- Manuel Belgrano (TMB):

- 865 MW Combined Cycle plant completed in 2010.

- CEPU is the 1st minority in TMB.

- FONINVEMEM Receivables: CEPU collects US$ receivables in 120 monthly payments plus 360-day LIBOR+1%

- Equity Stake: CEPU has a 30.95% equity stake in TMB which will be diluted to 15.5% 10 years after COD (i.e. in 2020). The government will be incorporated as a 50% equity holder.

- 865 MW Combined Cycle plant completed in 2010.

- Vuelta de Obligado (CVOSA):

- 865 MW Combined Cycle plant completed in March 2018.

- CEPU is the controlling company for CVOSA

- FONINVEMEM Receivables: CEPU collects US$ receivables in 120 monthly payments plus 30-day LIBOR+5%

- Equity Stake: CEPU has a 56.19% equity stake in CVOSA which will be diluted to 17% 10 years after COD (i.e. in 2028). The government will be incorporated as a 70% equity holder.

- 865 MW Combined Cycle plant completed in March 2018.

Figure 4: CEPU’s cash flow stream from FONI receivables.

Other Assets/Liabilities

- Receivables/Loan with CAMMESA: As of 2Q18, CEPU has ~$94mn of loans with CAMMESA (including principal and interests), resulting from old loan transactions with the Argentine trading chamber. CEPU also has receivables (only principal) recognized at book value, as the company is not allowed to recognize the interest portion of its credits before effective settlement of this receivable. CEPU’s net receivable position is positive, at ~$50mn. CEPU’s receivable with CAMMESA can be used to pay down the loan with CAMMESA (i.e. non-cash transaction) and can be used as currency to pay for the government’s equity stakes in power generation assets, should it win the auction.

- Turbines acquired for future projects: In 2015/2016, CEPU acquired four gas turbines (totaling 1,255 GW), one of which will be used for the already contracted project San Lorenzo (286 MW). Additionally, the company has also acquired 130 hectares of land in the province of Buenos Aires. We believe that the remaining 3 turbines/land will be looked upon favorably in future auctions as CEPU will be able to reduce development time from 24-36 months to 18-24 months. CEPU has spent US$ 134mn on these assets.

Non-Core Assets

- Ecogas is the third largest natural gas distributor in Argentina, with almost 11.75% volume share in the country with a network of ~31k km covering ~1.3mm clients. Distribuidora de Gas Cuyana (DGCU) and Distribuidora de Gas del Centro (DGCE); both operate under the Ecogas brand. CEPU would eventually like to merge DGCU and DGCE and list the combined entity on a foreign exchange. While we believe that Argentinean equity markets would need to improve before this happens, we note that CEPU is amenable to monetizing its equity stake.

- DGCU: CEPU owns a 22.49% equity stake in DGCU. DGCU is publicly traded in Argentina (Ticker: BGCU.BA). DGCU has a market cap of $300M. CEPU’s ownership is $67M. CEPU collected $6M in dividends from DGCU in 2018.

- DGCE: CEPU owns a 33.69% equity stake in DGCE. Given both DGCE and DGCU have very similar size and operations, we assume both companies have a similar equity value. We approximate CEPU’s ownership at $119M. CEPU collected $13.6M in dividends from DGCE in 2018.

- DGCU: CEPU owns a 22.49% equity stake in DGCU. DGCU is publicly traded in Argentina (Ticker: BGCU.BA). DGCU has a market cap of $300M. CEPU’s ownership is $67M. CEPU collected $6M in dividends from DGCU in 2018.

- Transportadora de Gas del Mercosur (TGM): CEPU has a 20% equity stake in a company that manages a 450km natural gas pipeline extending from Argentina to Brazil with transportation capacity of up to 15mm m3/day. In Q1, CEPU received a $11.4M dividend derived from TGM’s settlement with YPF. Since Argentina no longer export gas to Brazil we value TGM’s value going forward as $0 M

