| 2020 | 2021 | ||||||

| Price: | 37.62 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 36 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 1,339 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 74 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,413 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- winner

- None found

- BETA

- IRHYTHM TECHNOLOGIES INC IRTC S 09/16/2018

Description

Note: I submitted this writeup for my application to VIC a week ago. Since then, the stock has drifted lower with the market which makes the multiples discussed below about half a turn higher than today’s levels.

My favorite investment ideas tend to be opportunities where you don’t need to believe very much to get a solid return and have free options which could lead to much higher returns. It’s hard to find these opportunities in today’s world, but I think Biotelemetry (“BEAT”) fits this framework.

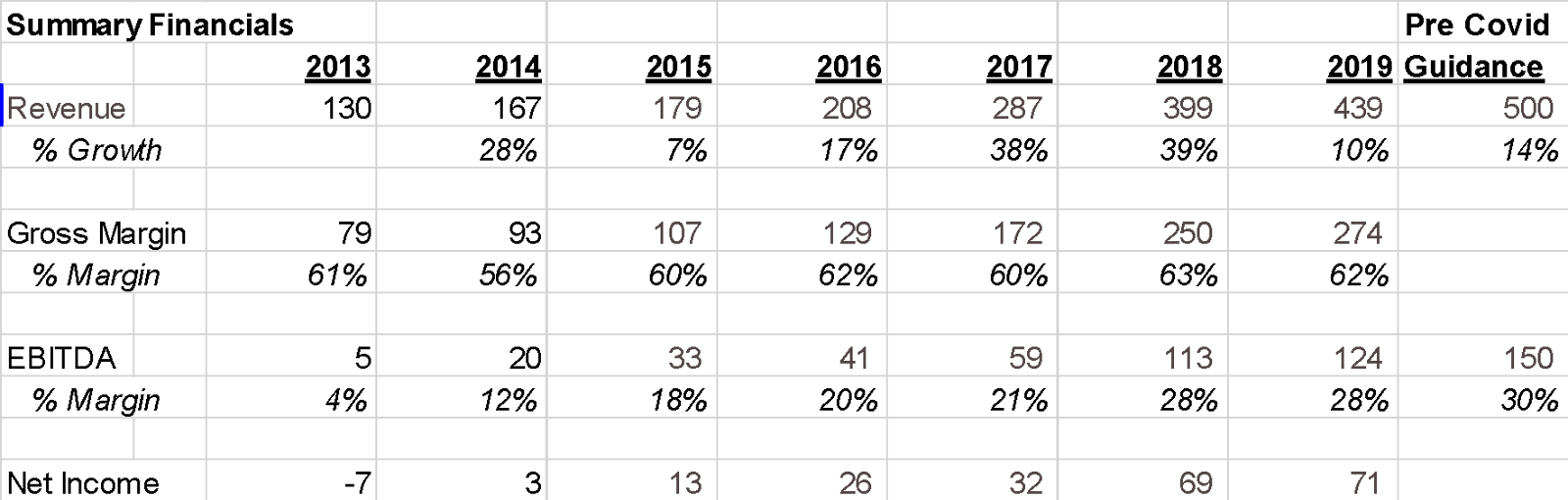

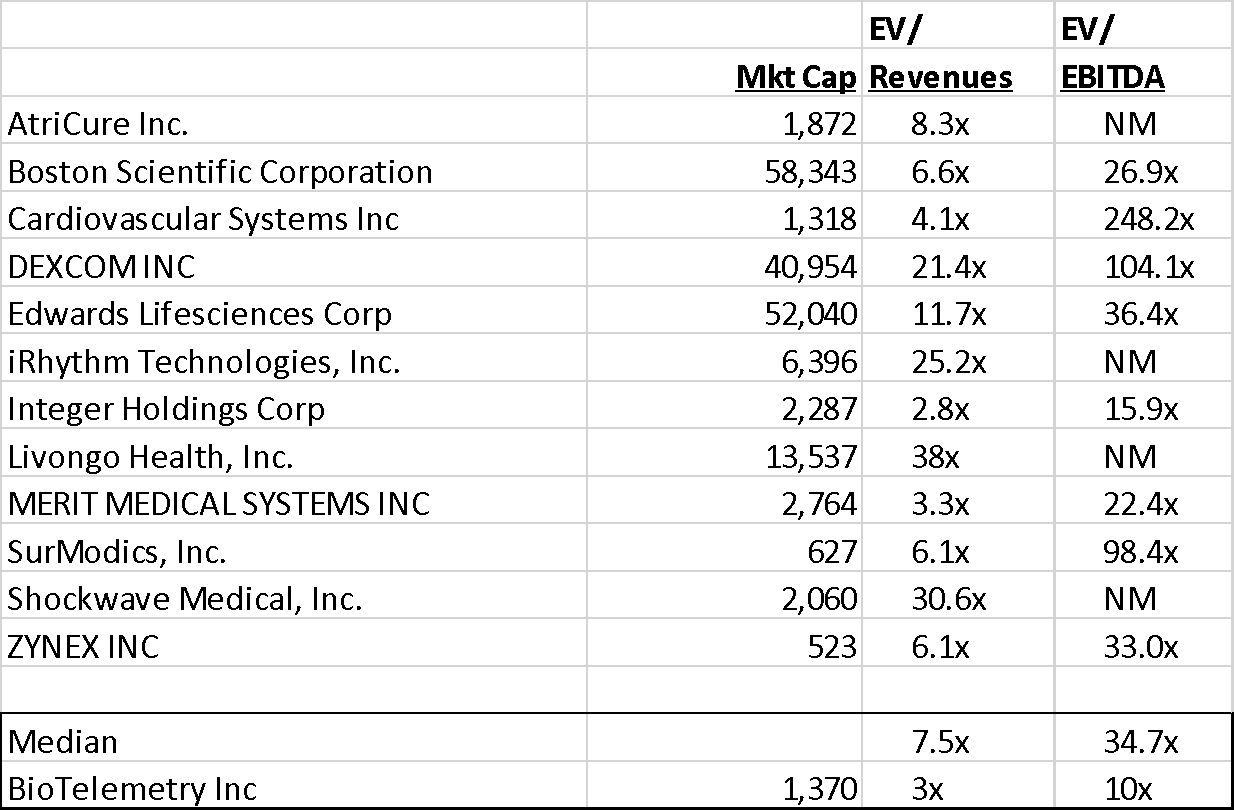

I believe that the shares of BEAT, a leader in the cardiac monitoring industry, are materially undervalued at current prices and could easily double as it emerges from a covid induced slowdown in doctor’s office visits. In addition, BEAT has several remote monitoring initiatives in the early stages of rollout / incubation that could trigger a wholesale rerating if they begin to gain traction. BEAT currently trades for around 3x Revenues and 10x what I consider normalized EBITDA (based on pre covid guidance). This is a massive discount to comparables which is even more surprising given the following:

- BEAT has grown for 30+ consecutive quarters (pre covid)

- Has more than doubled revenues and almost quadrupled EBITDA over the past 5 years (includes the acquisition of Lifewatch)

- Is growing organically in the low teens with the potential to accelerate

- Has a history of excellent capital allocation

- Its largest business is about twice the size of iRhythm ($6B mkt cap, 25x Revenues)

- It recently acquired a SAAS based cardiac monitoring business that has already doubled run rate revenues (about $30mm revenue) and has a $1B TAM according to management

- It made a significant move to accelerate its diabetes management product that’s similar to Livongo ($13B mkt cap, 38x Revenues)

- Its “slow growth” research services division, which was expected to be flat this year, had 34% growth in bookings

- Monitoring volumes have basically recovered to pre covid levels despite a dropoff in doctor’s office visits

Company / Industry Background

BEAT has alot going on for a small cap company and very little analyst coverage, which is one of the reasons I think this opportunity exists. The simplest way to understand the moving parts is based on the guidance they gave coming into the year which at the time was estimated to be about $500mm in revenues and close to 30% EBITDA margins. Of that about 80% was the traditional Heart Monitoring business 20% was everything else which I estimate as $60mm for Research Services, $30mm for Geneva (the software division) and $10mm for the various digital population health initiatives (including diabetes management).