2) Valuation

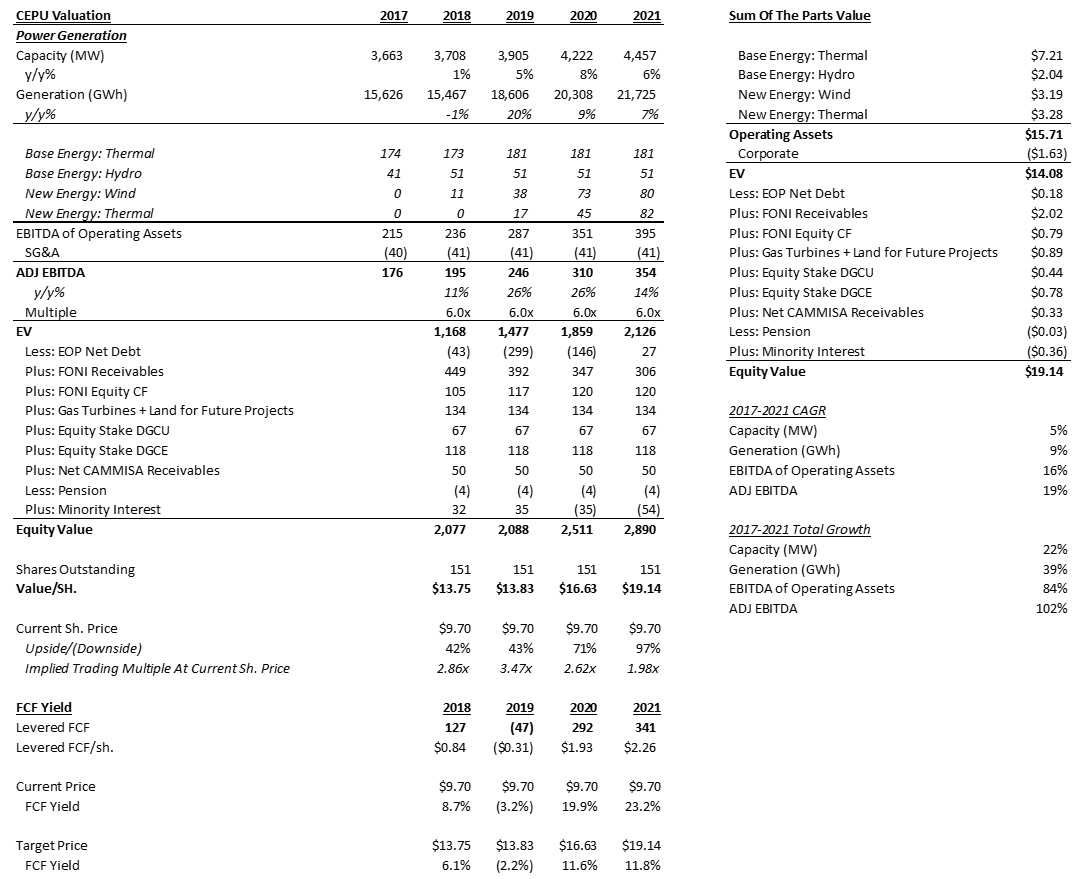

We believe that CEPU, trading at $9.70/sh., remains significantly undervalued. CEPU has a predictable revenue stream denominated in USD. It’s cost structure OPEX (30% USD) and Capex (80-90% USD) benefits from the FX depreciation occurring in Argentina. We believe that CEPU’s existing assets (at the current Base Energy rate, which is higher than it was in 2017) generates $192M of Adj. EBITDA. This number is inclusive of $40M of corporate SG&A, which we expect to be flat going forward (minimal SG&A required for future projects will be largely offset by ARS depreciation). Given messiness of CEPU’s financials we define EBITDA as gross margin less SG&A plus D&A. The new projects CEPU has coming online between now and Q2 2020, should add $162M of incremental EBITDA. We believe that by H2 2020 CEPU should be generating $354 M run rate of EBITDA. We capitalize this EBITDA stream at 6x, in line with other LatAM GenCo’s, then make the following balance sheet adjustments to arrive at our equity value:

- EOP Net Debt: Forecasted EOP net debt

- FONI receivables: NPV of FONI receivables discounted at 12%. CEPU will collect a receivable stream from its ownership in FONINVEM projects, averaging $72M for the next 10 years with higher cash flow in the front years

- FONI equity CF: NPV of CF in FONI equity holdings (post-PPA expiration and post-government inclusion as an equity holder) discounted at 12%

- Gas Turbines and Land: We value the $134M CEPU has spent on 3 gas turbines and land at cost.

- Equity Stake in DGCU: Valued at the current market value of DGCU multiplied by CEPU’s ownership.

- Equity Stake in: DGCE: Assumes DGCE has the same equity value as DGCU, since their assets are similar, .

- Net CAMMESA Receivable: CEPU has a $50M net receivable with CAMMESA (receivables from CAMMESA less Loans with CAMMESA)

- Pension: Book value of pension liability

- Minority Interest: 30% of 6x Wind Segment EBITDA less 30% of non-recourse wind project debt.

Figure 5: CEPU Valuation Overview

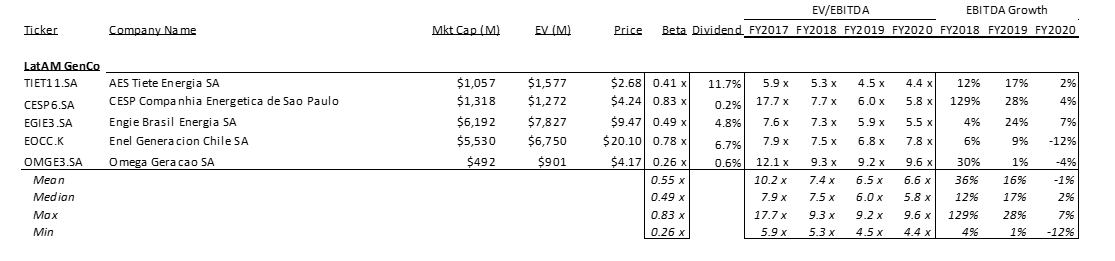

With exception of Brazilian GenCo’s, LatAm (Mexico, Colombia, Chile, Peru and Argentina) power prices are set in USD. We believe that a fair EV/EBITDA multiple for CEPU is at least 6x, in-line with other LatAm GenCo’s, which is below the 7-9x that US merchant generators trade, and significantly below the 10-12x that regulated utilities trade. We also note that that LatAm GenCo’s are trading at the bottom of the 6-8x range they have traded in over the past few years. By our calculations, CEPU trades at a material discount to other LatAm GenCo’s despite having USD denominated revenues and a better EBITDA growth profile. After making the appropriate balance sheet adjustments, CEPU trades at 2x our 2021 EBITDA vs. our target of 6x. Our target value of $19.14 implies a 12% levered FCF yield vs. 23% at the current price.

Figure 6: Comparable Multiples of LatAm GenCo’s

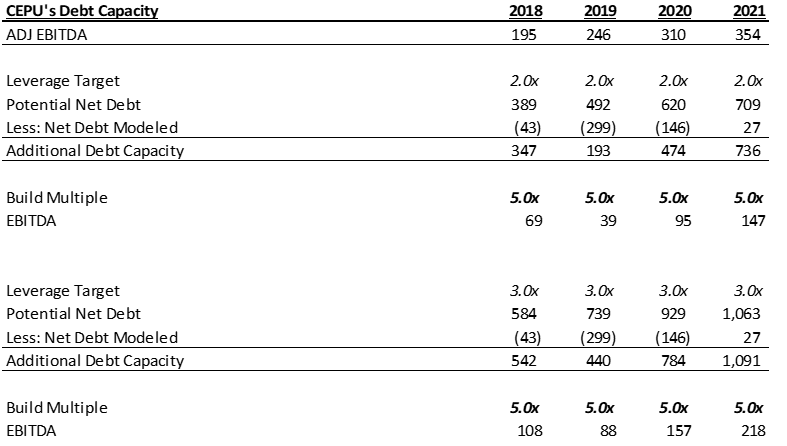

CEPU’s underleveraged balance sheet and strong track record put CEPU in a strong position to bid for projects in new capacity auctions as well as bid for government’s equity stakes in its power plants. Assuming 2-3x leverage, we believe the company has $700-1,000M of debt capacity, which could add $147-218 M in EBITDA (Figure 7).

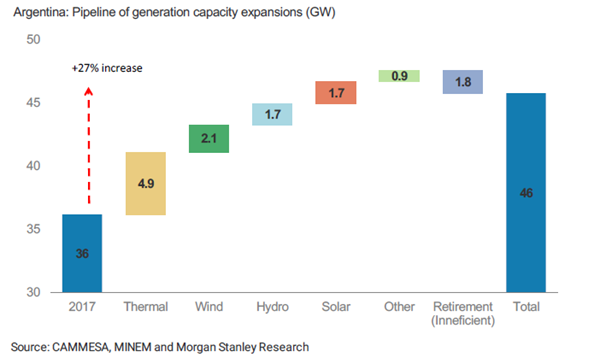

- The government plans to auction off 10 GW of new capacity by 2025 (5GW thermal and 5GW renewable) and has typically auctioned 1-2GW/yr. The next thermal auction will be on September 21, 2018.

- The government will sell its ownership of Central Termica Brigadier Lopez (280 MW + 140 MW under construction; 10 Yr. PPA with CAMMESA; COD 2012; 100% owned by the government) and Ensenada De Barragan (576 MW + 280 MW under construction; 10 Yr. PPA with CAMMESA; COD 2012; 100% owned by the government). These

- auctions will conclude in September 2018.

The government will sell its equity stakes in FONINVEMEM assets (Manuel Belgrano, Vuelta de Obligado, Almirante Brown, and General San Martín), though timing is still unknown.

Figure 7: CEPU’s debt capacity assuming 2-3x leverage

Upside to CEPU’s Valuation

We believe that the impacts of regulatory normalization are skewed to the upside. For CEPU, we believe it is more likely that new project wins will fully offset the removal of inefficient assets. Further, the regulatory impacts of Base Energy tariff normalization and fuel purchase normalization would be viewed positively. We see a path to an additional $8.87/sh. in upside from our base case target if regulatory normalization occurs as detailed below.

- New Thermal Project Wins: Given CEPU has already purchased 3 gas turbines and land in Buenos Aires, we believe that puts CEPU in an advantaged position in future auctions. Specifically, we believe that by having those assets in hand, CEPU can reduce the completion time for a power asset from 24-36 months to 18-24 months. CEPU notes 1,456 MW of potential projects in its company presentation (969M W of gas turbines combined with a 487 MW of steam turbine capacity to form a CCGT). Winning 1,456 MW of capacity, assuming the 70% project debt, would increase our valuation by $3.80/sh.

- Removal of Inefficient Assets: CEPU believes that it has 569MW of thermal power generating assets are inefficient. These assets include 3 steam turbines at Puerto Complex (NP TV05, PN TV07, PN TV08) and 2 steam turbines at Lujan de Cuyo (MARELLI TV11, MARELLI TV12). These turbines use more fuel than average. The removal of these assets would decrease our valuation by $1.84/sh. It is worth noting that CEPU has 500 MW of efficient steam turbines, as deemed by the company. Longer term, as more efficient technology comes online, these efficient turbines could become inefficient.