Health Care Monitoring -- BEAT was once a hot IPO (in 2008). They basically “invented” mobile cardiac outpatient telemetry (“MCOT”). So, what is this industry all about? Basically, heart arrhythmias are very bad, and a big part of cardiology has always been diagnosing and treating these arrhythmias. While you can have an EKG in your doctor's office, arrhythmias don’t present themselves 24/7 and, hence, various long-term monitoring solutions were developed.

|

Diagnostic |

Monitoring |

|||

|

Reimbursement |

Patients / Yr |

Yield |

Time |

|

|

Traditional Market |

||||

|

Holter Monitor |

$50 |

2.5mm |

5-18% |

2-4 days |

|

Event Monitor |

$200 |

1.5mm |

15-68% |

up to 30 days |

|

MCOT |

$800 |

500k |

88% |

up to 30 days |

|

"New" Products |

||||

|

Extended Wear Holter |

$300 |

500k |

60% |

3-14 days |

|

Implantable Loop Recorder |

100k |

9-73% |

3 years |

|

|

Source: BEAT Investor Presentation |

Holter monitors were the first product developed for this market and are still the cheapest and most widely used, despite their limitations. Basically, this is an at home EKG that you wear for two days and take back to your doctor’s office to have the results analyzed. The limitations have always been that a) it isn’t worn for very long and b) people don’t like wearing EKG leads (you can’t shower with them, hard to sleep so patient compliance isn’t that great). Event monitors are somewhat similar devices that are worn for longer periods. They record when the device detects an event or when the patient feels a symptom and presses a button. Neither of these devices were great for potentially severe cases given the turnaround time, so MCOT was invented as a real time solution. BEAT has two remote monitoring centers which are staffed by cardiac monitoring specialists and have to have FDA approval. These centers receive all the data in real time and notify the patient’s physician of any events.

Extended wear holters were popularized by iRhythm’s Zio patch and are currently taking significant share from the traditional holter market. The Zio patch and other similar products are like big bandaids, without the wires and leads of a traditional holter. BEAT’s MCOT device and extended wear holter are also in patch form. They can be worn for up to 14 days, worn in the shower and are generally much more comfortable for the patient, which leads to better compliance. After the 14-day period, they are returned to either the doctor’s office or the company (in the case of Zio) to produce an analysis of the results. I’m not going to wade into the whole diagnostic yield debate or whether patches measure p-waves as well as multi-lead systems because I don’t think it’s super important for what is going on in the industry. I think it’s fairly clear that if patients wear a monitoring device for a longer period, you have a better shot at catching an arrythmia.

Implantable loop recorders are the most expensive and intrusive option for long term heart monitoring courtesy of the large med tech companies. BEAT generally views this as a complimentary / different market since it requires surgery and is usually for patients who have already gone through a battery of diagnostic testing. The main relevance is for BEAT’s software business, Geneva, which automates the ILR workflow on a vendor neutral basis and tracks the ILR data output for each patient. This product has experienced rapid uptake as it provides a significantly improved experience for the doctor and patient. In addition, Boston Scientific, is rolling out it’s ILR this fall and chose BEAT as the exclusive sales agent in North America. While I don’t believe this is financially material, it is a surprising validation of the strength of BEAT’s sales force, especially considering that Boston Scientific has a large investment in Preventice, a BEAT competitor.

Other Businesses -- In addition to its rapidly growing software business Geneva, BEAT has several other businesses in various stages of growth. Its research business which does heart monitoring and imaging studies for clinical trials is a solid business and is one of the reasons why BEAT was chosen as the heart monitoring company by Apple for its watch monitoring study. At around $60mm of revenues, I don’t think it is a near term needle mover, but it seems to have a long growth runway. They have an at home INR testing business which just took over Roche’s business and will be interesting to watch. What I think is the most interesting development is the acquisition last month of Centene’s On.Demand business. Livongo, which has a great writeup on VIC, basically started with an employer driven model which helped companies reduce their self-insured or health plan costs and provided a nice benefit for employees. BEAT’s CEO’s background was in the diabetes market and they had been collaborating with Centene on building out this business for Centene plan members. BEAT took full control of the product which could potentially have enormous potential. Diabetes management for the health plan segment is in the very early stages and would dwarf the current employer model. To give some perspective, Livongo has around 300k mostly corporate sourced lives. On.Demand is currently open to about 4mm of Centene’s 23mm lives, of which 8-10% have diabetes. I think we’ll hear more about this rollout in the coming quarters, but if they are successful with Centene, the market is enormous.