- Base Energy Tariff Normalization: We believe that the disparity between Base Energy prices and New Energy prices will normalize at some equilibrium. This could occur either if the government increases Base Energy rates or the government allows for a thermal TERM market, like it does for renewable assets. In a term market CEPU could receive rates closer to market prices for its efficient thermal assets (1,154MW of CCGT & Co-Generation assets). This optionality could be worth $4.95/sh. in value.

- Fuel Purchase Normalization: CEPU expects to benefit from an additional operating margin if fuel purchasing responsibility is shifted back to generators, as opposed to the current regime in which CAMMESA is responsible. Given CEPU’s scale as the largest private sector power company in Argentina and the strategic location of its thermal assets, CEPU expects to benefit from better fuel prices than the reference pass-through values provided by CAMMESA. CEPU had historically realized a 5-10% margin on fuel purchases prior to the regulatory distortion period. Assuming a 5% fuel margin, fuel purchase normalization could be worth $1.97/sh. in value.

3) Macro Overview

We are still constructive on the medium/long term structural story of Argentina, Latin America’s third largest economy, but acknowledge the cyclical speed bumps that Argentina has hit and the challenges to macro stability that remain over the short-term. Argentina chose a gradual approach to macro normalization: specifically, to tame high inflation, stimulate growth, and reduce the fiscal deficit. The delicate balancing act to simultaneously accomplish all three goals, while maintaining political capital, was derailed by a confluence of factors, both domestic and external.

For context, current president Mauricio Macri, who was elected in 2015, inherited a large fiscal deficit from the prior regime. Argentina had been in the eye of the perfect storm for quite some time, allowing stagflation to spread and the fiscal deficit to spiral out of control. Macri’s solution was policies aimed at lowering inflation through the Central Bank, increasing social spending to guarantee governability, and reducing government expenditures by cutting subsidies, particularly those for public transport, utilities and other public goods. The lynchpin of this plan was that economic growth would reverse the fiscal deficit and finally tame inflation. To stimulate growth Macri focused his efforts on opening Argentina’s capital markets. Most importantly, Macri settled with creditors from the 2002 bond default. This settlement effectively opened Argentina to the international bond markets after having been shut out for well over a decade and allowed Argentina to finance its debt externally. Macri continued this capital markets reform by lifting currency controls, opening borders for trade and passing tax reform. These policies have been validated through MSCI’s upgrade of Argentina from frontier market to emerging market status in June 2018.

When Macri took office in December 2015, inflation was running around 30% and the fiscal deficit was 5.4% of GDP. When Macri allowed the peso to float, it quickly devalued by 29%. Consequently, he gave the central bank freedom to raise rates to target inflation. The government raised large amounts of foreign-denominated debt to cover the fiscal deficit. Over 70% of the country’s debt is foreign denominated. Capital flowed into government bonds on the back of ultra-high interest rates, artificially strengthening the peso against the dollar. That kept imports high and made it hard for exports to compete. The worst drought in 30 years and weakness in Brazil, Argentina’s main trading partner, caused a further reduction in Argentina’s exports. The combined effect caused the current-account deficit to rise to more than 5% of GDP. At the same time, inflation remained persistently high. As the Central Banks inflation targets moved further out of reach, the Central Bank’s credibility began to be challenged.

The US Federal Reserve’s interest rate hike in May caused both the dollar to strengthen and a reversal in the liquidity conditions in emerging markets. The Argentine peso devalued sharply. The central bank hiked interest rates to 40% and tried to prop up the peso using foreign reserves. When that failed Mauricio Macri, secured a $50bn credit line from the IMF. Although IMF credit line means most of Argentina’s external-financing requirements are covered until 2020, it is tied to austerity measures. Specifically, Argentina is required to cut the budget deficit, which reached 3.9% in 2017, to 1.3% of GDP by 2019 and to zero by 2020. The savings are supposed to come from postponing infrastructure projects; cutting subsidies and transfers to the provinces; and shrinking the federal payroll.

We expect the downturn in activity in 2Q18 to continue into 3Q18 amid high inflation and a tighter policy mix. We believe this will negatively affect sentiment and politics in Argentina. Moreover, the acceleration of fiscal consolidation objectives will remain a drag on growth for the foreseeable future, reducing the likelihood of a sharp recovery.

While a recovery in Brazil remains a wild card, the drought should be a one-time event. One positive about this backdrop is that, with tighter fiscal policy and a subdued growth outlook, the needed correction in external accounts may end up materializing sooner than anticipated. The Argentine consumer is still under levered and Argentina’s debt to GDP ratio is still manageable. Absent another bout of sizable currency volatility, and assuming fiscal objectives are met this year and next, the economy would be on more solid footing, and therefore more likely to be able to sustain growth in the next political cycle, provided there is no significant change in policy direction.

While we don’t preclude the possibility of things getting worse before they get better, we do believe that a lot of the carnage is behind us. After being one of the best performing markets in 2017, Argentina is the worst performing market in 2018 YTD. The MSCI Argentina benchmark (USD denominated), Merval Index (ARS denominated) and Argentine Peso have lost 53%, 25% and 38% YTD, respectively. The two biggest risks to the recovery are a deterioration in the social and political dynamics that undermine overall governability conditions/the current regimes political prospects in the 2019 election; and a risk-off scenario that could eventually trigger another episode of currency depreciation.

4) Argentina Macro Implications on CEPU

Major EM currency crises typically ignite broad-based equity sell-offs that are followed by a selective and powerful recovery of high quality stocks. We think earnings from the Argentine utility sector should be supported by a) macro protection (FX and inflation passthrough; GenCo’s revenues dominated in USD), and b) capacity expansions.

Although there was a change in leadership of the Energy Ministry in June 2018, we believe that the current administration remains committed to the normalization of tariffs and prices, as well as the removal of unnecessary subsidies from the power sector. Importantly, we understand that all contracts and tariff review processes will be honored, which removes an important concern and overhang.

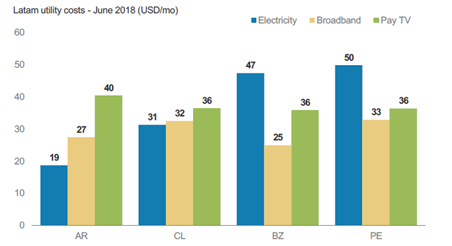

Importantly, electricity prices in Argentina are not yet extremely high vs. both other LatAm countries and vs. other average monthly bill for consumers (in Buenos Aires, average June 2018 electricity bill stood at US$19 vs. the US$27 cost of a mid-range broadband package and US$40 for Pay TV). This suggests policy execution, and not affordability, is the key constraint for further tariff normalization in the country.

Figure 8: Cost of electricity in LatAm

Further, the current administration should continue to incentivize domestic generation capacity. We believe investment should be the fastest growing segment of the economy. We also believe that 60%+ of the capex backlog in Argentina is energy intensive. Thus, we think Argentine utilities are poised to benefit not only for tariff normalization, but also from pent-up power demand, regardless of the macro economic cycle. The Ministry of Energy still needs to auction ~10 GW of new projects by 2025, of which ~5 GW will be thermal projects and ~5 GW will be renewable projects.

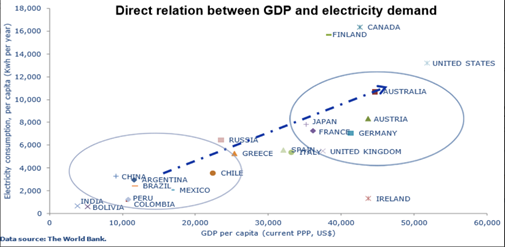

Figure 9: Expected capacity growth in Argentina. There is a direct correlation between GDP growth and electricity demand

5) Market Structure

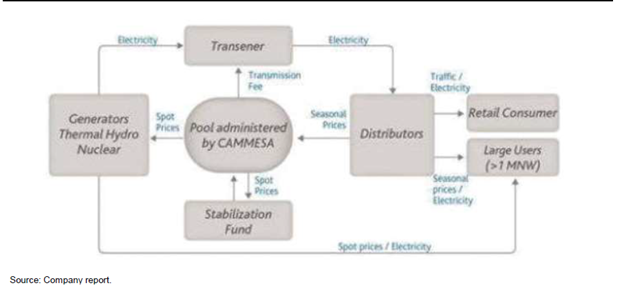

The Argentine electricity sector is formed by a variety of distinct generation, transmission, distribution, commercialization and central load dispatch entities. Cross-ownership in these activities is strictly limited, with the transmission entities being forbidden to own any part of a generating or distribution enterprise and cross-ownership of distribution and generating assets is limited to ten percent of the entire market. Most of these companies are in private hands, with only minor participation by the federal government in the generation sector.

Market Participants

- Generators are companies with electricity generating plants that sell output either partially or wholly through the SADI. Generators are subjected to the scheduling and dispatch rules set out in the regulations and managed by CAMMESA. In the past, generators were able to enter into direct contracts with distributors or large users. However, this possibility was suspended by SE Resolution No. 95/2013. As of December 31, 2017, Argentina had a nominal installed capacity as reported by CAMMESA of approximately 36.5 GW (+2.6 MW compared to 2016), composed by 62.7% of thermal, 30.4% of hydroelectric, 4.8% of nuclear and 2.1% of renewable.

- Besides CEPU, the Argentine power generation market consists of four major players:

- Pampa Energy (NYSE: PAM): 3,871 MW installed capacity with 554MW under construction. PAM is a vertically integrated power producer, with an E&P unit and equity stakes in electricity transmission company (Tranener), electricity distribution company (Edenor) and gas transportation company (TGS)

- AES Argentina Generación S.A.: A subsidiary of US power group AES Corp. (NYSE: AES). The company operates 3,528MW of capacity in Argentina.

- ENEL: Enel Américas participates in energy generation in Argentina through its subsidiaries Enel Generación Costanera, Enel Generación El Chocón and Central Dock Sud. The three companies together have a total of 4,537 MW of installed capacity

- YPF EE: Subsidiary of Argentine E&P YPF (NYSE: YPF). 1.8 GW installed capacity (0.15 GW installed within its upstream business) with 0.6 GW under construction.