Industry Dynamics / Variant Perception

When BEAT went public, MCOT was a new product and was operating under a provisional CPT code for reimbursement. This is normal for new products. Until last month, extended wear holters (i.e. iRhythm) were also operating under a provisional CPT code. As an aside, Kerrisdale Capital had a short report on iRhythm based on permanent CPT code risk which turned out to be wrong but still has plenty of relevant industry background for those looking for more. In BEAT’s case, the provisional CPT code was so aggressive (with some influence of prior management) and so far away from the competing product (traditional holter) that the permanent CPT code dramatically reduced it. This sent the nascent industry into a tailspin. After the fallout, Joe Capper joined the company and spent years restoring the company to profitability, expanding commercial coverage and consolidating the market (BEAT acquired its largest competitor, Lifewatch, in 2017).

In iRhythm’s case the permanent CPT code basically affirmed the provisional CPT code which sent IRTC stock soaring and led to an additional capital raise. The market seems to believe that IRTC is going to run away with this business which I believe is far from certain. BEAT has a relatively small extended wear holter business (although it’s been growing in triple digits). I think they were wary to jump into a product line with a provisional CPT code given their prior experience with new product reimbursement risk. Now that the CPT code has been finalized, it’s not clear to me why BEAT can’t dramatically increase this product line given how imbedded it is in cardiology practices / the strength of its sales force. In addition, IRTC is trying to expand the extended holter market dramatically by showing that screening of asymptomatic patients for afib can prevent strokes. If this is successful it would create an even larger market for everyone in the industry. IRTC has recently relaunched its MCOT patch, which is based on the same Zio extended wear holter form factor. While there is plenty of background on how this product has been a bit of a dud in the Kerrisdale report, it would be dismissive to assume they couldn’t make some inroads. However, the market opportunity for BEAT in extended wear holter should be larger than any potential headwind.

Management

I have followed this company for quite a while and would say that they are very strong on execution, hence the track record of consistent growth. My biggest concerns were that they seemed overly focused on maximizing quarterly profitability at the expense of investing in new markets and that the management team was stretched too thin. Through the acquisition of Geneva, they added a Chief Medical Officer and also recently added a CTO who came from $30B mkt cap Iqvia. To me it’s starting to look like a company ready to expand, rather than your typical small cap where the CEO and CFO wear numerous hats. The CEO has about $40mm of stock and hasn’t sold any stock in the last 2 years. For a non-founder CEO, I think that this is a meaningful expression of confidence in the future.

Valuation

I don’t think you have to get too creative to see attractive returns at these levels. If you start with pre-covid guidance of around $500mm and assume 10% growth for a couple of years (which is below management’s view) and assume a 15x multiple you get a double. Even if you don’t bake in any multiple expansion, despite the massive discount to the comparables, you are still looking at a mid teens IRR including the free cash flow. If the diabetes program or any of the other population health businesses start to gain significant traction, I believe the upside would be significantly higher than either of those cases.

Reimbursement

About 35% of BEAT’s revenues are from Medicare which sets rates for every covered service annually through the Physician Fee Schedule. Other than cuts in 2013 (which lowered reimbursement by about 14% and resulted in a 4% reduction in pro forma revenues), MCOT reimbursement has been very stable. The formulas that set the rates are complicated but are essentially based on a relative value unit (RVU) and a conversion factor ratio (CFR). The CFR affects all services and is required by statute to make the annual proposed Physician Fee Schedule budget neutral (i.e. it’s an output of all the other changes in the proposal). This year’s CFR proposal represents a cut of about 10%. Typically, CFR cut proposals are viewed as totally arbitrary and lead to intense lobbying pressure across the health care spectrum (since everyone is affected). Changes to the CFR proposal generally require additional congressional funding (or a reallocation of funding in the final Physician Fee Schedule). In the 2010 to 2014 period, for instance, the CFR proposals projected cuts of up to 30% but were “fixed” each year resulting in flattish rates. I don’t have any special insight about what will happen this year but historically the CFR has remained fairly rangebound (www.ama-assn.org/system/files/2020-01/cf-history.pdf). I do think that this proposal has put pressure on BEAT and other health care providers since it was announced in August.

Risks

Recurring weakness from Covid

Market share losses in MCOT to iRhythm

Reimbursement

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Continued recovery from the covid shock to monitoring volumes

Traction in the population health initiatives

Continued strong growth in the extended wear holter space after the permanent CPT code

| show sort by |