- Pampa Energy (NYSE: PAM): 3,871 MW installed capacity with 554MW under construction. PAM is a vertically integrated power producer, with an E&P unit and equity stakes in electricity transmission company (Tranener), electricity distribution company (Edenor) and gas transportation company (TGS)

- Besides CEPU, the Argentine power generation market consists of four major players:

- Transmission companies hold a concession to transmit electric energy from the bulk supply point to electricity distributors. The transmission activity in Argentina is subdivided into two systems: the High Voltage Transmission System (‘STEEAT’), which operates at 500 kV and transports electricity between regions, and the regional distribution system (‘STEEDT’) which operates at 132/220 kV and connects generators, distributors and large users within the same region. Transener is the only company in charge of the STEEAT, and six regional companies are located within the STEEDT (Litsa, Transnoa, Transnea, Transpa, Transba and Distrocuyo)

- Distributors are companies holding a concession to distribute electricity to consumers in a geographic area. Distributors are required to supply all of the electricity in their concession area, at prices set by regulation. The three distribution companies divested from SEGBA (Edenor, Edesur and Edelap) represent more than 40% of the electricity market in Argentina. Only a few distribution companies (i.e., Empresa Provincial de Energía de Córdoba, Empresa de Energía de Santa Fé, and Energía de Misiones) remain in the hands of the provincial governments and cooperatives.

- Large Users: The wholesale electricity market classifies large users of energy into three categories: (1) Grandes Usuarios Mayores (Major Large Users or ‘GUMAs’), (2) Grandes Usuarios Menores (Minor Large Users or ‘GUMEs’) and (3) Grandes Usuarios Particulares (Particular Large Users or ‘GUPAs’). Each of these categories of users has different requirements with respect to purchases of their energy demand. For example, GUMAs are required to purchase 50% of their demand through supply contracts and the remainder in the spot market, while GUMEs and GUPAs are required to purchase all their demand through supply contracts.

- CAMMESA (Compañía Administradora del Mercado Eléctrico Mayorista or ‘Argentine Wholesale Electricity Market Clearing Company’): The creation of the WEM (‘Wholesale Electricity Market’) made it necessary to create an entity in charge of the management of the WEM and the dispatch of electricity into the SADI (Sistema Argentino de Interconexión or ‘Argentine Electricity Grid’). The duties were entrusted to CAMMESA, a private company, created for this purpose. 80% of CAMMESA is owned by agents of the wholesale electricity market (generators, distributors, transmission companies and large users) while the other 20% is owned by the Energy Ministry. The main objectives of CAMMESA are to coordinate economic-technical deliveries from the SADI grid, supervise the quality and security of SADI's operations, oversee economic transactions in the spot and future markets, and manage billing, collection and financial operations of market funds. The purchase and dispatch of fuels remains centralized in CAMMESA. Further, CAMMESA is also the entity that collects the subsidies from the government.

Figure 10: Structure of wholesale electricity market

Regulatory

- ENRE (Ente Nacional Regulador de la Electricidad or ‘National Electricity Regulatory Entity’) Autonomous agency responsible for enforcing the regulatory framework and controlling concession contracts. It monitors compliance by the federal distribution companies (EDENOR, EDESUR and EDELAP) with tariffs and services, while provincial regulatory authorities monitor compliance by local distributors subject to provincial regulatory frameworks.

- Ministry of Mines and Energy: Successor of the Secretariat of Energy, its main duties include the implementation of national policies and oversight of the regulatory framework

6) Brief History of Argentine Power Market

- 1990-2001 – Marginal system: Regulatory framework was robust and based on free competitive market conditions among power generation companies; spot prices defined according to the marginal cost of the system; and the companies had reasonable returns.

- 2002-2015 – Regulatory Distortions: After the 2001 economic crisis, a period of high government intervention started, including the conversion of prices and tariffs to ARS peso (from USD), the centralization of power contracts at CAMMESA and the reduction of company’s attractive profitability and investment levels. These measures created a huge structural deficit in the operation of the wholesale electric market and caused many Argentine electricity generators, transmission companies and distributors to defer further investments. In this context, the government had to create certain programs to incentivize new installed capacity and to preserve old capacity plants’ operation. A few examples are: i) Res. 220/2007 & Energia Plus: established a free price scheme for new installed contracted capacity; ii) Resolution 95/2013: Energía Base pricing moved towards a “cost plus” system with a fixed and a variable component; and iii) FONINVEMEM: fund created to reinvest remuneration owned by CAMMESA to new generation power projects.

- 2016-2018 – Transition to potential normalization: In 2016, the new federal government enacted the Power Sector Emergency Law, making several adjustments towards the normalization of companies’ profitability and stimulating new investments. Resolution 19/2017 is the one that current establishes the remuneration of old energy. The Argentine government hiked the remuneration scheme for “old energy” by >100% (avg. hydro and thermal) between 2016 and 2017 and converted it back to USD

7) Prior Auctions

Thermal

The Argentine government is targeting 10GW of additional thermal capacity by 2025, of which 4.7GW have already been auctioned off.

- Resolution SEE 21/2016: The Secretariat of Electric Energy auctioned new thermal generation units to become operational between 2016 and 2018. Power generation companies entered into PPAs with CAMMESA denominated in USD. The program awarded 2.9 GW of installed capacity, with average total prices (capacity + generation) of US$21,951/MW-month.

- Resolution SEE 287-E/17: The Secretariat of Electric Energy awarded 1.8 GW of installed capacity from combined cycle or co-generation units, with average total prices (capacity + generation) of US$20,568/MW-month. Units under this resolution have PPAs with CAMMESA denominated in USD. These units have their own permanent and guaranteed fuel supply, which reduces the need for transportation and lowers costs.

- CEPU contracted two cogeneration projects: i) San Lorenzo (330 MW), at an average total price (capacity + generation) of US$23,480/MW-month; and ii) the expansion of Luján de Cuyo (93 MW), at an average total price (capacity + generation) of US$22,860/MW-month.

Renewables

The Argentine government is promoting the production of energy from renewable sources. The government has mandated that the minimum renewable energy share of total consumption increase from 8% in 2018 to 20% by 2025. Larger users (+300kW) will need to gradually increase the purchase of energy from renewable sources, meeting specific goals. The Argentine government is targeting 10GW of additional renewable capacity by 2025, of which 5.1GW has already been auctioned off.

- RenovAR Program Rounds 1: In July 2016, the Ministry of Energy and Mining auctioned called 1.1 GW the capacity of new renewable projects, mostly from wind (708 MW), solar (400 MW) and biogas (1 MW). Average prices totaled ~US$60/MWh for wind and solar projects.

- CEPU contracted the La Castellana wind project (99 MW) for US$61.5/MWh.

- CEPU contracted the La Castellana wind project (99 MW) for US$61.5/MWh.

- RenovAR Program Round 1.5: In October 2016, the Ministry of Energy and Mining auctioned 1.3 GW of installed capacity from wind (765 MW) and solar (516 MW) projects, at average prices of ~US$55/MWh.

- CEPU contracted the Achiras wind project (48 MW) for US$59.4/MWh.

- CEPU contracted the Achiras wind project (48 MW) for US$59.4/MWh.

- RenovAR Program Round 2: In August 2017, the Ministry of Energy and Mining auctioned a total amount of 2 GW of renewables, mostly from wind (993 MW), solar (816 MW), biomass (156 MW) and others (75 MW). Average prices totaled ~US$42/MWh for wind and solar projects.

- CEPU contracted the Genoveva I wind project (87 MW) for US$40.9/MWh.

- CEPU contracted the Genoveva I wind project (87 MW) for US$40.9/MWh.

- MATR: The government has allowed a term market for renewable energy. In 2018, 0.8 GW of PPA’s were auctioned off.

- CEPU contracted the La Castellana II wind project (15.7 MW), Achiras II wind project (79.8 MW), and Genoveva II wind project (41.8 MW). The PPA’s for these projects are still under negotiation, but are likely to be in the US$60/MWh range

8) Counterparty Risk

CAMMESA is the off taker of almost all CEPU’s electricity generation and as such, is CEPU’s primary creditor. CAMMESA collects cash from power distributors and the government (i.e. subsidies) and pays generators and fuel producers. Since the government subsidizes electricity costs and has been known to backstop any temporary cash flow shortfall at CAMMESA, we believe that CAMMESA should have the same credit profile as the Argentine government. Argentina has a credit rating of (Fitch: B; Moody’s: B2; S&P: B+) and its USD denominated sovereign bonds yields 10%. Assets remunerated under the New Energy regime, which have legally binding PPA’s, have priority over Base Energy assets in CAMMESA’s cash flow waterfall.

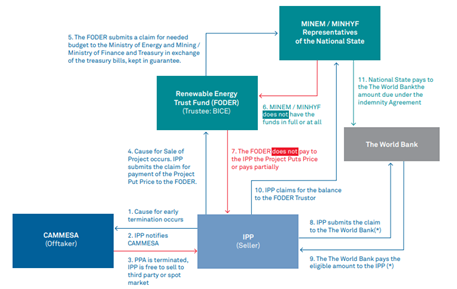

Renewable assets (wind/solar) in the RenovAR program, which also have PPA’s with CAMMESA, have secondary credit enhancement through a credit backstop by the World Bank (Figure 11). We believe this secondary credit enhancement could lessen the interest rate risk on the project debt that CEPU expects to use to finance the next four wind projects.

Figure 11: RenovAR counterparty flow chart

9) Regulatory Trajectory:

Over time we believe that the Energy of Ministry will shift the power generation policy back towards a market regime. In other words, the energy price received by GenCos would be determined according to the system marginal cost, instead of being fixed by the regulator as it is now. While CAMMESA dispatches power plants based on marginal cost, including fuel, the Base Energy structure incentivizes inefficient assets to stay in the market. This is because 1) CAMMESA provides fuel to Base Energy generation assets and 2) roughly speaking, the Base Energy variable remuneration rate covers the operators fixed costs and the capacity payments are the generators’ margin. Thus, inefficient assets that don’t produce any power are still economical. Over time, we expect the government to shift fuel supply responsibility back to generators and shift the remuneration rate mix to more of a variable rate policy (i.e. incentivizing efficient generation).

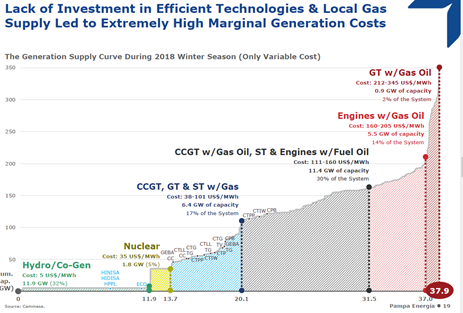

Given Argentina still lacks sufficient systemwide capacity, Argentina must add additional efficient power generation capacity before it can remove inefficient power generation capacity from the system. Units that run exclusively on high priced gas oil (5.5 GW of system capacity, of which CEPU has 0 GW) would be the first to be removed by the system, followed by those that run on fuel oil (CEPU has 1 GW of Steam Turbine capacity that can switch between natural gas and fuel oil).

Figure 12: Argentine Generation Supply Curve

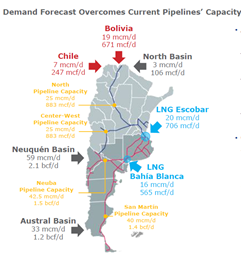

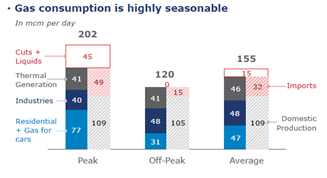

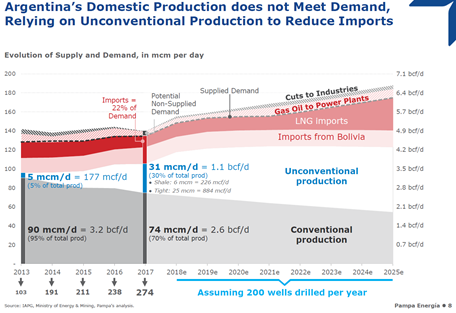

In the short term, we do not expect a change to current policies because Argentina is short 45mcm/d of natural gas in the winter. Argentina imports gas in the winter using 2 LNG fuel ships and by pipeline from Bolivia and Chile. While domestic gas production and imports will continue to increase, so will thermal capacity. Argentina will still need to use liquid sources (fuel oil/ gas oil) to meet production needs over the forgeable future (Figure 13). When Argentina is short of natural gas, particularly in the winter, efficient units that run exclusively on natural gas cannot run if they do not have access to an adequate fuel supply. Further, the efficiency dynamics change when there is fuel switching. As result of differences in fuel prices, a CCGT that would typically run on natural gas could switch to gas oil, making it less efficient than steam turbines that switched from natural gas to fuel oil. The price of gas oil ($15/mmbtu) is significantly above the price of fuel oil ($7/mmbtu; import parity with LNG).

Figure 13: Argentina is short natural gas in the winter. Argentina will continue to need liquid fuel sources to meet power demand for the foreseeable future.

The Argentine government hiked the remuneration scheme for “old energy” by >100% (average hydro and thermal) between 2016 and 2017 and converted it back to USD. The Secretariat of Electric Energy cited the fact that WEM prices have been distorted and discouraged private sector investment in power generation. It concluded that it was necessary to raise tariffs to partially compensate for increasing operation and maintenance costs and to improve the cash flow generation capacity of generators. We believe that the Argentine government will continue to normalize tariffs in the future to gradually restore economic rationality and price equilibrium. Currently, old capacity sells for an average of $18/MWh versus $60-70/MWh for new capacity. The reopening of the term market for thermal assets would be one mechanism to reduce the price disparity between Base Energy and New Energy pricing.

Figure 14: Base Energy vs. New Energy Prices and Base Energy Pricing of Thermal vs. Hydro

10) Risks

- Non-renewal of Piedra del Aguila hydroelectric plant concession: We believe that this asset does ~$51M in EBITDA/yr. assuming normalized water flows. Capitalized at 6x, this would reduce our valuation by $2.00/sh. We highlight that the Argentine government

has not yet defined conditions for hydro concession renewal; however, we expect CEPU to renew this concession before it is up. - Reduced water flow at Piedra del Águila could cause variability of results.

- Execution risk in building new projects.

- Increased competition in future capacity auctions could compress IRRs. Some smaller entrants have entered the market for renewable projects (solar and wind), which have reduced winning bids is subsequent auctions (RenovAR 1 vs. RenovAR 2). Thermal bidding has remained relatively stable since they are more complicated projects and require a higher level of expertise.

- Price scheme shift toward a market approach could remove CEPU’s inefficient assets from the system before or without winning future capacity.

- FX lagging inflation could lead to lower profitability in USD terms.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

- Expansion projects coming online

- Winning additional thermal capacity auctions

- Winning auctions for the government's ownership stakes in existing power generation assets

- Opening of a thermal TERM market

- Increase in Base Energy remuneration rate

- Improvement of macro conditions in Argentina

| show sort by |